Investors are nervous about the return of trade protectionism. Tariffs imposed by US President Trump in early 2018, contributing to the resignation of chief economic advisor Cohn, have caught the attention of the market. Some commentators are now talking about retaliation from major trading partners. All of this is occurring in the context of Trump’s “Make America Great Again” (MAGA) campaign, raising concerns about a broader economic and redistributive agenda at work. Certain sectors of the US economy may indeed be boosted by Trump’s measures—but at the expense of the rest of the world. After all, decades of economic growth, low inflation and credit creation have been achieved on the back of globalisation. Therefore, it stands to reason that there are material economic and financial risks from de-globalisation.

That said, the tariffs that have been announced so far have been limited in scope:

1. Tariffs announced in January apply to imported solar panels and washing machines. Early March tariffs apply to imported steel and aluminium.

2. Steel and aluminium tariffs were intended to shore up national security, notwithstanding potential costs.

3. Steel and aluminium tariffs will not apply to Australian exports, following recent negotiations.

We do not have particularly strong views about the likelihood of protectionism returning in earnest. We share the concerns of Australia fiscal and monetary policy makers about the economic and financial market risks from protectionism. We are particularly concerned about the availability of USD liquidity in offshore markets. But we also believe that there are downside risks to liquidity even in the absence of protectionist shocks. Indeed, we think that trade war talk ultimately distracts us from the underlying tightening of USD liquidity conditions occurring globally on the back of developments other than fiscal policy.

