In the wake of test match cheating scandal, the Australian market is also likely to do something “un-Australian” today. Therefore, it is worth having an “un-Australian” explanation for what is going down.

Our global money markets expert Zoltan Pozsar has published an article helping to explain some of the bizarre movements in spreads over the past few weeks (please see his article “Global Money Notes #12: BEAT, FRA-OIS and the Cross-Currency Basis”, dated 22 March 2018). His note is quite technical, and so we summarize his key conclusions, and basic logic here:

1. There is a large number of entities outside the US that are dependent on USD funding.

2. These entities can obtain USD funding in a number of ways. They could issue securities (eg commercial paper, or certificates of deposit) directly into the US market, during the US time zone. If eligible, they could borrow on an unsecured basis from US banks in the euro-dollar or interbank market. Or they could try to obtain local currency-denominated funding and convert this into USD-denominated funding via currency derivatives.

3. Tax reform is encouraging US multi-national corporates to repatriate capital. This drains USD supply from offshore markets, and forces foreign entities dependent on USD funding to issue securities more into US markets. The new base erosion and anti-abuse tax (BEAT) is making it less attractive for US branches of foreign entities to obtain USD funding from their foreign parents (assuming they have USDs to spare). This is forcing the branches to borrow more USDs directly in the US. It is also reducing the need for their parent entities to use currency derivatives to obtain USDs to fund them.

4. The net effect of all of this is that interbank credit spreads in USD funding markets (LIBOR-OIS, FRA-OIS, TED) rise, but cross-currency basis swap spreads on derivative instruments narrow. There is a switch in funding behaviour.

5. The rise in US interbank credit spreads is not an indicator of a systemic credit event like it was during 2008. But it is a sign of an emerging USD shortage. Pozsar has been expecting an offshore USD shortage to come about because of Fed balance sheet reduction in a re-plumbed financial system. This should have manifested first in cross-currency basis swap spreads. But instead, it is showing up in US interbank credit spreads.

Interestingly, an average of USD interbank credit and basis swap spreads is net widening. So we are not talking strictly about a zero sum game as USD funding behaviour switches to unsecured channels from derivative channels.

Also, it is worthwhile noting that Pozsar’s investment thesis over the past few years has been about a USD shortage emerging because of the unintended consequences of Fed balance sheet reduction, and the Treasury’s equivalent operation in bill issuance. Pozsar still holds to this view. Tax reform, bill issuance and even the threat of protectionism could continue exacerbating the USD shortage, irrespective of which instruments the liquidity stresses show up in. Note that Pozsar’s key investment call has been widening of front-end EUR/USD cross currency basis swap spreads. This has clearly not played out – but Pozsar is explaining why, and why the stress is showing up somewhere else.

Finally, we need to understand that even if USD liquidity tightening is not a sign of a 2008-style credit event, that the tightening in itself has consequences for the real economy and financial markets. This is especially the case when we consider how stretched pricing is on equities, credit and property. At the very least, rising LIBOR spreads will push up borrowing costs, causing the Fed to have to re-think its trajectory for rates. Perhaps this process has already begun, with Fed officials (on a median basis) choosing not to signal 4+ rate hikes for this year.

For these reasons, we can understand why the positive-sounding narrative that “widening LIBOR-OIS spreads is not systemic” – is also not offering much comfort for investors at the moment. The current dynamic brings to mind Greenspan’s famous quote: “ If you understood what I just said, then I must have mis-spoken”. LIBOR-OIS widening is not systemic, yes. But it is still something to worry about because USD shortages are emerging.

What does this have to do with Australia?

Interestingly, Pozsar does not mention USD funding costs for Australian entities in his article. He mentions European, Scandinavian and Japanese entities – but not Australian. Perhaps Australian banks are too small to worry about in the global scheme of things. But we think there are other reasons to justify the exclusion.

