Via Bill Evans:

The Reserve Bank Board meets next week on March 6. Of course we expect there will be no change in the overnight cash rate.

We also do not expect to see any significant change in the Governor’s rhetoric from last month.

The GDP Report for the December quarter – which we expect will show that annual growth has slowed from 2.8% in the year to September to 2.5% – will not print until March 7 and although the Bank will be anticipating a soft result, this is unlikely to dissuade it from its current view that GDP growth in 2018 will lift to 3.25%.

Readers should be aware that Westpac has reviewed its currency forecasts and, while continuing to see an AUD low of USD 0.70 in 2019, has pushed out the timing to September 2019 from March.

Below I set out detailed reasoning behind our AUD views.

We expect to see the AUD gradually fall through 2018 and 2019 against the USD.

The AUD is likely to hold around USD 0.77 to June before falling to USD 0.74 by year’s end.

In 2019 it is expected to reach USD 0.70 by September and to hold around that level to year’s end.

These forecasts broadly reflect our Fair Value model after making some adjustments for our own judgements particularly around capital flows that may not be fully explained by commodity prices and interest rates.

The key drivers behind our views are: a fall in Australia’s commodity export prices, and an unprecedented sharp negative widening in the AUD/USD interest rate differential as US rates rise sharply. Furthermore, we anticipate a reversal of the current trend for the USD to weaken against the other majors.

The key to commodity prices lies with China. China’s Chairman Xi recently identified pollution; poverty and excessive leverage as China’s key policy challenges.

Our commodity price views have been based around the expected slowdown in China’s credit growth (particularly in the unregulated so-called shadow banking sector) firstly squeezing commodity speculators who currently hold substantial stocks of iron ore and secondly slowing investment particularly in major transport projects. These projects are typically associated and funded by local governments, usually outside the regulated banking sector. They place considerable reliance on funding from the shadow banking system. In addition, housing activity, which also partly relies on the shadow banking sector, looks set to remain quite flat over the next few years.

While these are clear factors which are likely to weigh on commodity prices, China’s anti-pollution policies have been supporting iron ore and coking coal prices. Small high polluting mines/furnaces have been closed down with some production moving to larger more efficient operations. These larger producers have been using a higher share of quality imported iron ore, effectively holding up import prices despite lower production.

The dominant iron ore exporters – Australia and Brazil – have not been significantly lifting production to take advantage of higher prices and widening margins.

These dynamics will continue to support prices for some time yet.

Nevertheless we expect that over the course of the second half of 2018 and through 2019, the downward pressures associated with a slowing economy and tighter credit conditions in China will gradually take their toll on both iron ore and coal prices.

We would also expect some downward price pressure from a lift in supply from the dominant exporters. Margins remain extremely attractive and we expect producers, particularly the Brazilians (around 30% of the majors’ production) to lift production.

Overall, we are expecting a cumulative fall (in USD’s) in Australia’s Commodity Price Index of around 25% between June 2018 and December 2019. That includes around a 6% appreciation in the USD Index.

The USD Index has been under considerable recent pressure (down 15% from its peak in late 2016 to its low in mid-February). Recently it has lifted by around 2% partly reflecting the sharp rise in US bond rates.

While I was recently in the US visiting real money managers and officials, the common theme was that the recently enacted Tax Cuts and the $300 billion spending package were poorly timed. They coincided with the US economy at full employment and building momentum. The likely resulting inflation pressures and a rising FEDERAL FUNDS RATE were expected to significantly boost bond rates. In turn, higher bond rates are likely to reverse the recent weakness in the USD.

Readers will be aware that Westpac expects a considerable widening in the negative Australia/US interest rate differential as the FEDERAL RESERVE continues to raise rates and the RBA remains on hold.

Markets move on expectations.

They are currently pricing in a yield differential between Australia and the US overnight rates of around negative 50 basis points by end 2018 whereas Westpac expects negative 65 basis points. They are expecting a differential of around negative 30 basis points compared to Westpac’s forecast of negative 112 basis points by end 2019.

Our expected differential in 2019 has no precedent raising the prospect that the downward pressure on the AUD could be under stated in our forecasts.

We anticipate that as markets adjust to Westpac’s rate differential outlook there will be further downward pressure on the AUD. This effect is likely to be more pronounced in 2019 than 2018 with the gap between Westpac’s view and the market narrowing significantly in 2019. Note that only a few weeks ago markets were only expecting a negative differential of 28 basis points by end 2018. They have moved significantly towards the Westpac view. But there is more to come.

Falling commodity prices; widening negative yield differentials and a stronger USD all point to a weaker AUD through the remainder of 2018 and 2019.

Right idea but too bullish in my view. Bulk commodities will fall earlier as China slows. The RBA will be forced to cut on a renewed income shock. AUD down earlier and steeper!

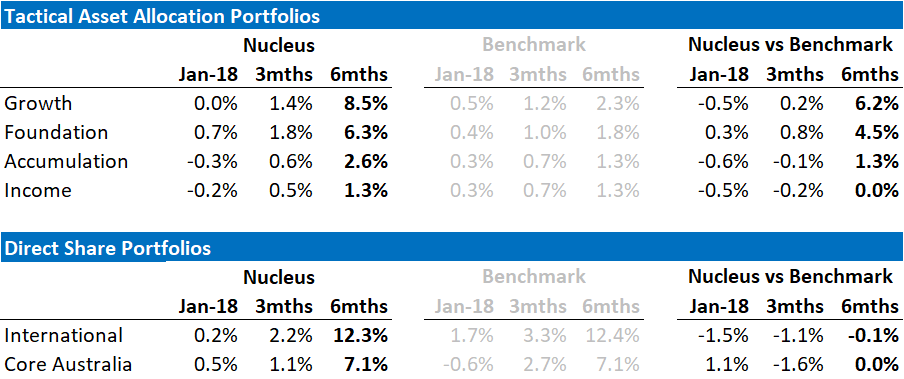

David Llewellyn-Smith is chief strategist at the MB Fund which is currently overweight international equities that will benefit from a weaker AUD so he definitely talking his book. Fund performance is below:

If these themes interest you then contact us below.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.