Hooray, no Trump tariffs:

It was only in the wee hours of Friday morning, when Donald Trump singled out Australia following a cabinet meeting on trade, that the Turnbull government finally felt its lobbying over the past eight months to exempt steel and aluminium from tariffs had succeeded.

More so, because Trump, in all but confirming Australian imports would be exempt, was citing the very same arguments that were first made to him by Malcolm Turnbull and Mathias Cormann on the sidelines of the G20 summit in Hamburg last July, and which had been put to him and members of his administration dozens of times since.

That Australia was one of a few nations with which the US had a trade surplus, that we were a close ally, that unlike others we were pulling our weight militarily in the region, and that Australian companies employ a lot of Americans.

We’re exceptional! $300m saved! Forgotten is that the Trump tariffs have just wiped roughly $10bn from Australian income via crashing iron ore and coking coal prices.

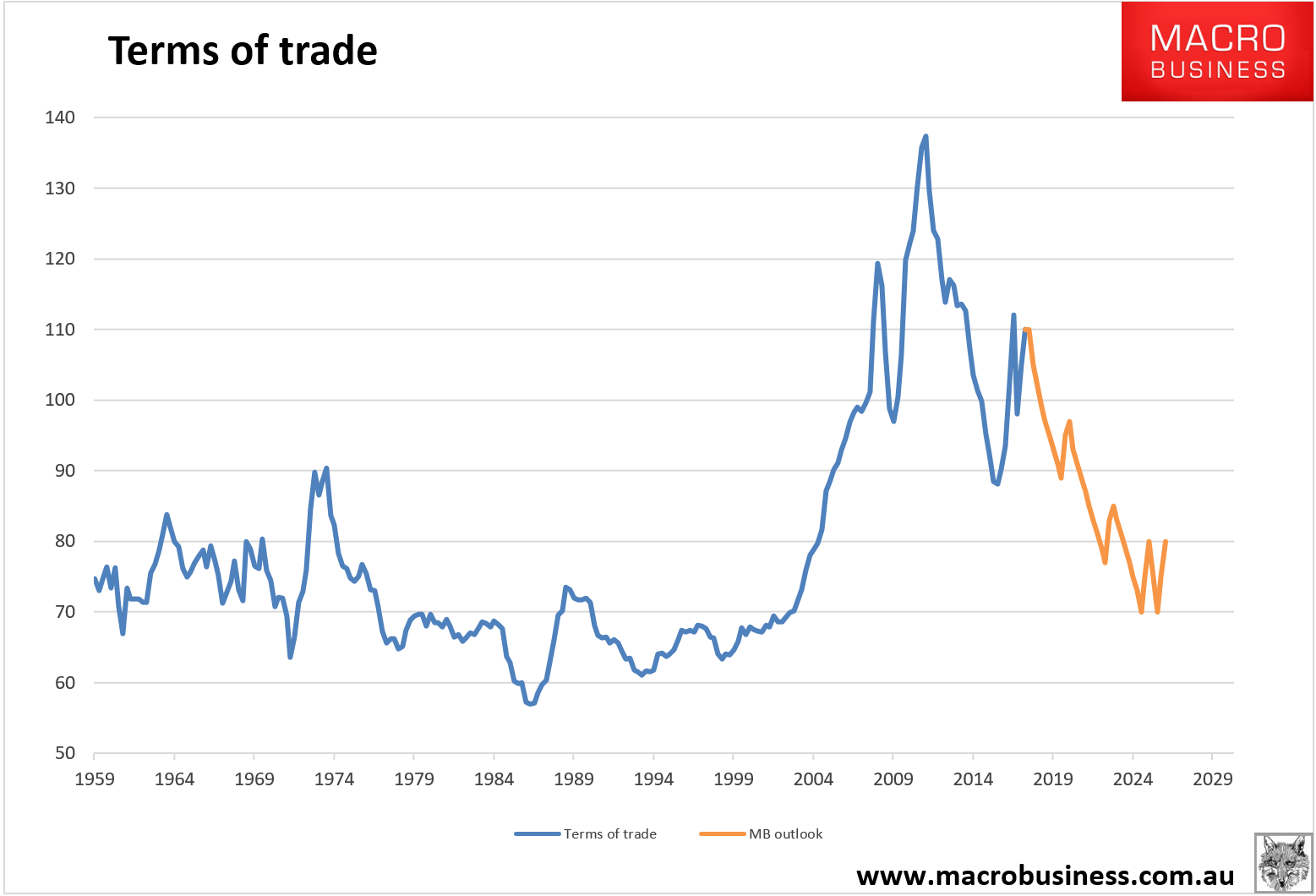

All of Australia’s problems are about to get much worse. The bulk commodities are breaking down as China slows. By the second half they’ll be materially below the Budget outlook. National income will be entering a renewed external shock. The wages crush will intensify. Corporate profits growth will be wiped out and the share market under-performance get much worse. RBA credibility will be in tatters again as it mulls further rate cuts. Political chaos will mushroom as the Do-nothing Government finds its re-election platform of tax cuts for companies and punters running headlong into a structural deficit and sovereign downgrade.

And all of this amid a global boom. How did it come to this? Very simple: our suicidal exceptionalism.

When the mining boom happened, instead of putting away the acorns we declared ourselves exceptional and spent it. Because we are exceptional, we assumed the boom would go forever, and allowed every non-mining tradable not bolted down to be thrown into the sea.

When the mining boom went bust in three years instead of thirty, instead of doing the hard yards to rebuild those tradables we deliberately kicked more into the sea. Because we are exceptional, we manufactured instead our last great housing bubble blowoff, based upon interest-free loans, to paper over the gaping economic wounds.

When that bubble could inflate no further, we turned to back-filling it with mass immigration. Because we are exceptional we mortgaged our successful multiculturalism by dishonestly crush-loading major cities, blowing countless billions upon dis-economies of scale infrastructure. It came with the added bonus of wiping out wages growth.

Which brings us to today. Instead of using a two year reprieve in the falling terms of trade thanks to temporary Chinese stimulus we’re getting set to spend it all again. Only this time it’s disappearing faster and soon we’ll have no money left. But we will have the debt and the big, fat interest-only mortgage rate reset plus the tumbling living standards as infrastructure crumbles.

The suicidal reign of exceptionalism is not yet over even as we face this:

I’ve come to the view that the terms of trade won’t fully revert to the lows of 1990s owing to the increasing role of LNG in the export mix. The sixties period looks a better analogy. But don’t celebrate that. The LNG exports are profitless, so the hollowing out will be worse even than it appears as the gas cartel gouges locally to make up the losses. Worse still, profitless LNG volumes will hold the currency higher than otherwise while bulk commodities keep deflating with Chinese growth.

For any other country this renewed adjustment to wages, house prices, the Budget and the currency might prove quite tough.

But we’re exceptional.