Overnight, the US equity market rallied strongly, more than recovering Friday’s losses, and noticeably outperforming bonds. There was little new news to speak of, but we think the following developments were noteworthy:

1. There are reports that the US and China are quietly de-escalating trade tensions.

2. LIBOR-OIS spreads narrowed very slightly, and asset allocators have chosen to cheer the headline that widening over the past few weeks is not systemic but rather, is due to a change in USD funding behaviour across different instruments.

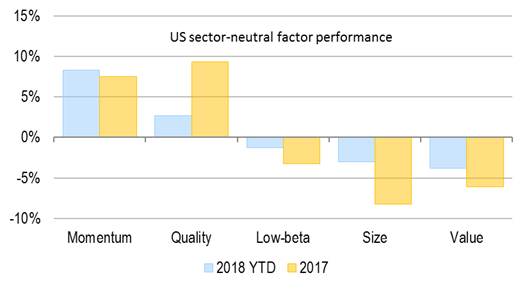

Interestingly, alpha and beta continue to tell different stories. Whereas equities outperformed bonds at an asset allocation level, within the equity market, momentum and quality long-short indices bounced strongly, while value was flat, and small caps and low-beta stocks underperformed. This continues the profile of alpha seen since Trump’s election victory in late 2016.

We think that value is still lagging, despite positive risk appetite among asset allocators, because stock pickers are concerned about still-wide LIBOR-OIS spreads. Even if recent spread widening is not systemic, it still represents an increase in funding costs, and a net drain on USD liquidity. In an environment characterized by stretched asset pricing, this keeps investors wary of the risks of over-tightening and de-leveraging. And in a de-leveraging environment, prices drive earnings, dividends and book values, rather than the other way around, creating numerous value traps.

In short, asset allocators are taking the glass half-full interpretation of LIBOR-OIS spread widening, while stock pickers are taking the glass half-empty approach.

As all of this unfolds in global markets, the AUD equivalent of the LIBOR-OIS spread continues to widen. It is not so much that tighter USD liquidity conditions are causing a problem for Australian financial institutions. After all, cross-currency basis swap spreads are still positive and narrow, and in any case, Australian banks do not technically need foreign funding. But the Australian money market continues to factor in more counterparty credit risk than is normal by historical, or international standards. Not only does this raise chances of out-of-cycle rate hikes – but it could be signalling a deeper problem in the economy.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.