Since we released our February Market Outlook there has been a significant change in US fiscal policy. Congress has supported a $300 billion (1.5% of GDP) spending package over the 18 months from April 2018. That follows the recently approved Tax Package estimated at a current cost of $1.5 trillion over 10 years.

One of the key themes from my discussions with real money managers; economists; and some officials over the last two weeks I was in the US focussed on the risks to stability of an ill- timed major fiscal stimulus. Most discussion was initially around the Tax Package although concerns around a prospective new spending package gathered momentum, particularly in the final week of the visit.

With momentum in the US economy lifting and the unemployment rate, at 4.1%, already comfortably below the estimated full employment rate of 4.5%, concerns were widely raised about stimulatory fiscal policy overheating the economy. Arguably we have not seen a comparable policy “mix” since the 1960’s.

With the introduction of the new spending package we have raised our forecasts for GDP growth in the US from 2.5% in 2018 and 2.2% in 2019 (see February Market Outlook) to 3.0% and 2.5% respectively.

With potential growth in the US generally assessed as around 1.7% these revised growth rates will pressure the output gap. The unemployment rate is likely to fall below 3.8% by year’s end meaning that the unemployment rate will have held below the full employment rate for nearly 2 years.

Despite likely ongoing volatility in equity markets and a rising bond rate (we have increased our forecast for the US 10 year bond rate by year’s end to 3.35% from 3.25%) the associated tightening in financial conditions is unlikely to slow momentum sufficiently to allow the FED to go on hold by year’s end.

In our February Markets Outlook we envisaged three FED fund hikes in 2018 with rates going on hold in 2019.

We now expect two further (March and June) FED hikes in 2019. The Federal Funds rate will then have reached 2.625%. FED estimates point to 2.5% (0.5% real) as the neutral rate.

With financial conditions tightening (we expect the 10 year Treasury rate to peak around 3.5% by March 2019); and the cessation of the temporary spending package; we assess that a modest move into “contractionary territory” will be sufficient to allow the FED to go on hold from mid-year.

Growth in the US economy is likely to slow in the second half of 2019 with bond rates easing somewhat. However we do not envisage an inverse yield curve by end 2019 and therefore no signal of an imminent US recession (inverse yield curves usually precede recessions in the US).

A second key theme in my discussions was around the risk of a steepening of the Phillips curve (relationship between wages/inflation and unemployment) once the economy spends a considerable time at/or below full employment.

Part of the explanation for the very flat curve has been the “headwinds” the economy has been experiencing in the aftermath of the GFC when wages did not adjust fully to the collapse in demand (a very popular observation from Chair Yellen). Arguably, as time has passed, and the fiscal stimulus gathers pace the “headwinds” will be replaced by “ tailwinds”.

The perceived risk for the US is that we are moving towards the point at which wages and prices accelerate.

Our forecasts for FED policy are not predicated on such an acceleration but assume a gradual lift in inflation and wages and a FED that is keen to emphasise that the 2% inflation target is symmetrical – it is quite acceptable for inflation to hold above 2% for a time (hence the prospect of a temporary “pause” some-time in 2018).

Of course an acceleration coupled with a FED determined to keep a 2% ceiling on inflation would imply a much more aggressive policy profile than we have adopted as our core view. Such a policy mix would be likely to see that inverse curve and a an associated recession.

What does this expected FED Policy mean for Australia?

Readers will be aware that Westpac does not expect the Reserve Bank to raise rates in 2018 or 2019.

This is the profile we have adopted throughout 2017 and is confirmed in our February Market Outlook.

