Via the AFR comes Macro Currency Group’s Mark Farrington:

“The US economic story is still too strong, the Fed is too far ahead of the central banks,” Mr Farrington said in an interview with The Australian Financial Review.

“Eventually this very long expansion and bull market has to end with some kind of recession. Until that day comes all of the potential for a growth, and inflation, surprise and higher rates will come from the US.”

The US dollar’s surprise weakness in 2017 was down to a combination of negative news flow that came with Donald Trump’s first year as President and a strategy among investors to “buy the laggards” and look to underperforming currencies, Mr Farrington says.

…But Mr Farrington believes interest rate differentials will re-exert itself as a factor in currency markets, and as the Federal Reserve raises rates to about 3 per cent, the US dollar will strengthen.

The increase in US interest rates relative to the rest of the world has created an “unusual phenomenon in which the global reserve currency has become the de facto high yielder at the same time”, Mr Farrington said.

“Interest rates are meant to compensate you for liquidity risk and [in this case] they are not doing that. But in this case [higher rates] are in place to stabilise an economy that has moved below NAIRU [the natural rate of unemployment].”

…”The whole idea for countries that were concerned about currency strength was that if they lagged the Fed their currency would weaken and give them a boost, so that game plan has to be thrown out,” he said.

…”Interest rates may have to stay lower for longer in Australia than you would otherwise think in an economy with high exposure to housing and high household leverage.”

…”We are not going back to having manufacturing, and not going to go back to this big super cycle in the Australian dollar playing a role as a counter-cyclical shock absorber to the economy. Interest rates will have to do more of the work because the currency is going to do less.”

Not entirely true:

- some of the recent USD weakness has been on upside growth surprises in Europe;

- though I agree that it is so far behind the US in the cycle that cash rate spreads will keep widening, especially so since the incipient Chinese slowdown should hit EUR harder;

- longer term, once the great Australian deleveraging begins then it’ll be curtains for the AUD as well as interest rates. That we don’t have the tradables we used to only means it will be harder to rebuild them not that we won’t need to…

