For all the negative sentiment towards bonds in the marketplace (eg because of inflation, or policy tightening concerns), it is interesting to note that in China, and in Australia, equities have actually underperformed bonds year-to-date.

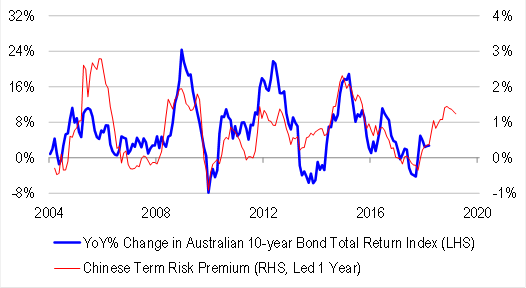

In a previous article (attached), we argued that these developments are no coincidence. The so-called term risk premium in Chinese bonds is one of the single best leading indicators of annual Australian 10-year bond returns. Over the past year, the Chinese risk premium has become much more positive, as policy makers have hit liquidity constraints under the pegged exchange rate regime. Not only has this made Chinese bond valuations more attractive, but illiquidity is now also having negative flow-on effects on the Australian economy via resources and housing sectors, and is contributing to lower Australian yields as well.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.