Senate leader Mathias Cormann yesterday conceded the government “will need to do some more work” to get the two more votes it needs, and said the Enterprise Tax Plan Bill would be shelved until budget week.

…The government had been optimistic on Sunday about passing the tax-cut bill this week, but cooled expectations on Monday as negotiations dragged out with crossbenchers Derryn Hinch and Tim Storer.

The government needs 39 votes to pass the bill, but has only 37. Senator Cormann said he believed the government could still secure the votes it needed.

Rob Burgess does some better work today on why this is a good outcome:

Company tax is really a ‘withholding tax’. It lets the Australian Tax Office hang on to the money until it knows who’s receiving the company profit in the form of dividends.

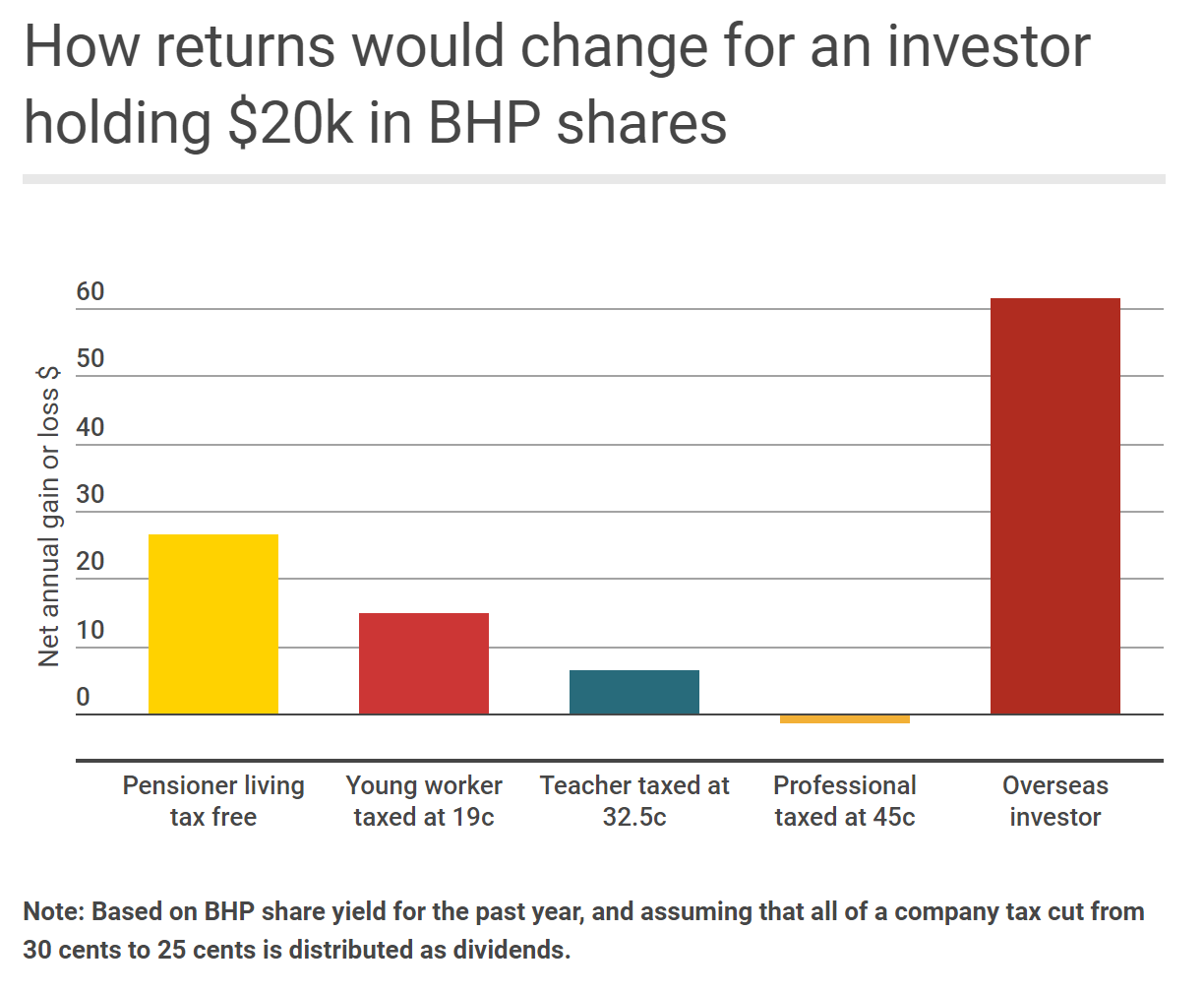

If the recipient is an Australian resident, the ATO looks at their marginal tax rate to work out whether they owe more or less than 30 cents in the dollar.

If the recipient is a pensioner living tax-free, the entire 30 cents is refunded via the franking credits process, and for income earners higher up the tax scale part, or none, of that 30 cents is handed back.

If the recipient is an overseas investor, the ATO just keeps the entire 30 cents.

The Coalition’s tax cut policy has already been legislated for companies turning over less than $50 million a year – their rate has been reduced to 27.5 cents, and will eventually be lowered to 25 cents.

The government now desperately wants to pass the remaining tax cuts for bigger businesses, so that they would see phased cuts until they too got to 25 cents by 2026.

Most of those bigger companies are listed on the Australian Securities Exchange, and on average about 50 per cent of their shares are owned by overseas investors.

So Senator Hinch needs to understand that the owners of half the shares listed on the ASX would do very well from the planned cut, but other shareholders less well – as the chart below shows.

Advertisement

So, it’s largely a tax cut for foreign shareholders. But it gets much worse.

As the secret BCA research showed yesterday, the tax cuts will do very little to trigger investment, employment or wage gains, via the AFR:

Fewer than one in five of Australia’s leading chief executives say they will use the Turnbull government’s proposed company tax cut to directly increase wages or employ more staff, according to a secret survey conducted by the Business Council of Australia.

More than 80 per cent said they would either use the proceeds to boost returns to shareholders or invest in the company.

Advertisement

This is consistent with what we’re seeing in the US with the Trump tax cut which is largely being used for capital management purposes. A much better idea is to offer the accelerated writedowns that both Trump and Labor are using which will effectively cut taxes for those that do invest.

Finally, why on earth would we be cutting company taxes just as we re-enter the Chinese structural slowing and correction in our terms of trade, not to mention the end-of-cycle shock? This is the time to be stacking away the acorns for the coming bust not dishing them out as corporate welfare. This context means that any tax cut today will have to be retrieved at the worst possible time tomorrow. This is why the RBA is against the cut.

So, both structural and cyclical considerations make this bad policy.

Advertisement

The final point to make for our hold-out senators is this: they are there to represent the national interest and trading that away for beads and trinkets is not in the job description.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.