In our recent article “Credit market tightening could overshadow macro-prudential loosening” dated 23 March 2018 (attached), we argue that:

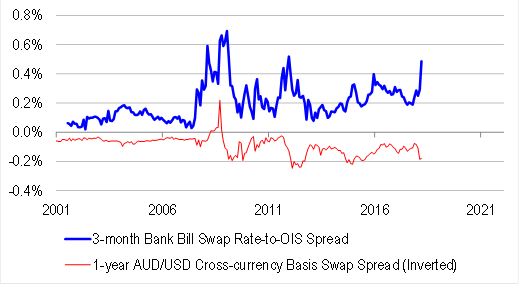

1. Rising USD funding costs should not be having much impact on AUD funding costs. Cross-currency basis swap spreads show that Australian banks have surplus USD funding at present, as evidence by positive (rather than negative) levels. The phenomenon described by Pozsar could have an impact on Australian banks to be sure, given that they do issue into the US. But the effect should be are order of magnitude smaller for Australian banks than other banks.

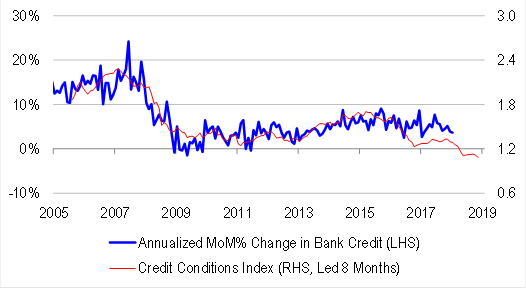

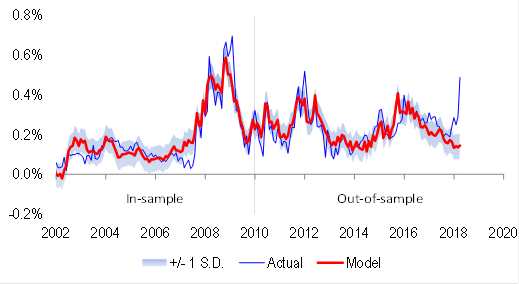

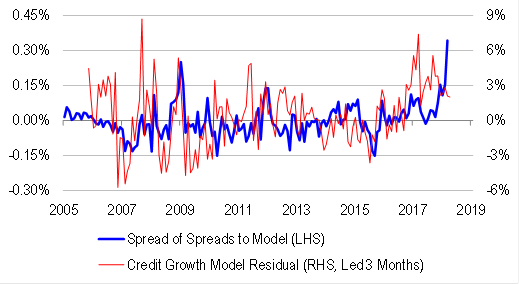

2. AUD interbank credit spreads have widened very aggressively, and this widening cannot be explained by conventional macro factors. But we have looked at something unconventional – the excess of credit growth relative to banks’ reported lending standards. We find that when credit growth is excessive, interbank spreads tend to rise, presumably because excessive credit growth brings about default risks. And over the past few years, credit growth has been well ahead of our proprietary credit conditions index. Widening USD LIBOR-OIS spreads may not be systemic – but it is an open question as to whether widening AUD spreads might be.

3. Regardless of why credit spreads are widening, they are likely to have a negative impact on Australian growth via the cost, and availability of credit.

Investment implications

Widening credit spreads are telling us at least about a liquidity event globally – and at worst, they may be telling us about a credit event in Australia. We cannot rule out the second possibility.

This sort of macro environment carries with it de-leveraging risks. And de-leveraging risk undermines the efficacy of naïve value factors. Earnings, dividends and book values stop anchoring asset prices during de-leveraging episodes. Rather, asset prices drive fundamentals. Perversely, higher multiple stocks may actually do well to the extent that they carry strong quality, or defensive characteristics.

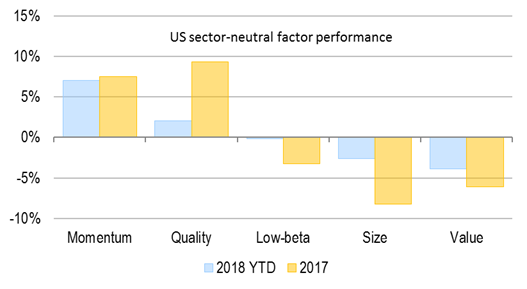

This is what we are seeing in the profile of quant factor performance. In the year-to-date, the batting order is momentum over quality over low-beta. Value and small caps are lagging badly. This profile is remarkably similar to what we saw in 2017 …

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.