The Grattan Institute has published a detailed report in Inside Story rubbishing Treasurer Scott Morrison’s “deeply misleading” claim that 54% of people affected by Labor’s proposed dividend imputation policy — some 610,000 individuals — have taxable incomes of less than $18,200.

Grattan’s key bone of contention is that “taxable income” ignores the largest source of income for many wealthier retirees – tax-free superannuation – and few (if any) of Scott Morrison’s 610,000 so-called “low income earners” affected by the policy are maximum rate pensioners:

Take the example of a self-funded retiree couple with a $3.2 million super balance, plus their own home, and $200,000 in Australian shares held outside super. Even drawing $130,000 a year in superannuation income, and $15,000 a year in dividend income, they would report a combined taxable income of just $15,000, and pay no income tax whatsoever.

And is the treasurer seriously suggesting that 610,000 retirees actually get by on less than $18,200 a year, or nearly 20 per cent below the poverty line? If that were anywhere close to the real story, it would signal a full-blown retirement-incomes crisis…

A single retiree receiving the full age pension has an income of $23,318 a year, and more if they earn extra income in dividends from shares. All this income would show up as taxable income if they submitted a personal income tax return — as required to claim refundable imputation credits.

Advertisement

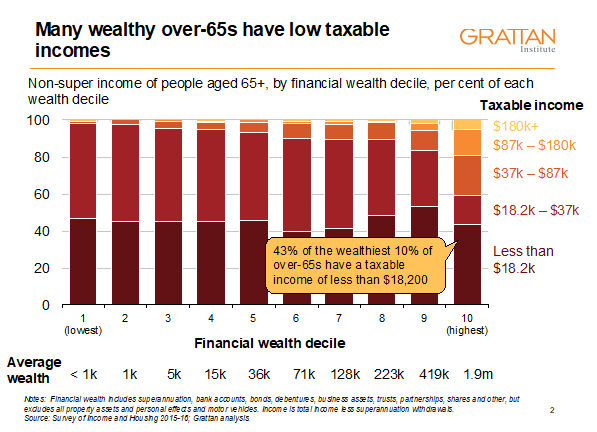

Grattan also notes that most of those affected by Labor’s policy who declare taxable incomes of less than $18,200 a year are in fact drawing much of their income from tax-free superannuation. In fact, even among the wealthiest 10% of retirees, almost half would report taxable incomes of less than $18,200 a year, despite having average financial assets of almost $2 million – and that’s without considering any property assets (i.e. owner-occupied or investor dwellings). Therefore, “many retirees who report having very low incomes in retirement have substantial retirement nest eggs”.

The fact of the matter is that it is primarily the wealthy that will be impacted by Labor’s dividend imputation policy, according to Grattan:

Around 33% of the extra tax from Labor’s policy will be paid by (mainly wealthy) individuals who own shares directly, 60% will be paid by self-managed superannuation funds (typically held by wealthier retirees), and the remaining 7% will be paid by super funds regulated by APRA.

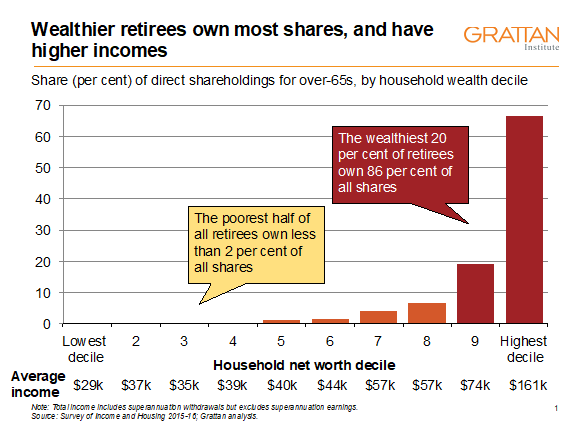

Among individuals, the poorest half of all retirees own less than 2% of all shares held directly. By contrast, the wealthiest 40% of retirees own 97% of all shares held directly, and the wealthiest 20% alone own 86% of all shares held directly.

Advertisement

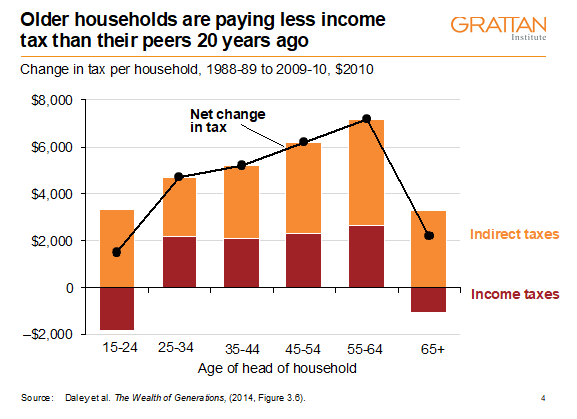

Finally, Grattan notes that Australia’s superannuation and tax system remains absurdly generous to older Australians, with older Australians paying less in tax today than they did 20 years ago, despite higher workforce participation and incomes, and the proportion of seniors paying tax almost halving in 20 years, from 27% in 1995 to 16% in 2014:

Advertisement

This is an excellent report that comprehensively debunks Scott Morrison’s lies.

Meanwhile, Labor is moving on the small adjustments needed to eliminate any losers, via the AFR:

Labor is leaning towards exempting low-income pensioners from its policy to scrap franking credit refunds, to head off a backlash from retirees and take the sting out of a growing campaign by the Turnbull government.

While no final decision has been made, the most likely option will be to adopt a proposal similar to that being pushed by Industry Super Australia, which suggested a change to allow up to to $1000 in cash refunds to an individual.

Exempting all pensioners would only cost about $238 million of the estimated savings in the first year of $5.6 billion.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.