Absolutely nothing … for Australia

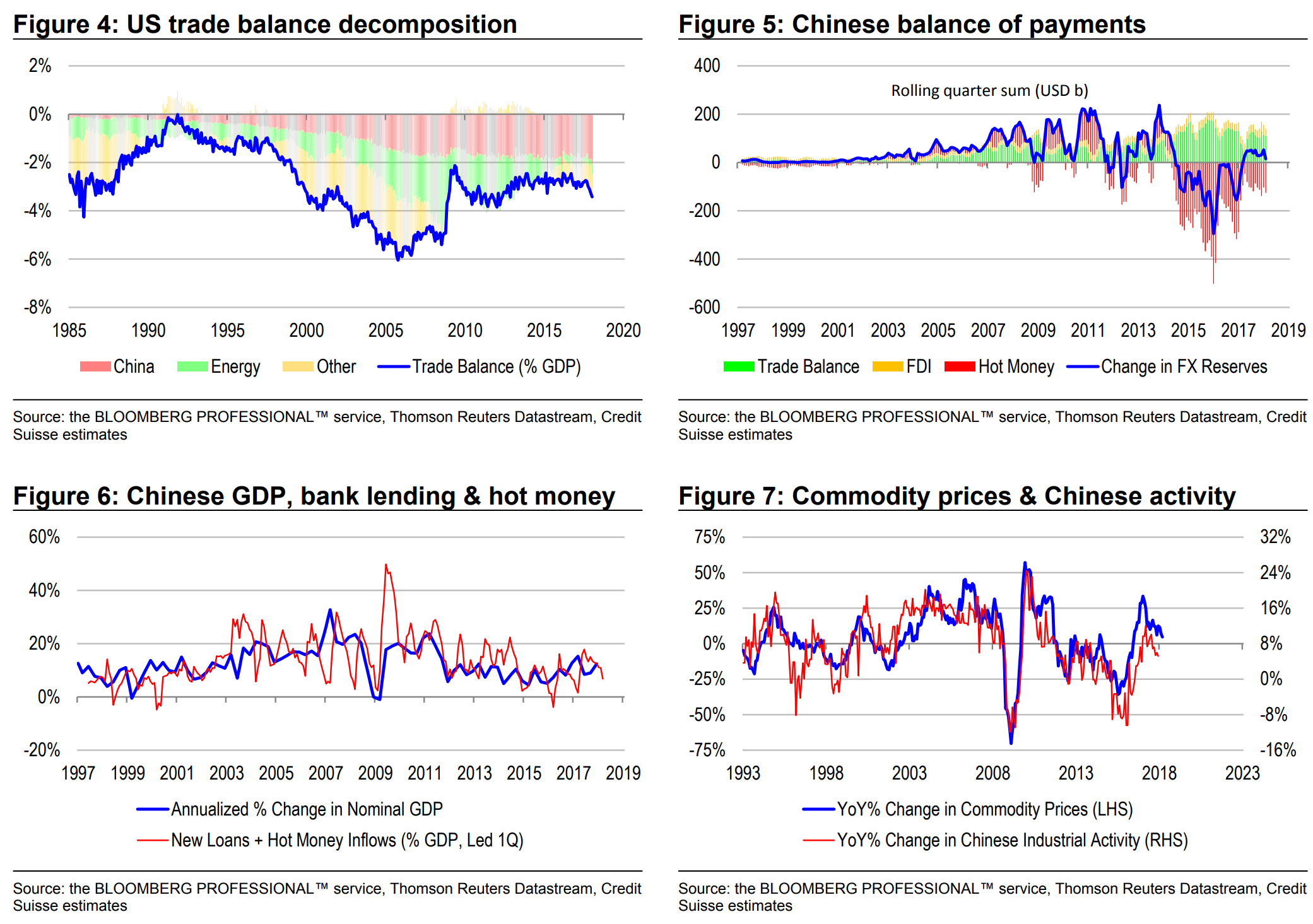

Recently, Australian Prime Minister Turnbull and RBA Governor Lowe spoke out against the dangers of trade protectionism. Such vocal opposition is unsurprising given that historically, USD liquidity has mattered a lot for the Australian economy and markets. One proxy for USD liquidity is the size of the US trade deficit. The larger the US trade deficit, the more the economy is net importing goods and services from the rest of the world. But equally, the larger the trade deficit, the more USDs the economy is exporting for payment.

Interestingly, there is a reasonably strong and positive correlation between the size of the US trade deficit and Australian equity market performance, whether measured in price or earnings terms. To explain this correlation, several linkages come to mind:

1. China and commodity prices.

2. “Foreign funding” of Australian banks.

3. China and housing demand.

On the commodity price front, there is a well-known inverse correlation between commodity prices and the USD because commodities are priced in USDs. However, if this were all there was to the story, movements in USD liquidity should have no net impact on AUD-denominated commodity prices. We believe that there is a non-linear relationship between USD liquidity and commodity prices because of China and because there are more determinants of the AUD/USD than just commodity prices.

As USD liquidity increases in offshore markets, hot money flows tend to move in China’s direction. This forces the People’s Bank of China (PBoC) to either allow the price of money (the exchange rate) to adjust or to allow the domestic quantity of money to adjust instead. Under the pegged exchange rate regime, the PBoC usually chooses to allow quantities to adjust over prices and the resulting money supply expansion contributes to super-normal growth in demand and commodity price inflation. On the flipside, as USD liquidity decreases, capital repatriation from foreigners complicates the PBoC’s domestic liquidity management. This can cause an unintended and unexpected tightening of Chinese financial conditions resulting in slower growth and weakness in commodity prices.

Through time, as the US has run large and persistent trade deficits, and as USD liquidity has increased in offshore markets, USD-denominated commodity prices have tended to rise because of the “crowding in” effect occurring in China. But AUD-denominated commodity prices have also experienced an uplift, because the Australian private sector has leveraged up at the same time. Not only has excessive household leverage constrained what the RBA can do with rates, weighing on Australian-US interest rate differentials—but excessive credit creation has directly caused money supply expansion, diluting the currency.

