Business conditions continued to improve across China’s manufacturing sector in February. Although growth in production softened from that seen in January, total new work expanded at a slightly faster pace. Meanwhile, companies continued to shed staff as part of efforts to reduce costs, which contributed to a further rise in the level of outstanding work. Although the rate of input price inflation eased further in February, it remained sharp overall and remained much stronger than that seen for output charges. Business sentiment remained strongly positive in February, with the degree of optimism reaching an 11-month high.

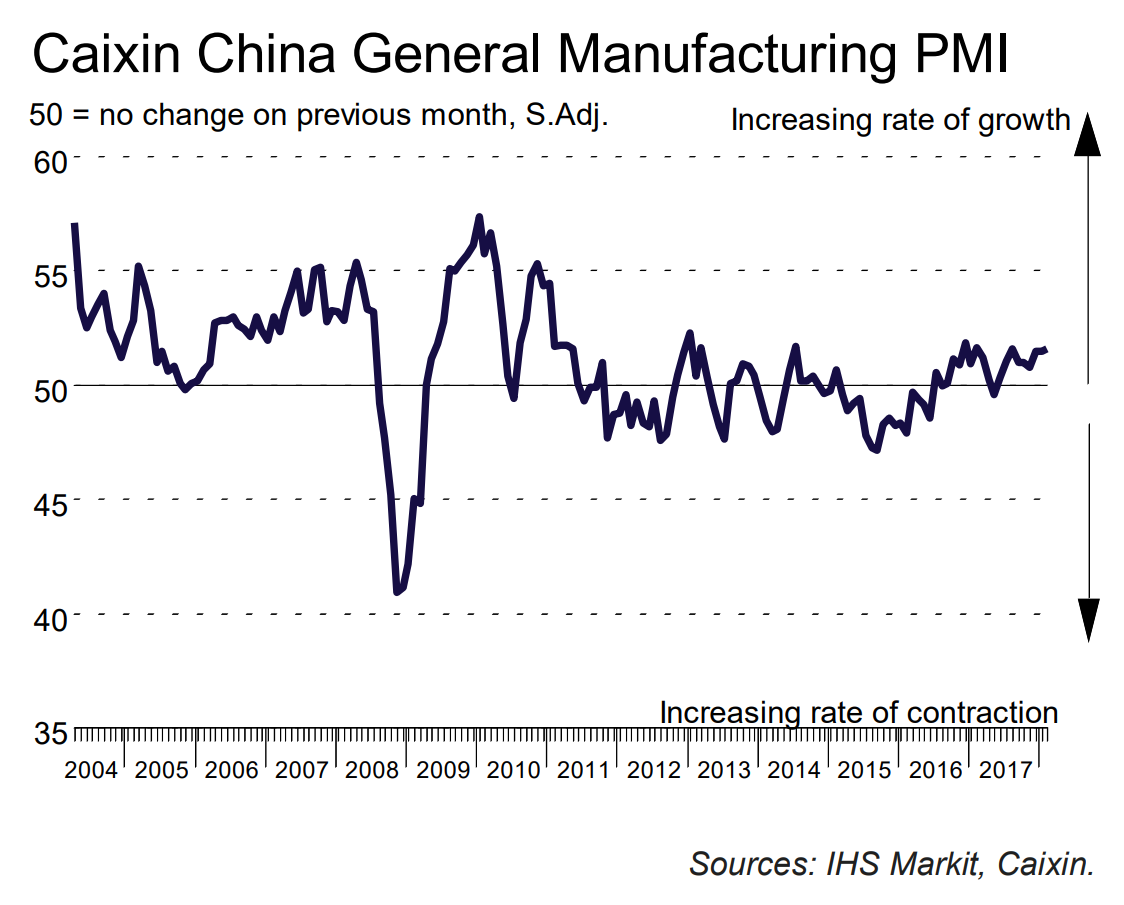

Adjusted for seasonal factors, including the Chinese New Year, the headline Purchasing Managers’ Index™ (PMI™) – a composite indicator designed to provide a single-figure snapshot of operating conditions in the manufacturing economy – edged up to 51.6 in February, from 51.5 in January, to signal a further improvement in the health of the sector. Though only modest, the latest reading signalled the strongest improvement in operating conditions for six months.

Manufacturing output in China continued to rise in February, albeit at a modest pace that was slightly softer than seen at the start of the year. According to panellists, production volumes rose due to greater amounts of new work. In contrast to the trend for output, growth in new orders quickened since January. This was despite new export sales rising to the softest extent for three months.

February data signalled a further drop in Chinese manufacturing employment as a number of firms sought to reduce costs through the implementation of down-sizing measures. Despite quickening slightly since January, the rate of job shedding remained marginal, however. Reduced staffing levels and higher new orders led backlogs of work to accumulate again, albeit at a weaker pace than seen at the start of the year.

Purchasing activity continued to increase in February, albeit modestly. Nonetheless, the sustained increase in buying activity underpinned the fastest rise in stocks of purchases for just over a year-and-a-half. Inventories of finished items also rose in February, following an eight month sequence of decline.

The amount of time taken for inputs to be delivered to manufacturers continued to increase, albeit modestly, with some reports linking delays to poor weather conditions.

Input prices continued to rise sharply, despite the rate of inflation easing to a seven-month low. Panellists widely attributed greater cost burdens to higher raw material prices. As a result, firms raised their selling prices again in February, albeit at a modest rate that was similar to that seen in January.

Finally, business confidence strengthened to its highest level for nearly a year in February. Positive expectations towards the 12-month outlook were widely supported by upcoming product releases and expectations that client demand will continue to improve over the year ahead.

As said many times, expect these things to be noisy through the first half but trend down.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.