The Grattan Institute has released a new paper for the Australian Gender Economics Workshop 2018, which argues that Australia’s superannuation system is Australia’s retirement income system is not working for the poorest Australians, who are disproportionately women. Grattan also argues that expanding already-generous caps on superannuation contributions would likely worsen gender inequality in retirement savings.

Below is the summary of the report, along with some key charts from the report’s body:

Australia’s retirement income system is not working for the poorest Australians, who are disproportionately women. Australia has a persistent gender gap in retirement savings and incomes. This means that women, particularly single women, are at greater risk of poverty, housing stress and homelessness in retirement.

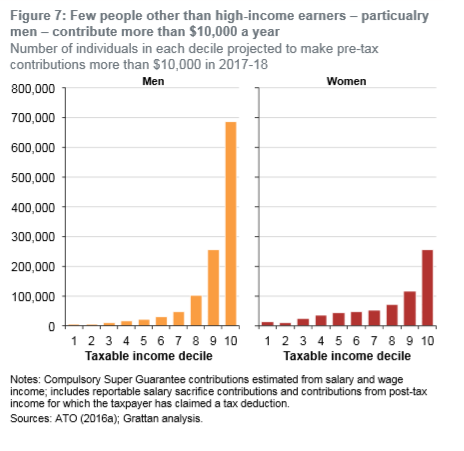

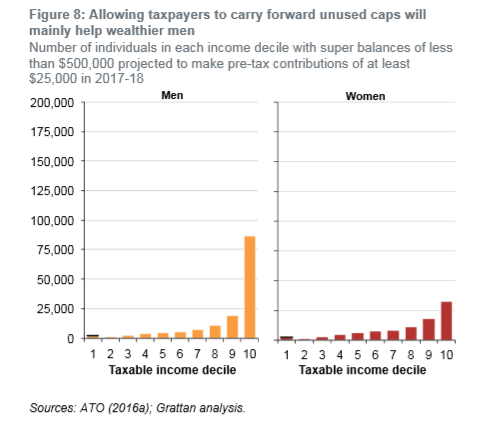

The superannuation lobby want more generous superannuation tax breaks to boost the retirement incomes of women. But in a paper to be presented to the Australian Gender Economics Workshop on Friday 9 February 2018, Grattan Institute Fellow Brendan Coates shows that expanding already-generous caps on super contributions would likely worsen gender inequality in retirement savings. Women save less via superannuation because they earn less. The current generous annual caps on pre-tax contributions are predominately used by older, high-income men to reduce their tax bills.

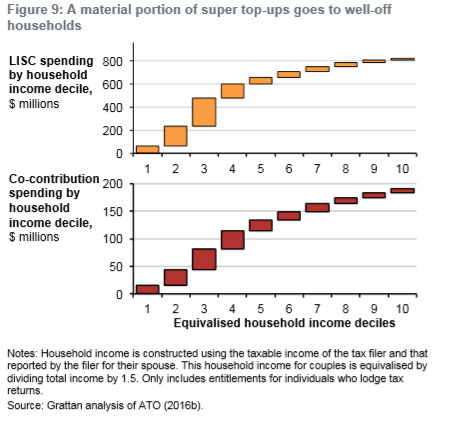

Other proposals to provide more top-ups to the superannuation savings of low-income earners, or particularly to women, are at least somewhat targeted at the gender gap. The now-renamed Low Income Superannuation Tax Offset (LISTO) will ensure that low-income earners are not disadvantaged when contributing to superannuation. But super top-ups should not be expanded. It is too hard to target them tightly at those most in need, and super fees can eat up their value. For example, Industry Super Australia’s proposed $5,000 Super Seed annual contribution to the superannuation accounts of younger low-income earners could cost almost $4 billion a year – and about a quarter of the Super Seed payments would still go to Australia’s wealthiest 50 per cent of households.

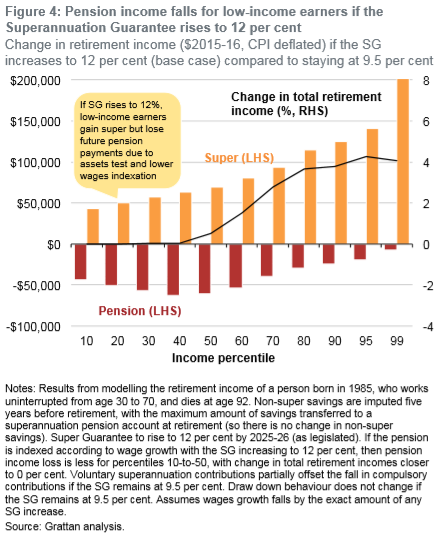

Nor is there a strong case to raise the Superannuation Guarantee to 12 per cent, as currently legislated. Higher compulsory super contributions are ultimately funded by lower wages, which means lower living standards for workers today. Therefore, increasing the Super Guarantee to 12 per cent will hurt the living standards of low-income earners, the bulk of whom are women.

