Via APRA:

The 10 per cent benchmark on investor loan growth was a temporary measure, introduced in 2014 as part of a range of actions to reduce higher risk lending and improve practices. In recent years, authorised deposit-taking institutions (ADIs) have taken steps to improve the quality of lending, raise standards and increase capital resilience. APRA has written to ADIs today to advise that it is now prepared to remove the investor growth benchmark, where the board of an ADI is able to provide assurance on the strength of their lending standards.

In summary, for the 10 per cent benchmark to no longer apply, Boards will be expected to confirm that:

- lending has been below the investor loan growth benchmark for at least the past 6 months;

- lending policies meet APRA’s guidance on serviceability; and

- lending practices will be strengthened where necessary.

As with previous housing-related measures, this approach has been taken in close consultation with the other members of the Council of Financial Regulators. With risks in the environment remaining heightened, it will be important for ADIs to maintain prudent standards and close any remaining gaps in lending practices.

APRA Chairman Wayne Byres said that while the announcement today reflects improvements that ADIs have made to lending standards, there is more to do to strengthen the assessment of borrower expenses and existing debt commitments, and the oversight of lending outside of policy.

Mr Byres said: “The temporary benchmark on investor loan growth has served its purpose. Lending growth has moderated, standards have been lifted and oversight has improved. However, the environment remains one of heightened risk and there are still some practices that need to be further strengthened. APRA is therefore seeking assurances from ADI Boards that they will maintain a firm grip on the prudence of both policies and practices.”

For ADIs that do not provide the required commitments to APRA, the investor loan growth benchmark will continue to apply.

As part of these measures, APRA also expects ADIs to develop internal portfolio limits on the proportion of new lending at very high debt-to-income levels, and policy limits on maximum debt-to-income levels for individual borrowers. This provides a simple backstop to complement the more complex and detailed serviceability calculation for individual borrowers, and takes into account the total borrowings of an applicant, rather than just the specific loan being applied for.

“In the current environment, APRA supervisors will continue to closely monitor any changes in lending standards. The benchmark on interest-only lending will also continue to apply. APRA will consider the need for further changes to its approach as conditions evolve, in consultation with the other members of the Council of Financial Regulators,” Mr Byres said.

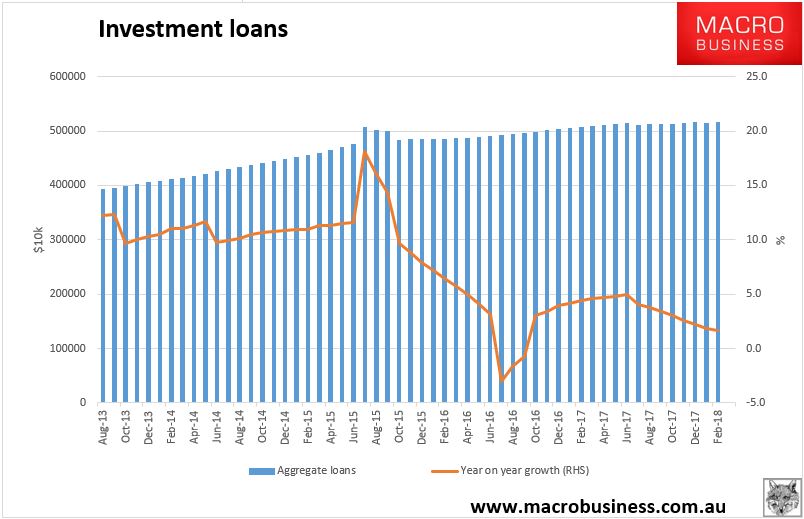

Given investor lending is barely growing that’s fair enough:

Do not remove the interest-only cap.