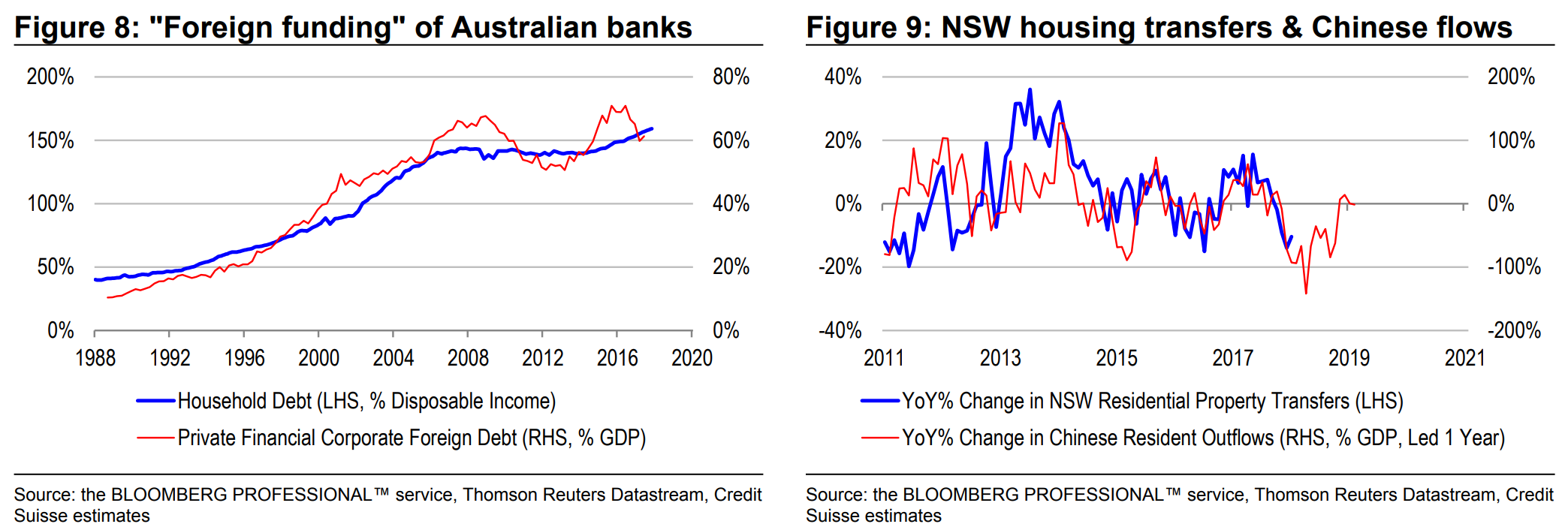

Many commentators believe that Australian households have indirectly borrowed from abroad via the banks to fund their mortgages. Indeed, there is a strong positive correlation between household debt and bank foreign debt. If this thesis is correct, perhaps USD liquidity expansion has contributed to Australian growth via credit creation. However, we must be careful to distinguish correlation from causation. Australian borrowers cannot use USDs to pay for their houses. And loans create deposits as a matter of double-entry accounting. Therefore, there is technically no funding problem for Australian banks. But over the past few decades, Australian banks have opted to go abroad for term funding.

This is unnecessary from a pure funding perspective, but understandable from a duration matching perspective. Mortgages are typically long-duration assets for banks. But deposits are typically short-duration liabilities. If, for regulatory purposes, banks are required to duration match their assets and liabilities, banks have an inherent need to lengthen the maturity of their liabilities, by taking on term funding. But as term funding markets are not well developed in Australia, banks are forced to search for it abroad instead. They can create a synthetic AUD-denominated exposure by taking on an appropriate currency hedge at the same time. In so doing, they effectively use the USDs they acquire from abroad to buy back the very AUD deposits they created in the first place.