And raising the Super Guarantee to 12 per cent could also hurt the retirement incomes of existing pensioners, by suppressing wages indexation of the Age Pension.

The Grattan Institute research paper proposes two reforms which together could help close the gender gap in retirement incomes and provide a boost to the retirement incomes of Australia’s most vulnerable women.

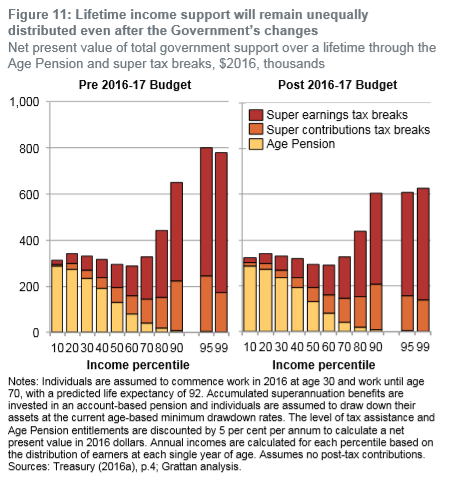

First, better targeting super tax breaks to the purposes of superannuation would reduce the gender gap in superannuation savings. Super tax breaks provide the greatest boost to high-income earners, who don’t need them. Most of these high-income earners are men. Better targeting of super tax breaks could free-up revenue to provide more targeted support for retirement incomes for people who need it most, and to reduce marginal effective tax rates for low- and middle-income earners to encourage greater female workforce participation.

Three reforms to super tax breaks are needed:

Contributions from pre-tax income should be limited to $11,000 a year. Eighty per cent of contributions above this level come from people likely to retire with enough assets to be ineligible for an Age Pension even without such big super tax breaks.

Contributions from post-tax income should be limited to $50,000 a year.

Earnings in retirement – currently untaxed for super balances up to $1.6 million – should be taxed at 15 per cent, the same as superannuation earnings before retirement.

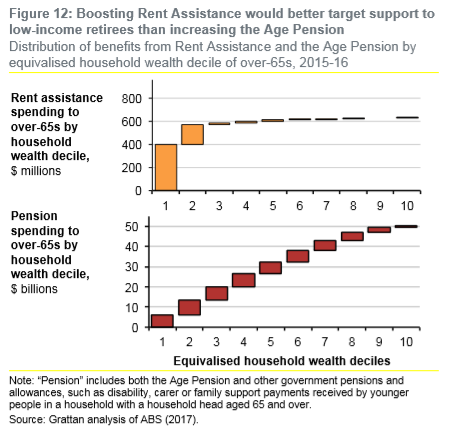

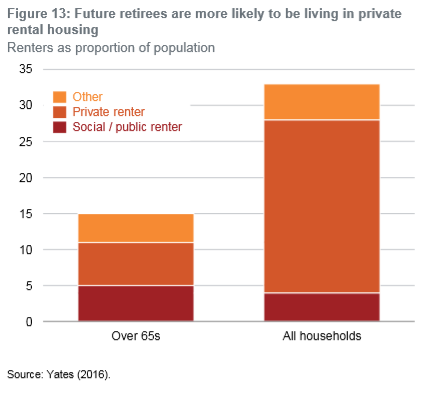

Second, a targeted boost to the Age Pension for retirees who do not own their own home, delivered as higher Commonwealth Rent Assistance, would do the most to alleviate poverty in retirement. Single women who are retired and do not own their own home are the group most likely to rely almost solely on the Age Pension, and are at the greatest risk of poverty in retirement. This proposal is affordable: a targeted $500-a-year boost to Rent Assistance for Age Pensioners would cost $250 million a year.

MB wholeheartedly agrees with the Grattan Institute’s assessment, and has made similar arguments previously. Expanding superannuation concessions would merely heighten inequities already present in the retirement system and would be a dud deal for low income earners and taxpayers alike.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.