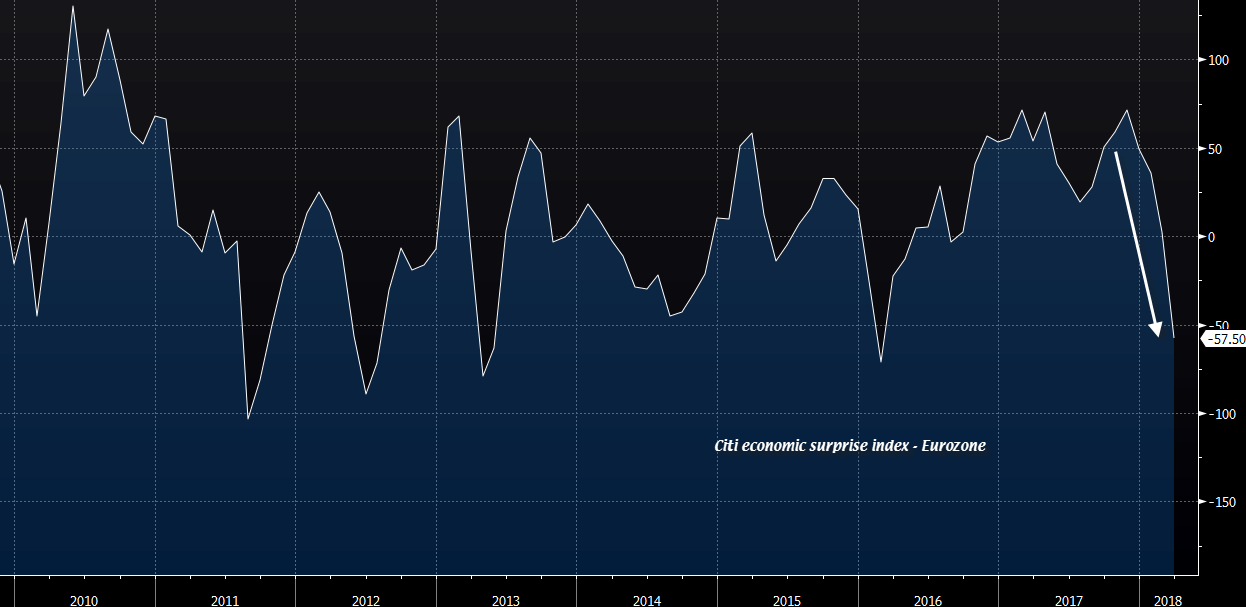

Here’s the chart to lead us off:

That’s what a tearaway currency will do to you. Now other components of European boomlet are on the turn, via Westpac:

With the benefit of hindsight, we believe that 2017 will be seen as this cycle’s peak year for Euro Area growth. Against the 2.5% year-average outcome for 2017, we foresee growth of 2.1% in 2018 then 1.6% in 2019. While a little more optimistic, the ECB has a similar view, expecting growth of 2.4%, 1.9% and then 1.7% in 2018, 2019 and 2020 respectively.