Risk markets are quite mixed here in Asia, particularly in China where stocks sold off in large caps due to concerns over earnings. Bond yields continue to moderate however, while currency markets are relatively quiet with some minor buying support for USD sending the majors down slightly.

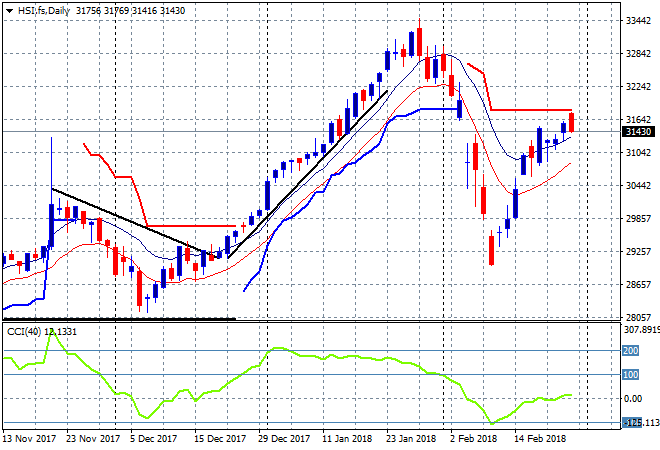

The Shanghai Composite lost over 1% to be back below 3300 points, taking back most of yesterday’s gains. The Hang Seng Index is off about half that, down 0.55% to 31326 points, after gapping higher on the open but failing to close the higher expectations. This almost took it up to resistance at the 31700 level, which is proving elusive to breach:

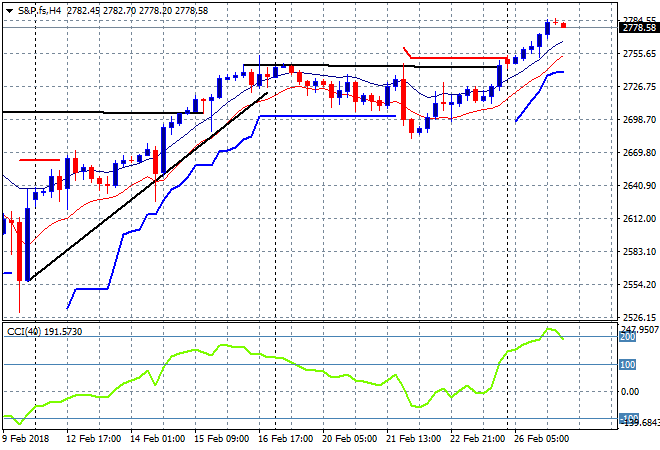

S&P futures are pulling back as markets position for the new Fed Chair to testify before Congress (remember what’s the opposite of Progress?) as we move into a fourth week of new highs:

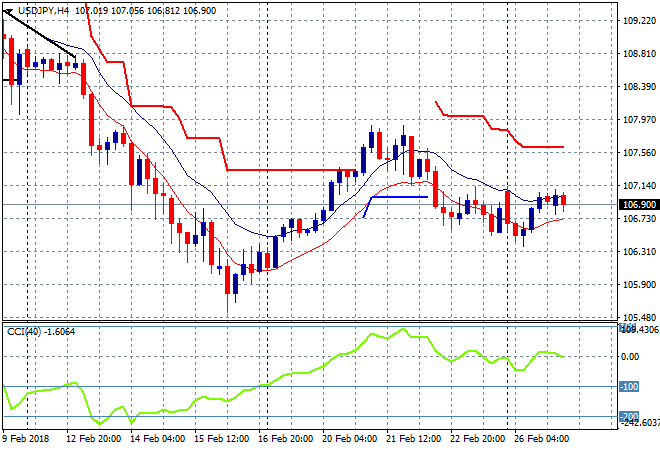

Japanese stocks however continue to rally with the Nikkei 225 up another 1% to 22389 points, building on its previous breakout. The USDJPY pair is slowly pushing higher against but not above the 107 handle, as the USD gains some strength before the Powell testimony:

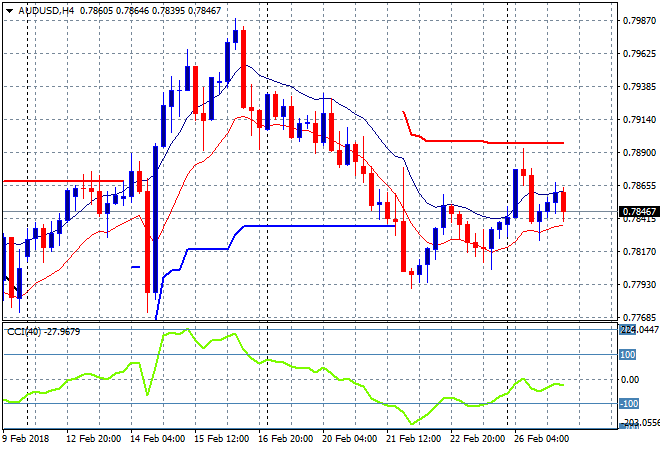

The ASX200 had a fair session, considering how its twisted and moved around by both Chinese and American stock markets in terms of correlation. Closing 0.2% higher at 6054 points its holding on to its gains above the psychologically important 6000 point level, setting up for a follow through to 6100 soon. The Aussie dollar was looking good against USD early in the session but has reversed in the last hour or so, now at 78.50 as risk positions for tonights busy economic calendar:

The economic calendar ramps up tonight with the German February CPI print, followed by US durable goods and advanced trade balance, but the big one is new Fed Chair Powell’s testimony to Congress.