MB has frequently questioned the merits of government policy that forces Australians into private health insurance, and argued that diverting subsidies away from private health insurance into the public system would lead to more efficient health outcomes.

Over the past week, several well-known commentators have gone one step further, describing the private health system as an outright “con job”.

Last week, The Guardian’sGreg Jericho penned the following:

Far from being free, the industry is absolutely dependent upon governments doing all they can to encourage people to join it and penalise those who don’t.

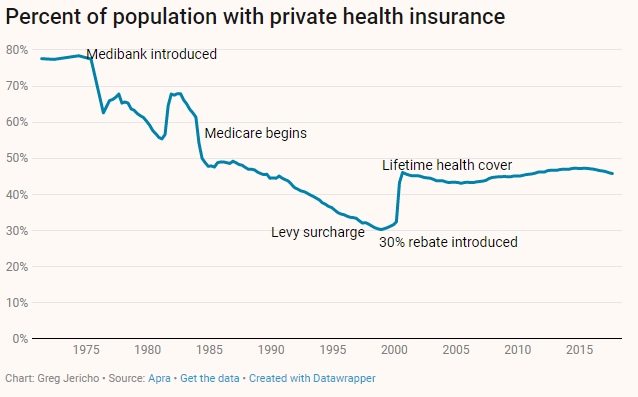

Since the first step into universal healthcare with Medibank in 1975, the percentage of the population in private health insurance has steadily fallen…

Take away that government-mandated penalty, and people would leave private health in their droves. The free market at play without that government blackmail would likely see many of the 60% of those with health insurance who say it does not deliver value for money leave the system.

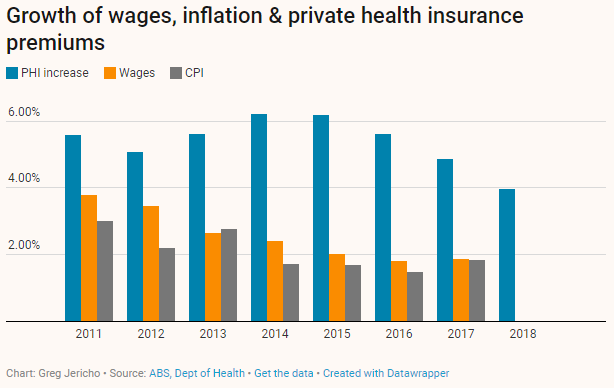

And you can understand why nearly two-thirds of private health insurance holders think that, given with the latest increase in premiums of 3.95%, the cost of health coverage has far outstripped both overall inflation and wages growth:

And yet the industry remains extremely profitable for the 13 of the 37 private health insurance companies that are for-profit.

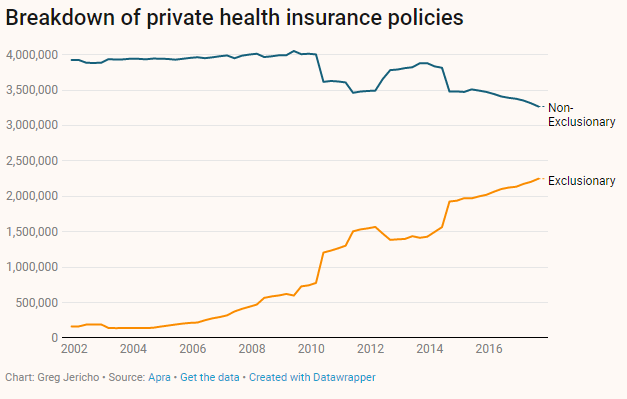

But it is not just the cost of the premiums – it is what you get for your money that is a concern. Increasingly policies contain exclusions – exclusions which add to the complexity of the system and leave people unaware of what they are precisely covered for:

Similarly there has been a large increase in the number of policies that contain excess or co-payments… now, over 80% of policies have excesses and co-payments…

We have a system that attempts to force young people to take out a private insurance policy they don’t want or particularly need in order to fund the use of it by older people.

…governments of both persuasion have attempted to prop up the private sector. And as ever the private system has taken advantage – offering less coverage while complaining about needing ever more government assistance.

Advertisement

And today, Fairfax’sRoss Gittins has stepped up to the plate:

Opinion polling by Essential has found that, although a clear majority of people believe “health insurance isn’t worth the money you pay for it”, 83 per cent of people believe that “the government should do more to keep private health insurance affordable”.

The former opinion is right; the latter is delusional. Governments have been trying to keep health insurance affordable on and off for decades, while its cost just keeps climbing.

Why? Because it’s a self-defeating process. The more you do to make insurance affordable, the easier you make it for the people running the health funds, the owners of private hospitals and the surgeons and other procedural specialists who work in hospitals, to raise their prices and fatten their profits. Which the pollies fully understand.

In the old days health funds were owned by their members, except for the government-owned Medibank Private. These days, three of the biggest funds – Medibank Private, Bupa and NIB – are for-profit providers, thus increasing the pressure on the government to allow big price rises and reducing the chance of getting value for money.

As Ian McAuley, of Canberra University, has written, from a policy perspective health insurance is a high-cost and inequitable way to fund healthcare.

Only 85 cents of every dollar passing through private insurance makes its way to paying for healthcare. And only if you can afford it do you share in the government subsidies taxpayers provide.

From the customers’ perspective, it’s a con job. Most people under 60 get back only a fraction of what they pay. Often when you do claim you don’t get what you expected, because you don’t get choice of doctor or a private room, you’re caught by ever-changing exclusions from your policy, or because no one warned you about a huge gap payment.

Many buy insurance to avoid waiting times for elective surgery. But if private insurance didn’t exist, surgeons would have to earn more of their income from public hospitals and waiting times would be shorter. It creates the problem it purports to solve…

Private insurance is so counter-productive and so unfair that the best thing would be to end the subsidies and use the saving to improve the performance of the public system…

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.