The selloff from overnight continued here in Asia today as markets weighed up the return of King Dollar and the more hawkish head of the Fed. The USD only hit a roadblock against Yen as the BOJ did some longer dated bond buying to boost the currency while in China the manufacturing PMI fell the most in nearly five years.

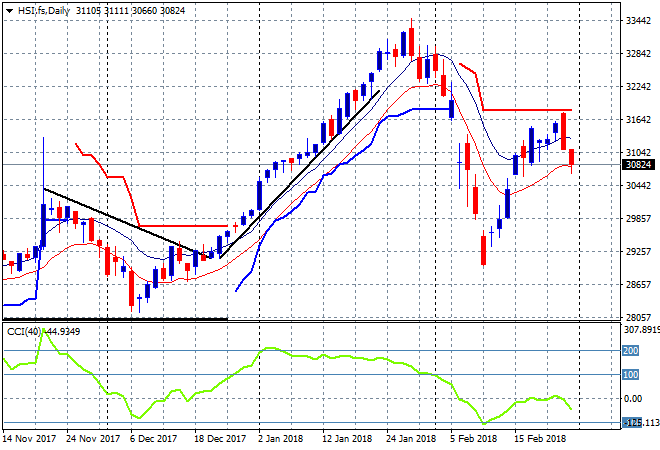

The Shanghai Composite was down 0.7% to remain below 3300 points, currently at 3267 points, recovering a little after the long lunch break. The Hang Seng Index is feeling the heat a bit though, down 1.2% to 30871 points, after rejecting resistance yesterday at the 31700 level, and breeching the low moving average on the daily chart for the first time in two weeks. Support at 30000 could come under pressure here:

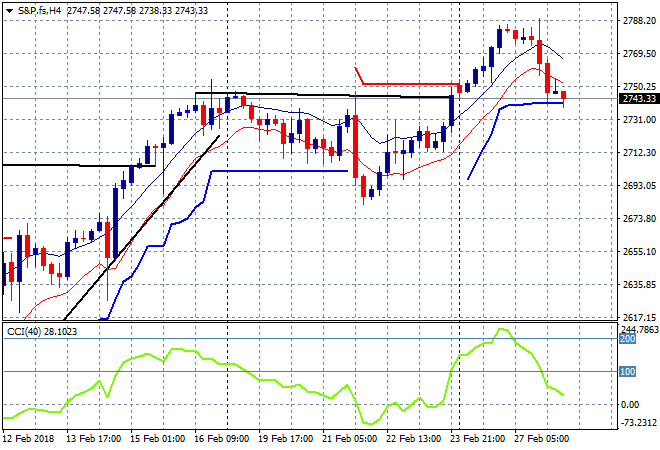

S&P futures continued to pull back after last night’s selloff, bunching up around former resistance, now crucial support at the 2740 point level:

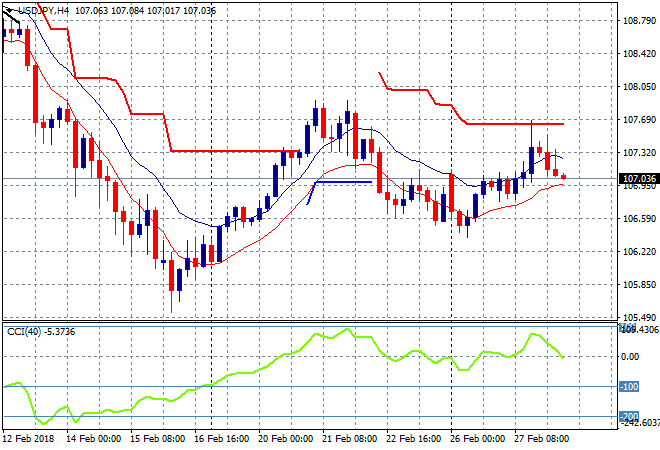

Japanese stocks fell the hardest in the risk off move with the Nikkei 225 down 1.4% to 22068 points, obliterating the last two days of strong gains. The USDJPY pair is slowly grinding lower after trying to make a run for it overnight, currently anchored just above the 107 handle moving into tonights busy economic calendar – watch Euro especially:

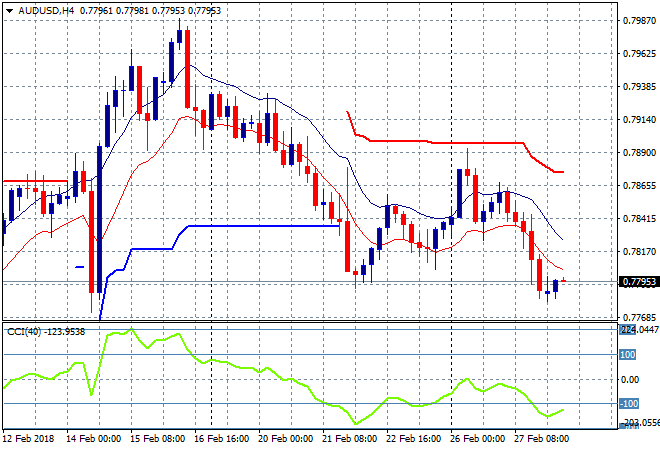

The ASX200 was the least worst off in Asia, closing 0.6% lower to 6016 points, still holding on to just above the psychologically important 6000 point level. The Aussie dollar has bounced back ever so slightly after last night’s knee capping, currently just below the 78 handle as it matches the previous two week low in what could be building support:

The economic calendar ramps up again tonight with the only unemployment print in Europe that matters – Germany – followed by the EZ wide CPI print for February. It gets busier in the US with fourth quarter GDP and then the DOE oil inventory report.