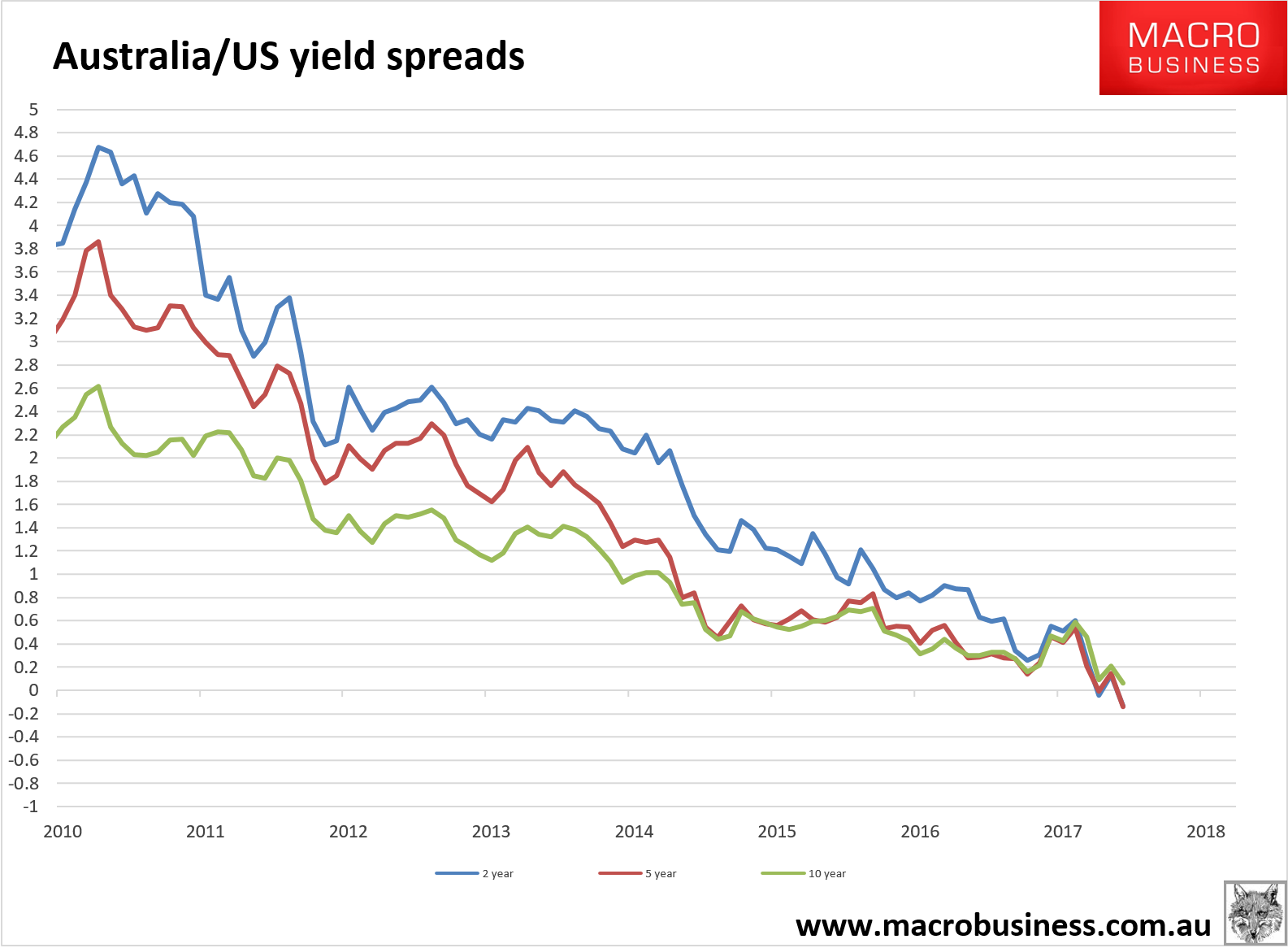

But, basically I agree. The spread between US and everybody else’s rates is going to widen a lot more. Indeed, the Australian/US spread hit new wides all day yesterday:

The 10 year spread came within 3bps of inversion last night:

That’s actually 20bps below where it was in 2001 when the AUD was at 47 cents, although the short end spread was much deeper then.

