In June last year, the Reserve Bank of New Zealand (RBNZ) launched consultation to have debt-to-income (DTI) limits added to its macro-prudential toolkit.

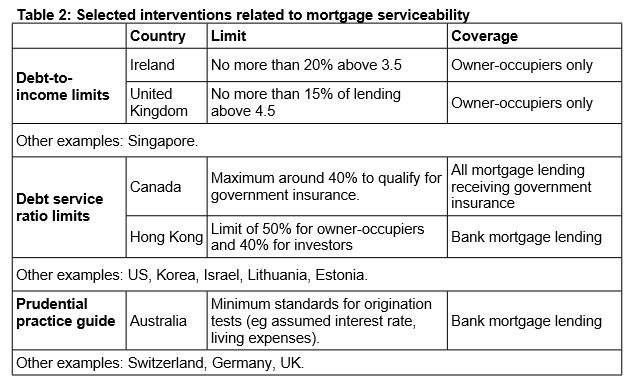

In the consultation paper, the RBNZ proposed a DTI limit of 5.0 times incomes and noted that DTI limits are used in other markets around the world, including the UK, where borrowers must have a loan no bigger than 4.5 times their income. However, the RBNZ cautioned that such a limit could significantly crimp housing demand and sales volumes, as well as trim prices.

According to the RBNZ:

All else equal, high DTI ratios increase the probability of loan defaults in the event of a sharp rise in interest rates or a negative shock to borrowers’ incomes. As a rule, borrowers with high DTIs will have less ability to deal with these events than those who borrow at more moderate DTIs. Even if they avoid default, their actions (e.g. selling properties because they are having difficulty servicing their mortgage) can increase the risk and potential severity of a housing related economic crisis…

The Reserve Bank believes that the use of DTI limits in appropriate circumstances would contribute to financial system resilience in several ways:

– By reducing household financial distress in adverse economic circumstances, including those involving a sharp fall in house prices;

– by reducing the magnitude of the economic downturn, which would otherwise serve to weaken bank loan portfolios (including in sectors broader than just housing); and

– by helping to constrain the credit-asset price cycle in a manner that most other macroprudential tools would not, thereby assisting in alleviating the build-up in risk accompanying such cycles…The focus would be systemic: on reducing the risk of the overall mortgage and housing markets becoming dysfunctional in a severe downturn, rather than attempting to protect individual borrowers…

DTIs on loans to New Zealand borrowers have risen sharply over the past 30 or so years, with further increases evident since 2014… average DTIs in New Zealand are quite high on an international basis, as are New Zealand house prices relative to incomes…

In his outgoing speech on Tuesday as acting RBNZ Governor, Grant Spencer said that a DTI ratio should be given serious consideration in the upcoming review of the Reserve Bank Act:

Macro-prudential policy has been particularly useful in the current environment of globally low interest rates, where monetary policy has been unable to counter the strong housing cycle of recent years…

I am keen to see macro-prudential continue to develop as a credible and sustainable policy over the longer term…

I believe that the review should look at whether we have the most appropriate macro-prudential framework for New Zealand circumstances, and what role other macro-prudential instruments could play to enhance and/or complement LVR restrictions…

While having limited scope to sustainably influence credit and asset price cycles, macro-prudential policy has significantly improved the resilience of banks’ balance sheets to any downturn in the housing market…

The IMF’s recent Financial Sector Assessment Programme (FSAP) benchmarked the New Zealand macro-prudential framework against their view of emerging best practice.7 The report noted approvingly the Bank’s clear mandate for financial stability, independence of the Bank’s decision-making process, and a demonstrated willingness to act. Key recommendations of the report were to further clarify the respective roles of the Bank and the Minister when considering variations to the framework, such as inclusion of a debt to income (DTI) instrument in the toolkit, and to continue to enhance accountability mechanisms…

Regarding the contents of the policy tool-kit, the mix of instruments should slowly evolve through time. In the present economic and financial environment I support retention of the four instruments listed in the MOU (LVRs, CCB, CFR, SCR) and the addition of a carefully designed debt to income (DTI) or debt servicing instrument. You will recall that the Bank consulted on including a DTI instrument in the toolkit last year. That process was overtaken by the general election and a decision on inclusion or otherwise was deferred to the upcoming Macro-Prudential Review. The DTI is a natural complement to the LVR, focused on reducing the risk of borrower default. Many macro-prudential authorities overseas view some form of debt servicing ratio as a key anchor and safeguard for macro-financial stability. The Review should give serious consideration to adding such an instrument to the toolkit.

However, New Zealand Finance Minister, Grant Robertson, yesterday voiced his reluctance to adding a DTI measure to the RBNZ’s macro-prudential toolkit. From Interest.co.nz:

Robertson’s views on adding a debt-to-income (DTI) ratio tool to the Reserve Bank’s macro-prudential toolkit have not changed, despite recommendations from Grant Spencer…

“I have concerns about the impact of DTI ratios on first home buyers – that remains my personal view.”

Despite this, he says this issue will be assessed in the upcoming Reserve Bank Act review and he is waiting to see what comes out of that.

It appears the new Labour-led Government is already back-sliding on promised housing and immigration reforms. Let’s hope it doesn’t stand in the way of DTI controls as well.

Regardless, you’ve gotta respect the RBNZ for always being on the front foot and actively attempting to temper housing risks, which is far more than I can say for the dunces at APRA/RBA, whose modus operandi is ‘soft touch’ (or ‘wet lettuce’).