A drop in global share prices of nearly 10% raises concerns about an end to the bull-run and increased volatility. No new domestic economic data of significance has been released since last months’ round. Domestic CPI inflation at 1.9% remains below the Reserve Bank of Australia’s official target band 2-3%, unemployment stands at 5.5%. The RBA Shadow Board rules out any likelihood that a reduction in interest rates could be called for. Instead, it attaches a 55% probability that holding interest rates steady at 1.5% is the appropriate setting, while the confidence in a required rate hike increased to 45%. There is a clear shift in the Board’s assessment in favour of higher interest rates, which also reflected in the six-month and 12-month recommendations.

The latest ABS figure has Australia’s seasonally adjusted unemployment rate at 5.5% in January. Total employment rose by 16,000 but full-time employment fell by nearly 50,000. The participation rate in January stood at 65.6%. The latest figures still put nominal wages growth at 2.1%, implying real wage growth continues to stagnate.

The Aussie dollar, relative to the US dollar, after its recent peak has fallen to around 78 US¢. Yields on Australian 10-year government bonds have fallen again slightly in March, to approximately 2.7%. After a gradual tilting up of the yield curve, the recent fall in the long-term interest rate may reflect heightened uncertainty in the wake of the global stock market rout. The local stock also suffered losses, albeit less than elsewhere, with the S&P/ASX 200 stock index’s dropping below 6000.

Continued attention will be directed at the global stock markets: losses of nearly 10% from recent peaks and greater volatility raise the spectre of further losses and even a bear market. If this were to occur, corporate and household balance sheets – saddled with historically large debt – would strain and a financial crisis, followed by recession, are a real possibility. This scenario contrasts with the recent optimism captured in the forecasts of international organizations such as the IMF and the World Bank. Geopolitical tensions remain currently remain contained.

Business and consumer indicators have barely budged and there is no new data providing a clearer direction for the housing market.

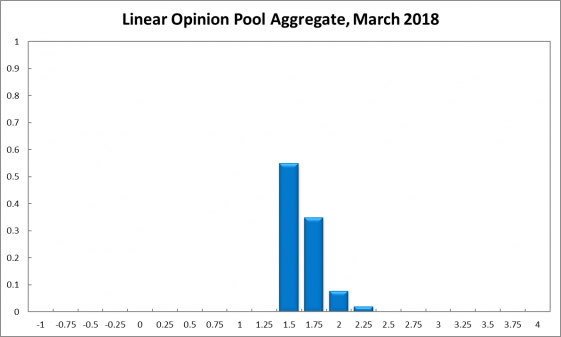

Since the last round in February 2017, the distribution of the Shadow Board’s policy preferences has strengthened in favour of an interest rate increase. The Shadow Board is 55% confident that keeping interest rates on hold is the appropriate policy, 8% higher than one month ago. It attaches zero probability that a rate cut is appropriate (unchanged) and a 45% probability (37% in February) that a rate rise, to 1.75% or higher, is appropriate.

The probabilities at longer horizons are as follows: 6 months out, the estimated probability that the cash rate should remain at 1.50% equals 23%, one percentage point lower than in February. The estimated need for an interest rate decrease is 4% (5% in February), while the probability attached to a required increase equals 74% (71% in February). A year out, the Shadow Board members’ confidence that the cash rate should be held steady equals 15% (14% in February), while the confidence in a required cash rate decrease equals 3% (4% in February), and in a required cash rate increase 82% (up 1% from February).

As much as I’d love to see it there’ll be no hike today nor ever again. Next move down.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.