Via Westpac:

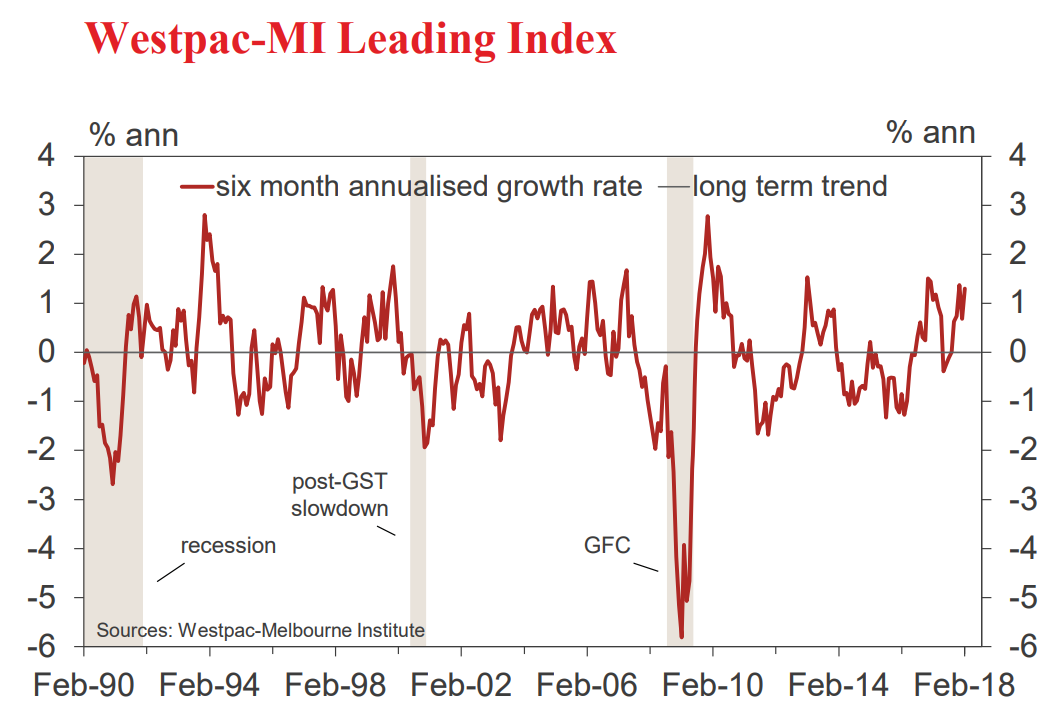

The six month annualised growth rate in the Westpac–Melbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, rose from +0.68% in January to +1.30% in February.

The level of the Index is well above trend indicating improving prospects for growth in the first half of 2018.Following the release of the December quarter national accounts which registered a disappointing overall growth rate of 2.4% for 2017, Westpac modestly raised its forecast for growth in 2018 from 2.5% to 2.7%. That change mainly reflected better than expected momentum in consumer spending in 2017.

It is interesting to examine this strong headline result for the Leading Index in terms of its components. The contribution to growth from the eight components of the Index emphasises the disproportionate impact of international factors. US industrial production (0.53 ppts) and commodity prices (0.40 ppts) explain 0.93 ppts of the overall 1.30 ppts reading. It is disappointing that only 0.18 ppts are contributed by the “domestic” components of the Index – consumer and employment confidence; dwelling approvals and hours worked. Of some concern is that recent prints of the Index have shown a marked deterioration in the contribution of the hours worked series (–0.19 ppt’s in February).

These points are further highlighted in the movements in the Index over the last six months.

In September, the growth rate printed +0.01% compared to February’s reading of +1.30%.

Seven of the eight components contributed to growth over this period with the main drivers being: commodity prices in AUD terms (+0.74ppts); US industrial production (+0.48ppts); the S&P/ASX200 Index (+0.25ppts); a steeper yield curve (+0.12ppts); dwelling approvals (+0.11ppts); Westpac-MI CSI expectations index (+0.05 ppts); and Westpac-MI Unemployment index (+0.02 ppts).

Aggregate monthly hours worked provided a significant offsetting drag (–0.47ppts).

Overall, however, the four “domestic” components of the Index (dwelling approvals; two confidence measures; hours worked) detracted –0.29 ppt from the sharp lift in the Index.

The Reserve Bank Board next meets on April 3. The Board is almost certain to keep rates on hold. The Minutes from the March Board Meeting emphasise the Board’s caution around growth and inflation. Only gradual progress is expected on the wages and inflation front.

There is also some uncertainty as to whether the Board has lowered its current bullish 3.25% growth forecast for 2018. That issue will not be settled until the next Statement on Monetary Policy on May 4.

When the Bank was confidently predicting 3.25% growth for 2018 it seemed likely that it expected to be raising rates in 2018. The signals in the latest minutes indicate that it may indeed be reassessing that expectation.

While Westpac has modestly lifted its 2018 growth forecast from 2.5% to 2.7% it retains its 2.5% forecast for 2019. If the economy is slowing into 2019 the need to raise rates in that year may be less urgent than most expect.

Westpac confirms its forecast that rates will remain on hold in both 2018 and 2019.

Yawn. Already history.