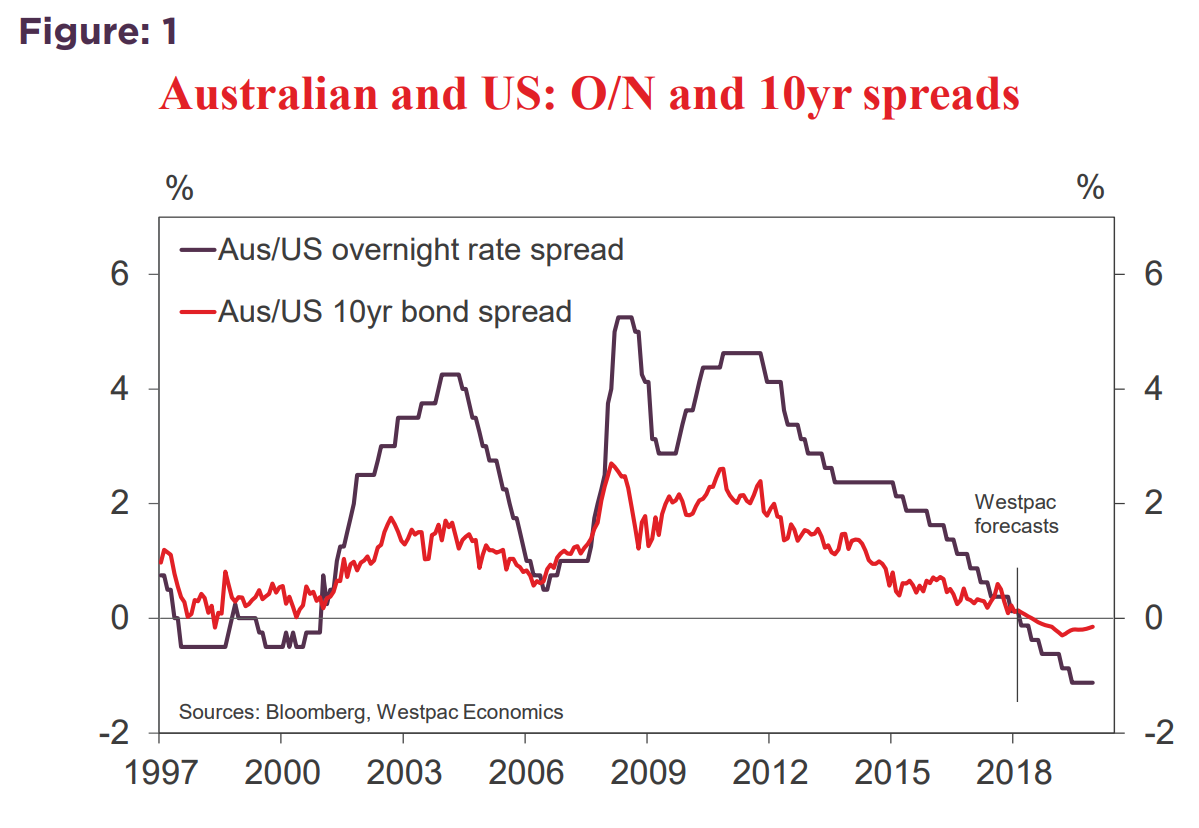

As such, our February view entailed the cash rate differential bottoming out at negative 62 basis points by year’s end. With two more FED hikes expected in 2019 we now anticipate that the differential will reach negative 112 basis points by June 2019. That is unchartered territory with the previous “record” being negative 50 basis points in the late 1990’s (see Figure: 1).

The maximum expected 10 year bond rate differential would move from negative 15 basis points to negative 30 basis points by March 2019 (Figure: 1).

We have previously discussed the reasons behind our views on Australian interest rates at length.

Governor Lowe neatly explained his own position in a recent speech “Countries like Australia, with a floating exchange rate, still retain considerable flexibility to set interest rates based on domestic considerations… we didn’t have a meltdown in the financial system… just as we did not move lock step on the way down we don’t need to do so in the other direction.”

The Governor appropriately emphasises “progress in reducing unemployment and having inflation return to the mid-point of the target range”.

In that regard I note particularly cautious forecasts from the Bank’s recent Statement on Monetary Policy – underlying inflation “stuck” at 1.75% in 2018 and rising to only 2% in 2019; the unemployment rate holding above full employment (5%) at 5.25% through 2018 and 2019.

These forecasts therefore anticipate underlying inflation holding at or below the bottom of the 2–3% target band for five consecutive years (already below the 2% in 2015; 2016; and 2017). Arguably this represents a structural fall in inflation which has not been addressed more aggressively with even lower rates due to concerns around housing markets.

On the other hand the Bank is decidedly “upbeat” on growth – 3.25% in both 2018 and 2019. That contrasts with “potential” growth of 2.75% – two years of a narrowing output gap but only limited impact on inflation and unemployment.

We recognise that our forecast lift in US growth has upside risks to our 2.5% forecast for Australian GDP growth in 2018 and 2019. However we would be surprised if the lift in US growth boosted Australia’s growth above potential (Westpac’s current growth forecast for 2018 and 2019 is 2.5% compared to potential of 2.75%).

For Australia the expected slowdown in China’s growth rate from 6.9% in 2017 to 6.3% in 2018 is much more important.

What does this mean for AUD?

We have chosen not to markedly change the AUD forecasts from the February Markets Outlook. We still see AUD around USD 0.70 by March 2019.

