More political suicide today from Do-nothing Malcolm:

Malcolm Turnbull has used a meeting with United States Treasury Secretary Steve Mnuchin to bolster his argument for his proposed company tax cuts by claiming up to 70 per cent of the benefit will flow to workers.

Speaking to reporters following his meeting with Mr Mnuchin, Mr Turnbull said the Treasury secretary advised him that the Trump tax cuts – which slashed the US corporate rate from 35 per cent to 21 per cent – would add almost 1 per cent tio the US’s Gross Domestic Product and see 70 per cent of the benefit flow through to workers.

“This is precisely the same argument that we’ve been presenting in Australia in respect of our own company tax program,” Mr Turnbull said.

I doubt very much that this will this play well with Australians. They don’t believe the rhetoric around tax cuts, they don’t like Donald Trump and his endorsement won’t help:

And since when was playing domestic politics with foreign policy acceptable?

Here’s what the world’s leading economic commentator, Martin Wolf, said about Trump tax cuts:

How does a political party dedicated to the material interests of the top 0.1 per cent of the income distribution win and hold power in a universal suffrage democracy? That is the challenge confronting the Republican party. The answer it has found is “pluto-populism”. This is a politically successful, but dangerous, strategy. It has brought Donald Trump to the presidency. His failure might bring someone more dangerous, more determined, to power. This matters to the US and, given its power, to the wider world. The tax bills going through Congress demonstrate the party’s primary objectives.

An argument for hoping that better times will soon be here is the huge tax cut for business. It is quite unlikely, however, that this will unleash a flood of investment and higher underlying economic growth. A more plausible view is that it will mainly increase stock prices, wealth inequality and the speed of the competitive race to the bottom on taxation of capital. British experience on this is sobering. The slashing of UK corporate tax rates to 19 per cent has done little for investment or median real wages. The hope that it proves any different in the US is likely to be disappointed.

And:

Furthermore, the US has just initiated a grossly pro-cyclical and fiscally irresponsible increase in its structural fiscal deficit, one designed, overwhelmingly, to shower benefits on the wealthy. The hypocrisy of this, in view of past Republican assaults on attempts by the Obama administration to administer a desperately needed fiscal boost to the crisis-hit US economy in 2009, is breathtaking. It would not be surprising if this fiscal policy, along with a worldwide recovery in private investment, raised real interest rates across the world economy.

This last point was echoed by RBA chief Phil Lowe this week:

“That’s very problematic and if we were to go down the direction of having lower corporate tax rates it is really important that it does not come at the expense of higher budget deficits.”

Which is exactly what we would be doing given the entire charade of future surpluses is based upon short term gains in iron ore and coking coal prices. We’re supposed to saving now so we can stimulate later if need be.

In closing let’s muse on whether Mr Turnbull has heard of the phrase “Ricardian Equivalence”:

The proposition (also known as the Ricardo–de Viti–Barroequivalence theorem) is an economic hypothesis holding that consumers are forward looking and so internalize the government’s budget constraint when making their consumption decisions.

It’s not a terribly useful theory usually but in recent years has fit patterns of behavior in Australia. That’s likely because household balance sheets are so stretched that they kind of freak out at any deterioration in the national Budget and diminution in its implicit guarantee.

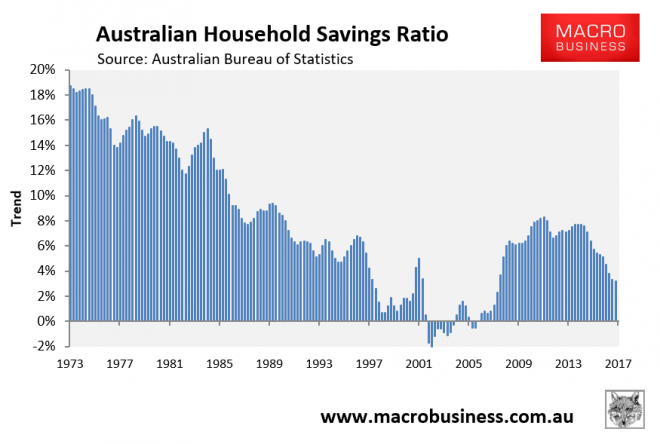

One example was the Abbott Budget of 2015. Another was the pre-GFC period when the Howard Government showered tax cuts upon all and sundry only to watch household savings rate climb:

A Trump endorsement is exactly what Turnbull’s company tax deserves.