John McGrath, the founder of the embattled real estate group, McGrath, is set to appoint a new chairman on Monday – likely be a ”well known former chief financial officer” – on a whittled-down board with two other directors.

…Privatising the company ”is off the agenda,” spokesman Tim Allerton said. Mr Allerton has been called in as a temporary consultant by Mr McGrath.

…There will be only three directors in the new-look ”lean and mean” board with backgrounds in the financial and legal industries.

Mr McGrath, who has never been comfortable in the public role, will ”focus on restoring investor and the market’s confidence and play to his strengths”, Mr Allerton said.

This will see him focus on restoring shareholder value by recruiting new agents and building confidence across the business, particularly with franchsise agents and the property management operations.

Mr McGrath is also getting advice from a range of ”long standing friends”, including Bruce McWilliam, a director of the Seven Network, and former rugby player Paul Cheika, whose brother Mike coaches the Wallabies.

…He said the issue of Mr McGrath’s gambling habits ”is very seperate to the business and would remain that way”.

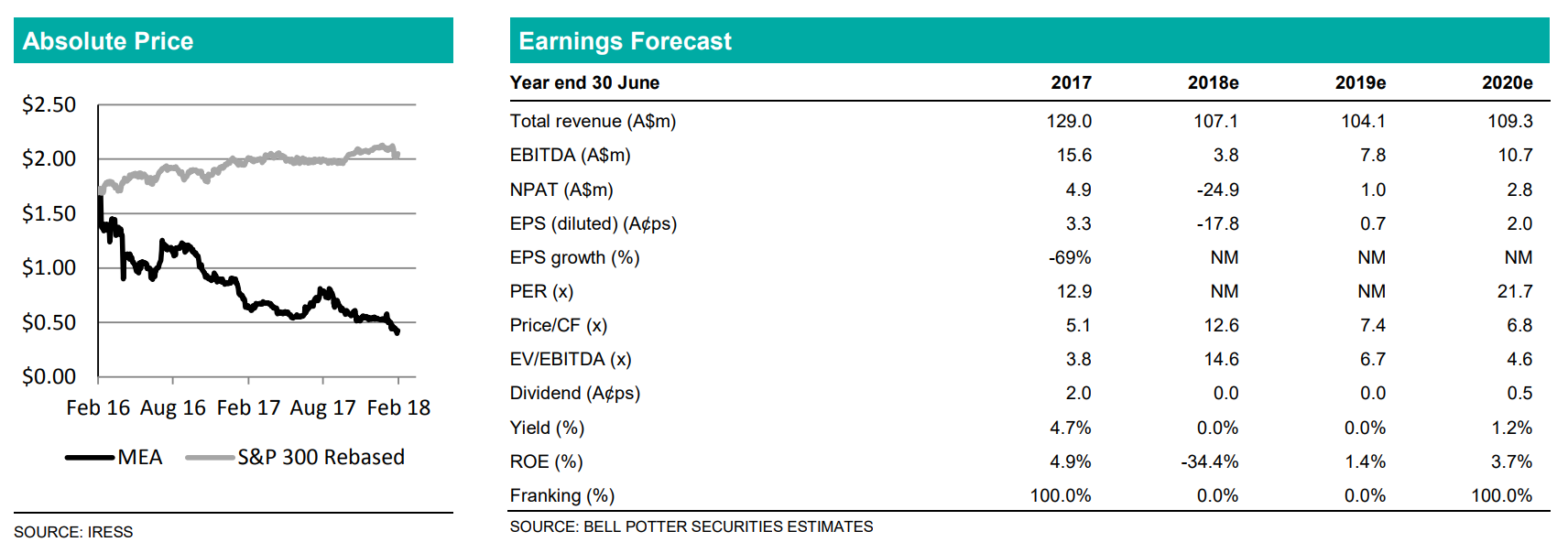

Only one more problem to solve: the steadily dying property market. Former ally, Bell Potter, sinks the boot in today:

1HFY18 result as flagged but additional impairment

1HFY18 EBITDA loss of $0.1m was as flagged by McGrath last month and consistent with our forecast. The company, however, took a goodwill impairment charge of c.$23m which resulted in an NPAT loss of $25.5m versus our forecast NPAT loss of $2.8m (i.e. we did not forecast the impairment). Only other key difference between the result and our forecasts was revenue was lower ($51.5m vs BP $56.6m) which was driven by lower than expected revenue in Company Owned Sales ($32.3m vs BP $36.4m). There was no interim dividend and we did not expect any.

FY18 guidance not reiterated

McGrath did not, as far as we can tell, reiterate the FY18 guidance which was provided in the company update provided in late January. No specific guidance was provided and the company only gave a few general outlook statements including “focus is on improving productivity and performance of the Company Owned Sales segment” and “continued stable contributions of our annuity style businesses.”

Further downgrades

We have further downgraded our forecasts given the lack of reiteration of the FY18 guidance and also the general lack of confidence we have of a quick and successful turnaround. We also believe there has been some brand damage over the past year or so which will make a turnaround even more difficult.

Investment view: Maintain SELL, PT down 11% to $0.40

We maintain our SELL recommendation on McGrath. We have updated our DCF for the earnings changes as well as the time creep. We have also reduced our valuation of the annuity businesses to the lower end of the $0.40-0.44 range given the 1HFY18 earnings decline in the property management business and also for conservatism. The net result is an 11% reduction in our PT to $0.40. We note the PT is now equal to the low end of our valuation of the annuity businesses.

Advertisement

Let’s not forget that it was BP that underwrote the float at $2.10.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.