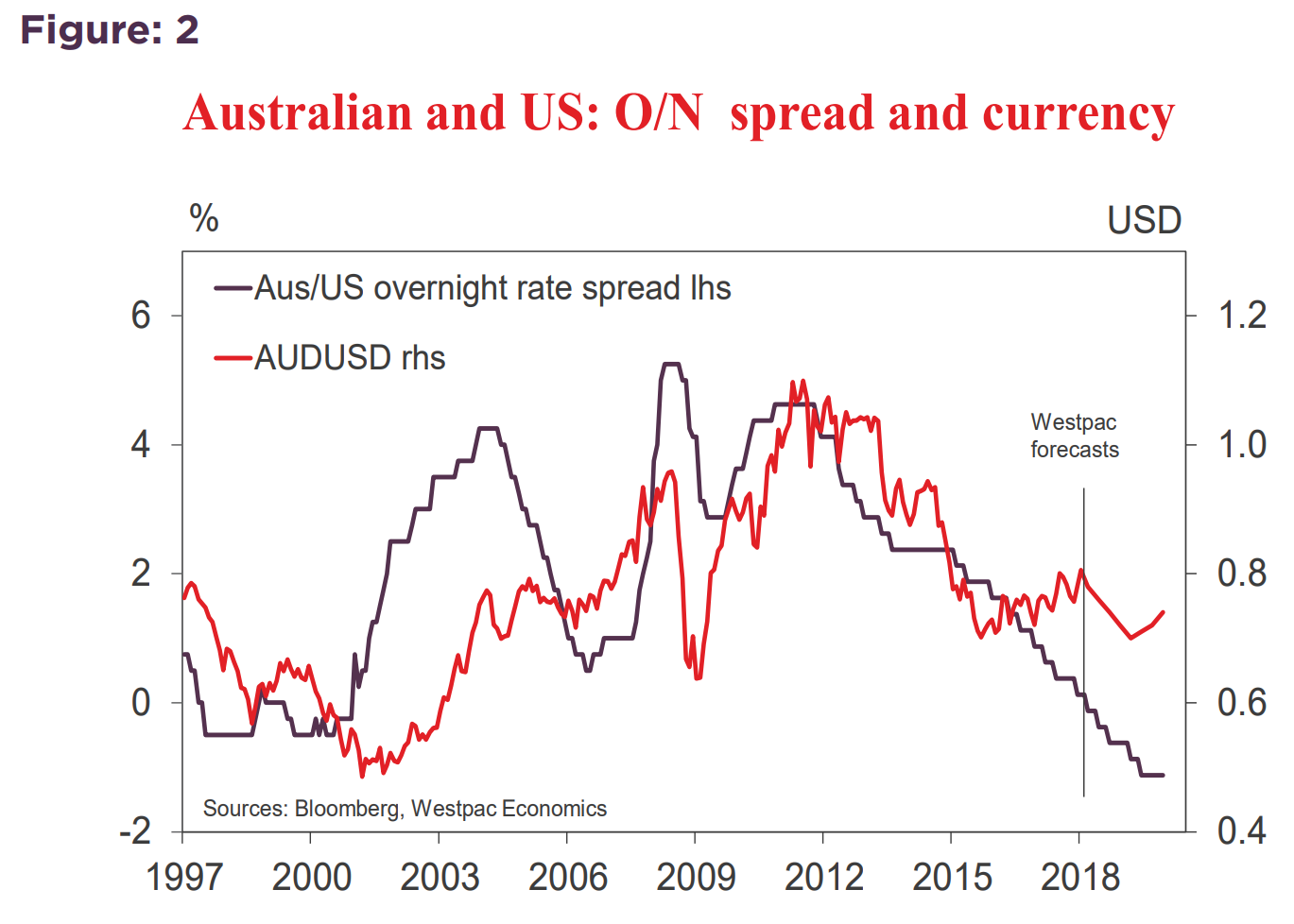

Figure 2 highlights the relevance of interest rate differentials to previous trends in the Australian dollar.

These forecasts are based on a 7% lift in DXY (the USD Index) out to mid- 2019. My discussions in the US showed widespread negativity around the USD. Arguments against the USD hinge around widening budget and current account deficits; political uncertainty, including potential political interference with the FED; and ECB and BOJ tightening.

Notwithstanding this sentiment, we continue to favour our positive USD view.

In 2017 Europe and Japan ‘s growth rates exceeded potential by sharply more than did the US. (more than 1% compared to around 0.5%).The USD fell an extraordinary 11% through 2017.

The story will be different in 2018. US growth is expected to exceed potential by 1.3% as Europe and Japan slow.

We are also less convinced than many commentators and certainly a range of the people I met in the US around any imminent tightening by either the ECB or BOJ.

That is in sharp contrast with our FED view.

However, despite the more aggressive FED in our revised forecasts the offsetting concern about rising fiscal and current account deficits has caused us to hold with the currency targets in the February Market Outlook.

That is almost exactly the MB view. It will be an all-time low on the 10 year spread. I will add that we expect China slow enough for bulk commodities to fall materially into H2 and that the Fed will likely end the business cycle (accidentally or otherwise) before Australia can hike rates at all.

Hence, once the next round of AUD weakness starts it has plenty ahead of it.

Advertisement

David Llewellyn-Smith is chief strategist at the MB Fund which is currently overweight international equities that will benefit from a weaker AUD so he definitely talking his book (or Westpac is!) Fund performance is below:

If these themes interest you then contact us below.

Advertisement

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.