In short, we are not fans of the traditionalist view that the historical abundance of USD liquidity has directly contributed to credit expansion in Australia and the earnings of domestic financial and non-financial companies. To be sure, banks have chosen to expand their USD funding books as they have extended more credit to households. But this has been a choice, more than it has been a necessity. In the event that banks choose not to take on foreign term funding (or foreigners refuse to extend this funding), they will simply shorten the duration of their liabilities, and will have to sell AUDs to buy USDs to close out their foreign funding positions. This is not to say that there is no relationship at all between USD liquidity in offshore markets and Australian credit creation. After all:

1. Chinese resident capital outflows are historically pro-cyclical, and have been a major driver of Australian housing demand over the past decade. Until very recently, banks have been very happy to lend more to local home-buyers to match the buying power of the Chinese.

2. During episodes of USD liquidity shortages, we have seen credit conditions seize up globally, causing banks to become much more selective in their lending practices. This is because there is a critical mass of non-US institutions in the world that requires USD funding. When such funding dries up, these entities often face severe currency mismatches which can exacerbate illiquidity in markets and lead to defaults.

In summary, we can see several fundamental linkages between USD liquidity availability and Australia’s performance. Much of this centres on China, and perhaps unsurprisingly so, given that US-Chinese bilateral trade has historically accounted for a third to a half of the US trade deficit over the past decade.

Distractions aside, the USD surplus has disappeared

Protectionism is a major risk factor to monitor because it threatens to materially cut the size of the US trade deficit. While this is notionally a positive for US growth, it is also a major shock to USD liquidity in offshore markets. US growth and USD liquidity are the flipside of one another by definition of the balance of payments.

But even before we get to the threat of protectionism, there is still the risk that USD liquidity dries up because of other developments. In this context, talk of protectionism distracts us from some worrying trends beneath the surface.

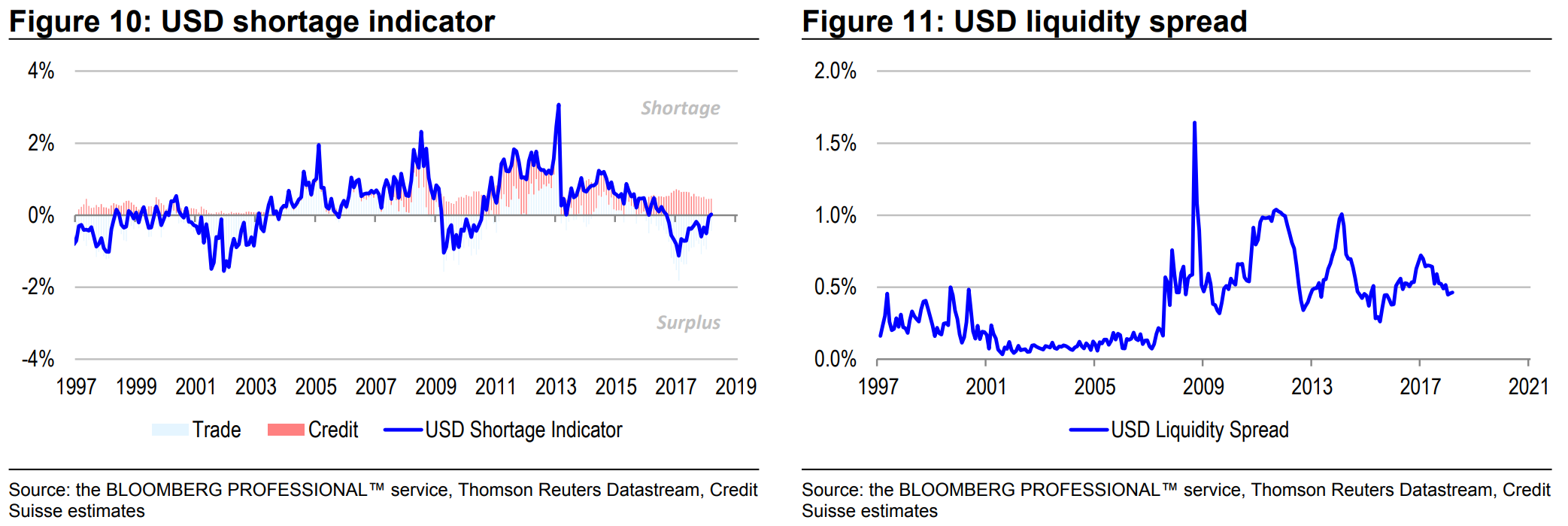

We have constructed a forward-looking measure of the marginal availability of USDs in offshore markets using trade and credit data. Our USD shortage indicator is defined as the sum of:

1. A USD liquidity spread.

2. The prospective change in the “core” (non-petroleum) trade balance based on a simple macro model.

By defining the indicator in this way, we are able to capture shifts in USD liquidity due to credit and trade developments.

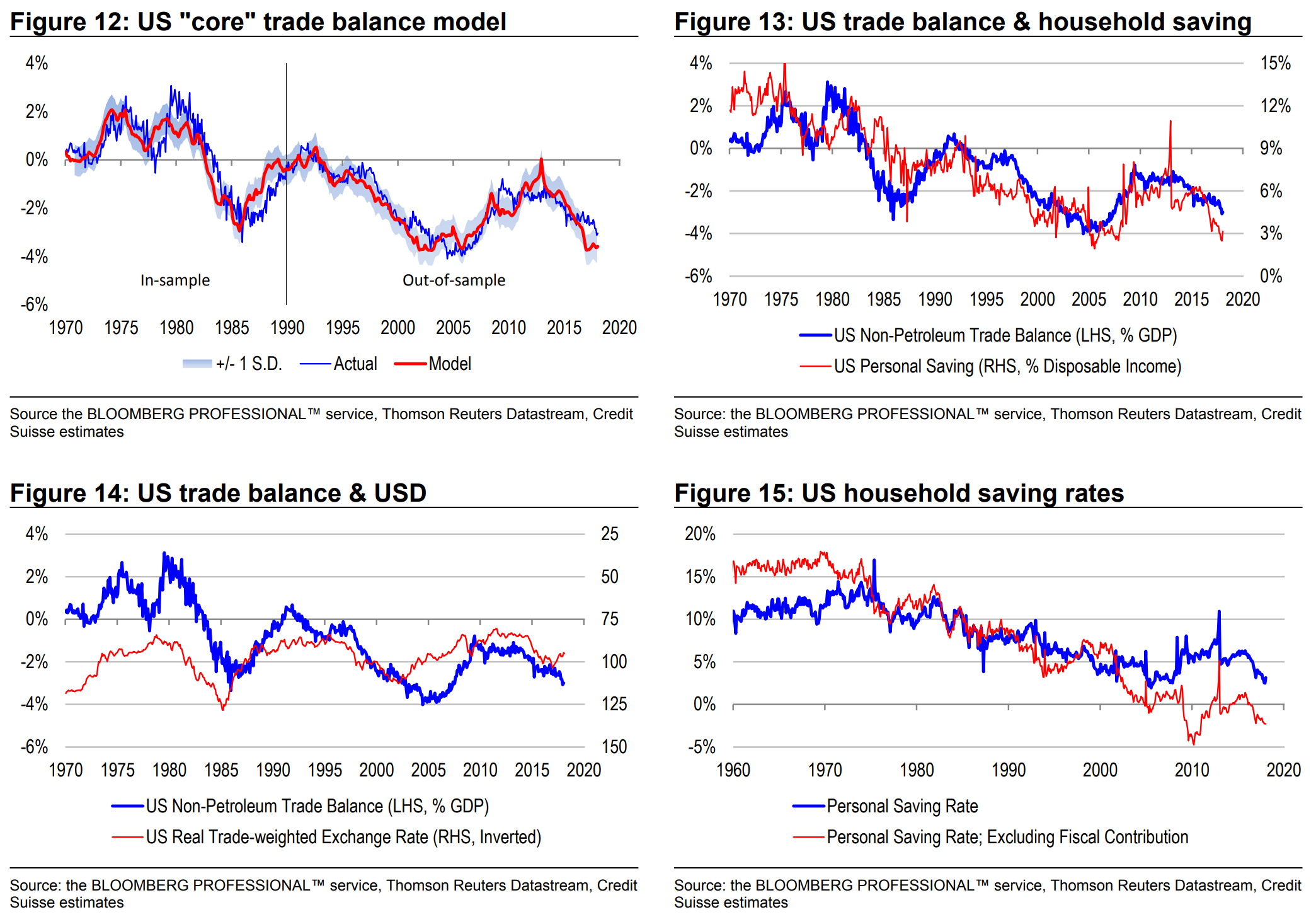

1. US saving rates: Higher (lower) saving rates tend to cause the trade balance to increase (decrease), because they result in weak (strong) consumption and weak (strong) demand for imported products. We allow for the fact that government deficits create deposits which mechanically show up as additional household saving (because someone has to hold cash at the end of the day). Our saving rate is a blend of the raw household saving rate and the saving rate removing the fiscal contribution.

2. The US trade-weighted real exchange rate: A stronger (weaker) real exchange rate tends to make US exports less (more) competitive relative to US imports, contributing to a lower (higher) trade balance.

Model parameters are statistically significant and correctly signed. Importantly, they are also very stable through time, as evidenced by strong out-of-sample forecasting performance since 1990. In terms of causation, our model projection of the “core” trade balance tends to lead the actual balance by several quarters. All of these properties allow us to make reasonably accurate projections of prospective trade balance shifts over horizons of up to a year.

In 2017, our USD shortage indicator was in surplus territory. This was largely because of trade developments. The US trade deficit was simply too narrow relative to fundamentals and susceptible to widening. Prospective widening would increase USD liquidity to the broader world via trade. As it turned out, the trade deficit did widen materially