The Conversation yesterday published a ripper series of charts on Australia’s private health insurance system, which illustrates the strong inflation in premiums that has taken place over the past 15-plus years.

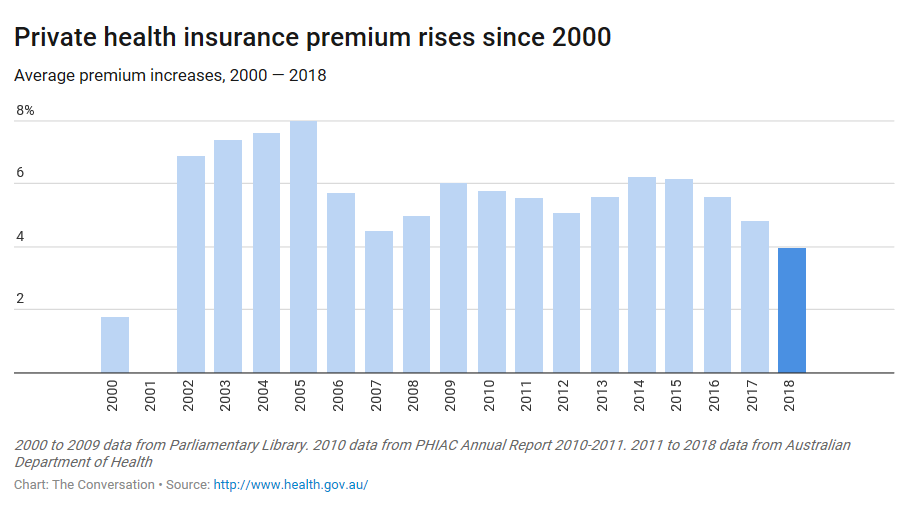

For mine, the key charts are below, namely the annual percentage increase since 2000:

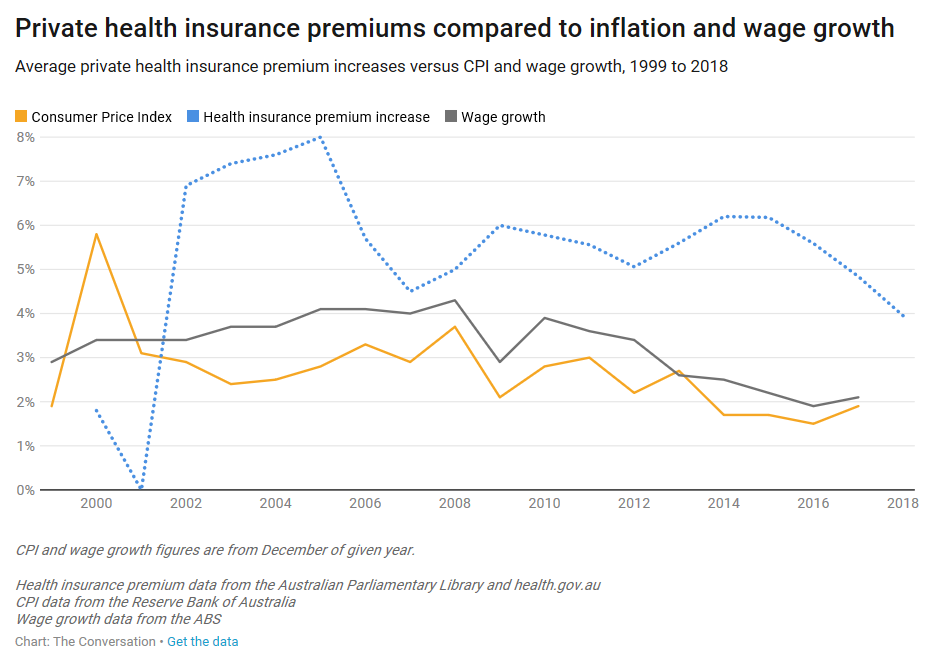

Premium rises relative to wages growth:

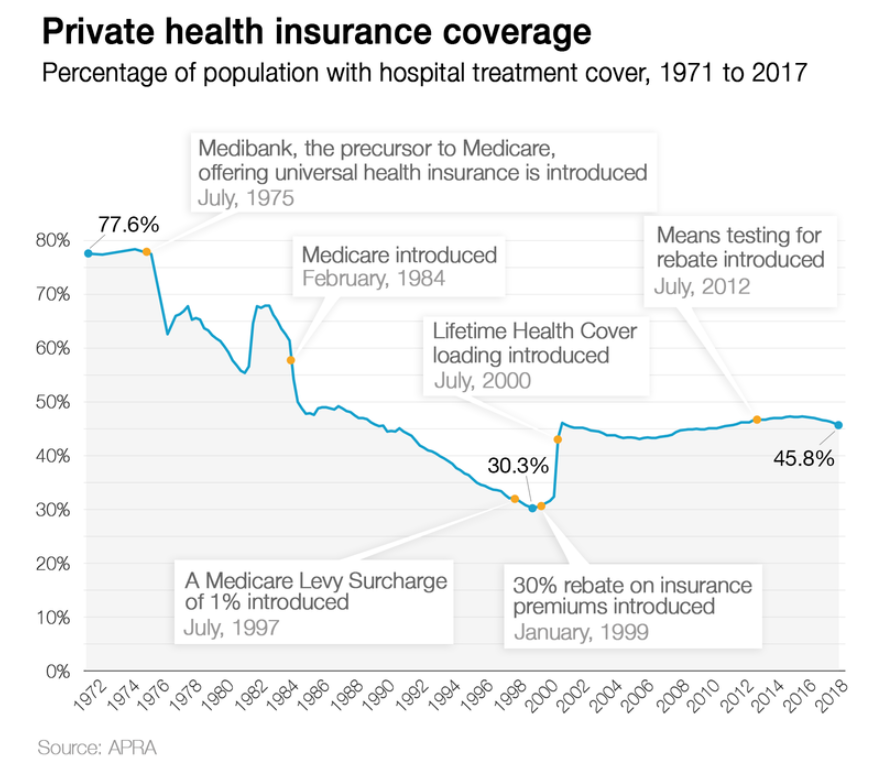

Private health insurance coverage:

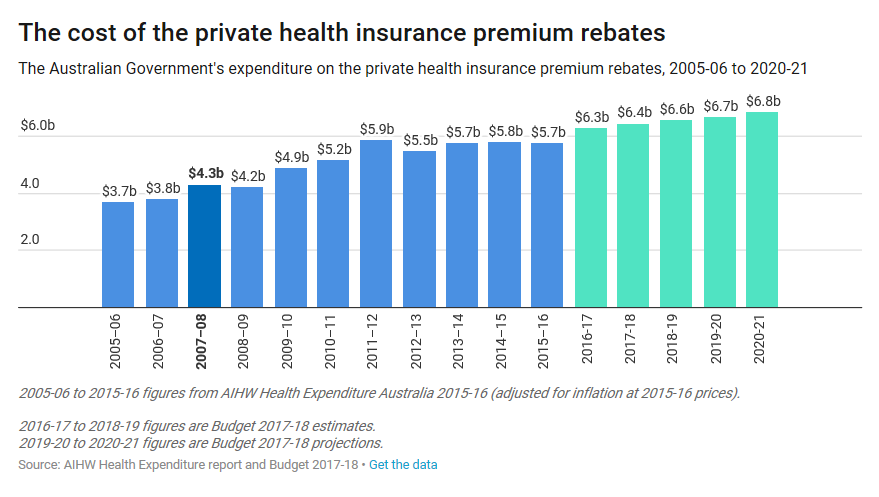

The huge and growing cost to the federal budget:

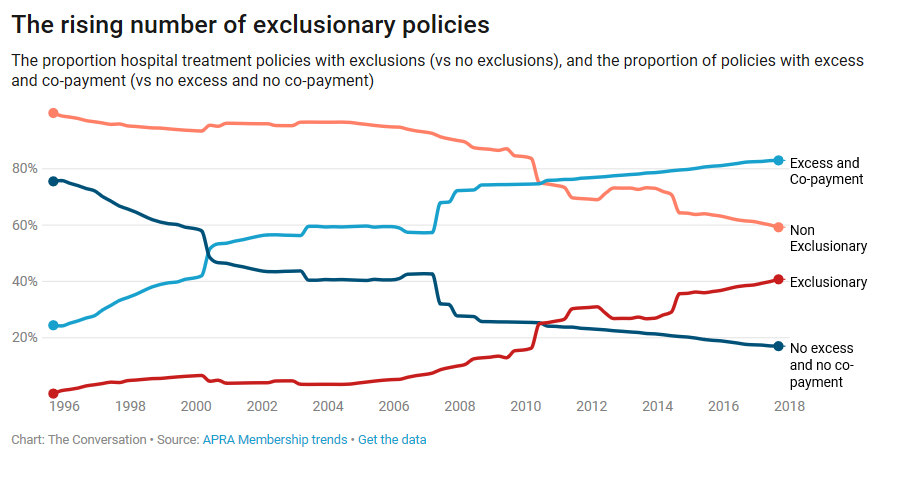

And the growth in exclusionary policies:

When viewing the above charts, one immediately has to question whether Australia’s private health insurance rebate system is a form of corporate welfare in disguise?

That is, since the Howard Government introduced its “Lifetime Health Cover” policy in July 2000 – effectively forcing Australians to take out private health insurance – premiums have ballooned despite the massive cost to the Budget (rising from $3.7 billion in FY06 to a projected $6.8 billion in FY21), and the huge growth in policy exclusions and co-payments for treatment.

One could credibly argue that Australia’s Lifetime Health Cover policy is working more for the benefit of the private industry players than the public good by providing a steady source of members compelled to take out insurance against their will, which the industry can effectively ‘clip the ticket’ and earn profits without improving service.

Every year, the Australian Competition and Consumer Commission (ACCC) releases its report to the Australian Senate on competition and consumer issues in the private health insurance industry. And every year, the ACCC finds that Australia’s private health insurance industry is characterised by market failures due to asymmetric and imperfect information, as well as significant complexity.

Accordingly, consumers are viewing private health insurance as poor value for money.

There is no evidence that private health insurance buys patients extra quality and safety. The Productivity Commission (PC) found that the larger, most comparable public and private hospitals had similar adjusted premature death ratios. Further, the PC found that the team-based care in large public hospitals also leads itself to better coordination of care.

In fact private health insurance might even raise overall Australian health costs. This is because the high financial overhead of private insurance means that only 84 cents in every dollar collected by private insurers is returned as benefits, with the rest going to administrative costs and corporate profits. By contrast Medicare returns 94 cents in the dollar, even after the cost of tax collection is taken into account.

With the costs of private health insurance rebate climbing, it’s time Australia had a national debate about the efficacy of the private health insurance system and whether we should abandon subsidies and shift towards a single national insurer.