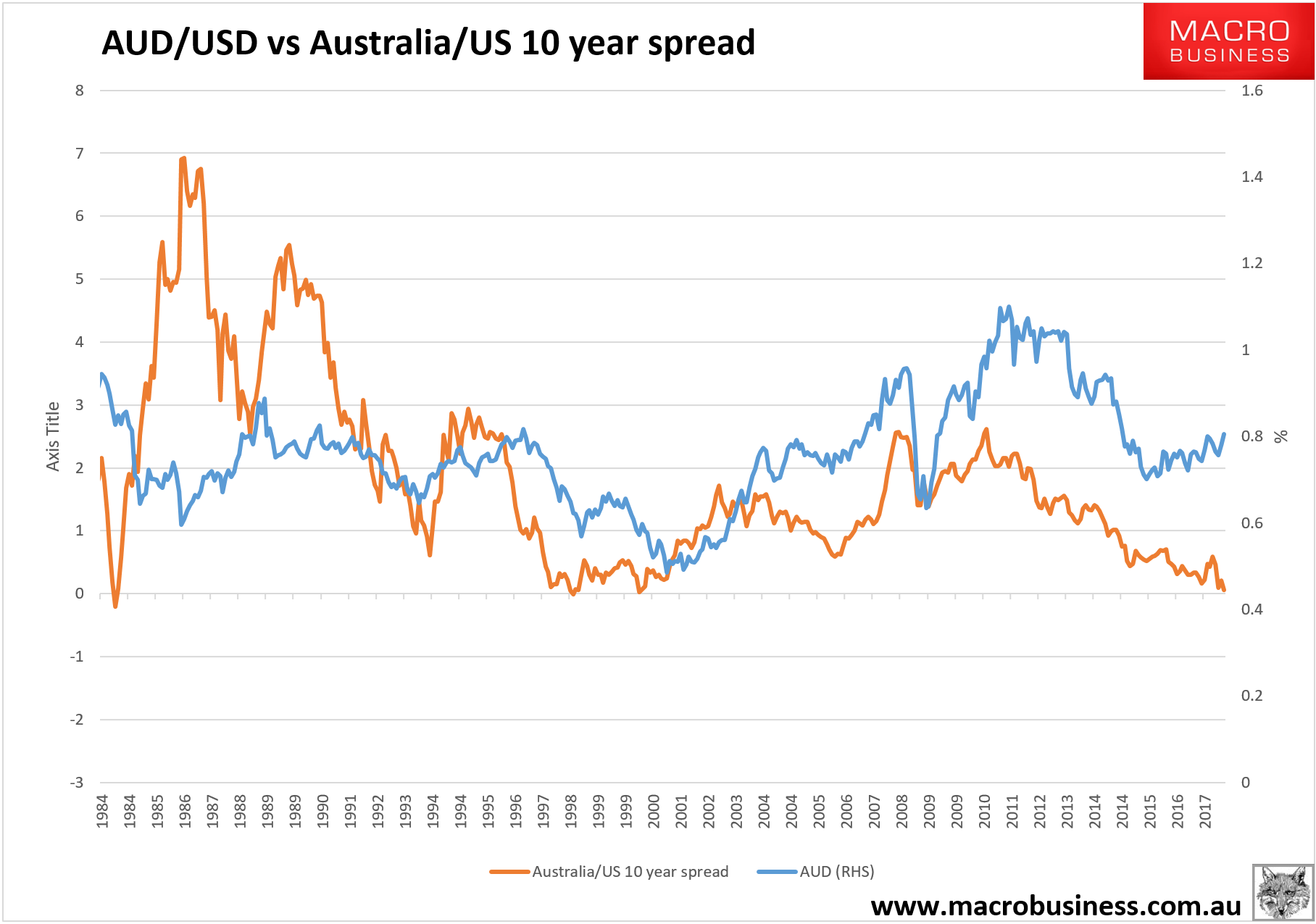

Notice in the chart how the spread and currency have trended together non-stop since the AUD float. That is, until late 2015 when China stimulated again. That’s the key. The wedge between today’s high dollar and the low yield spread is the high terms of trade (largely iron ore and coking coal). But as that falls with a slowing China this year…well…the stretching of the AUD rubber band may snap as the 10 year spread sinks into unprecedented negatives.

The “synchronised global growth” narrative might be exciting in New York right now but, to put it bluntly, why would you buy AUD on a deepening negative carry when Aussie houses prices are falling and bulk commodities are about to join them (assuming no new Chinese stimulus)?

As the wise gentleman says, what else is there?

—————————————————

David Llewellyn-Smith is chief strategist at the MB Fund which is currently long international equities that will benefit when the Australian dollar falls so he is definitely talking his book.

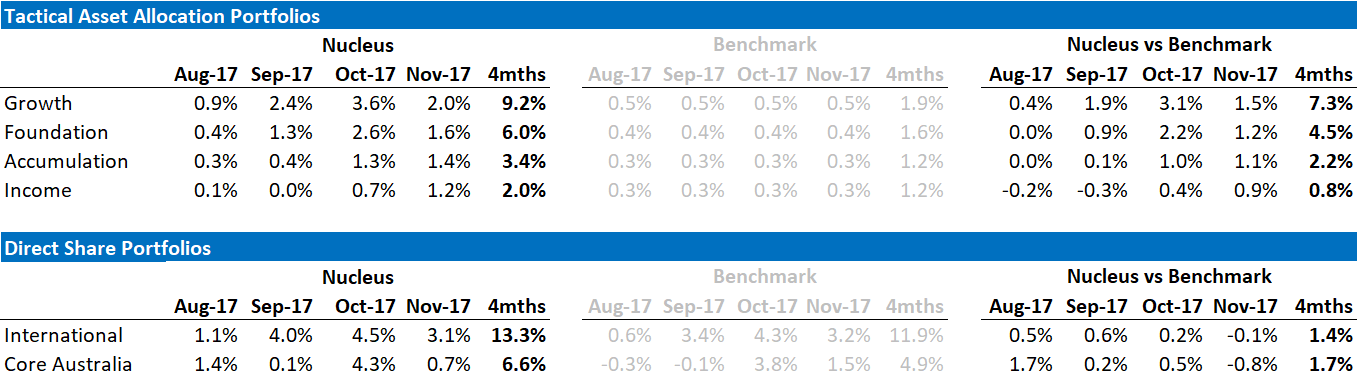

Here’s the recent fund performance:

Source: Linear, Factset

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. October monthly returns are currently at 4.9% for international and 4.2% for local shares.

If the themes in this post and the fund interest you then register below and we’ll be in touch:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. The MB Fund is a partnership with Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.