over the year. Indeed, the resulting additional supply of USDs from trade effectively nullified some of the tightening that was occurring in money markets due to other developments (previously discussed by our global expert Zoltan Pozsar—please see our recent article “Unusual money market tightening” dated 12 March 2018 for a summary of his thesis).

In early 2018, this surplus has disappeared. Liquidity spreads are threatening to widen, starting with local-currency, interbank credit spreads. And the US trade deficit could peak soon, limiting the marginal supply of USDs being offered through trade. To be sure, we are not yet in outright shortage territory—but it would not be hard to see how a shortage could occur if the Fed continues to shrink its balance sheet, with a host of unintended consequences now that the system has been replumbed. Indeed, tightening is likely to occur via this channel, even before we see the effects of tax reform and protectionism on offshore USD supply.

On a more positive note, it is possible that USD liquidity increases if US twin deficits (fiscal and trade) expand materially. But it is not a given that larger US fiscal deficits will necessarily boost the trade deficit, especially if households choose to ramp up their saving in the interim.

Investment implications

Over the past few years, the International Monetary Fund (IMF) has been very focused on global imbalances, while the Bank for International Settlements (BIS) has been focused on offshore USD liquidity: 1. IMF on global imbalances: Fund officials have spoken at length about the risks of a sharp unwinding of imbalances that have built up over time, whether expressed in terms of current account balances or leverage. Arguably, the US trade deficit is at the forefront of these imbalances.

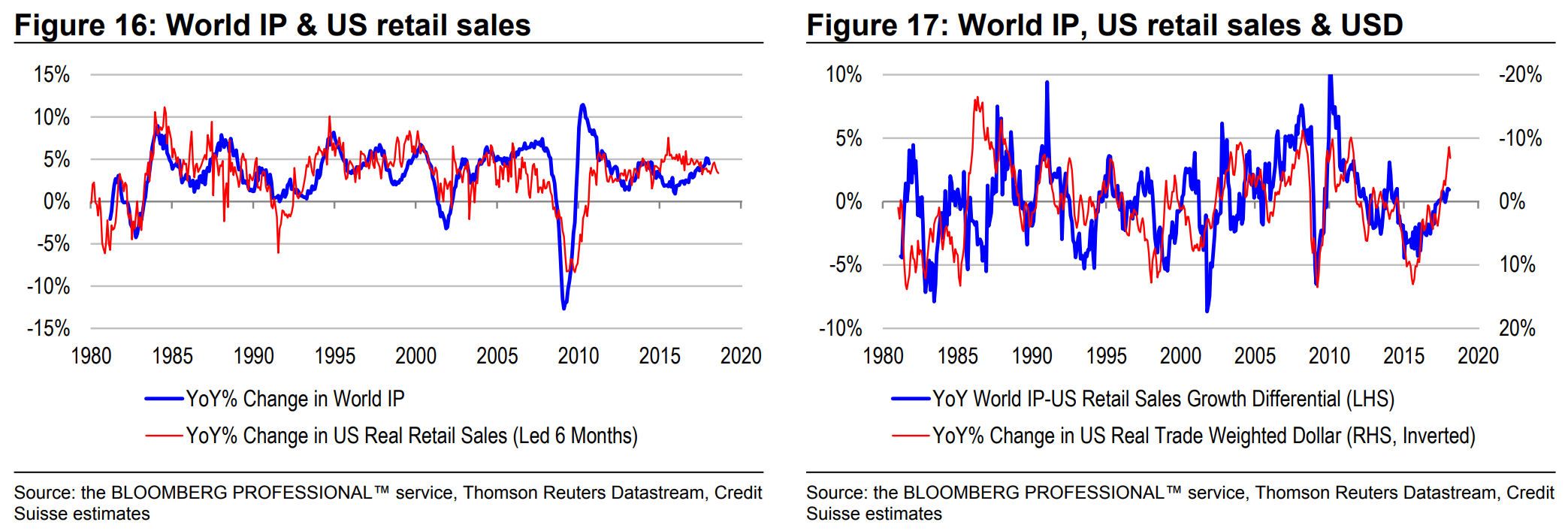

2. BIS on USD offshore liquidity: Bank officials have conducted extensive research into the effects of USD movements on balance sheets, trade finance and supply chains. Their starting point is that the Western consumer is the buyer of last resort of goods and services produced globally. Consistent with this intuition, world industrial production (IP) growth has a robust one-for-one relationship with US retail sales, suitably led. But it is possible that global supply can undershoot (overshoot) consumer demand if the USD strengthens (weakens). This is because USD strength (weakness) can cause US banks to become less (more) willing to extend their balance sheets to foreign entities. In turn, trade finance could shrink (expand), causing global supply chains to shrink (grow) disproportionately. Reflecting this logic, the deviations between world IP and US retail sales are inversely correlated with USD movements through time.

In this article, we have demonstrated the relationships between global imbalances and USD liquidity with the Australian market. And in the way we have constructed our offshore USD shortage indicator, we have effectively spoken to both the IMF and BIS schools of thought. Our shortage indicator takes into account prospective movements in global imbalances via the US trade deficit, and market shifts in USD liquidity via interbank and cross-currency basis swap spreads.

We find it significant that the marginal USD surplus, which supported world growth and commodity prices in 2017, has disappeared in early 2018. This is even before we have considered the threat of protectionism. If the trend continues, it is quite easy to see how an offshore USD shortage might emerge, to the detriment of the Australian economy and markets. We are particularly concerned about the collateral damage on commodity and housing demand. The risks make us cautious about cyclical and financial exposures. We prefer high-quality industrials (many of which, just so happen to have USD-denominated earnings).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Interestingly, there is a reasonably strong and positive correlation between the size of the US trade deficit and Australian equity market performance, whether measured in price or earnings terms. To explain this correlation, several linkages come to mind: