My new favourite economist, Damien Boey at Credit Suisse, has given the Australian outlook a complete rogering in the past few days. It began with his Q1 GDP tracker:

Growth momentum slows sharply in 1Q

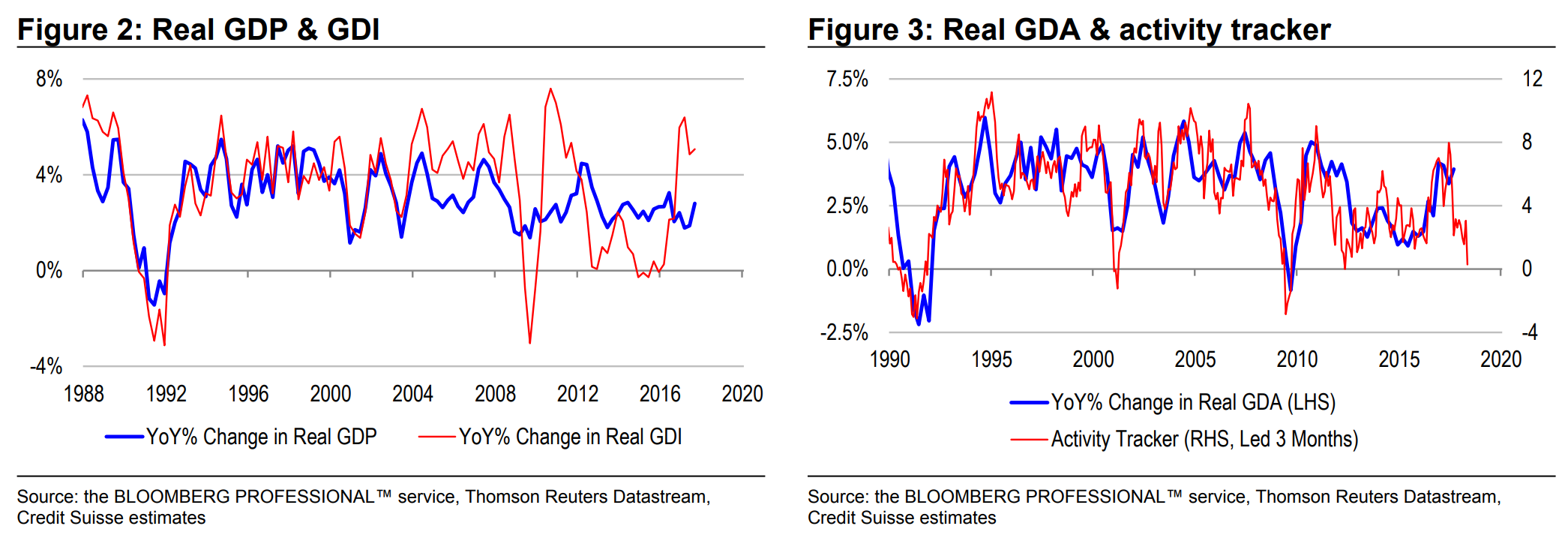

To help with stock selection, sector rotation and asset allocation decisions, it is important to be able to gauge the pulse of activity in real time, let alone forecast it. And for a small open economy like Australia, activity must be defined more broadly than production. Instead, a working definition of activity must also capture income transfers between Australia and the rest of the world via terms of trade movements. Our preferred measure of activity is real GDA—a blend of production (GDP) and income (GDI) concepts.

Of course, GDA is calculated from the national accounts and the national accounts are released with almost two quarters’ delay. Therefore, we need a real-time tracker of activity. We have constructed such a tracker using a wide array of partials:

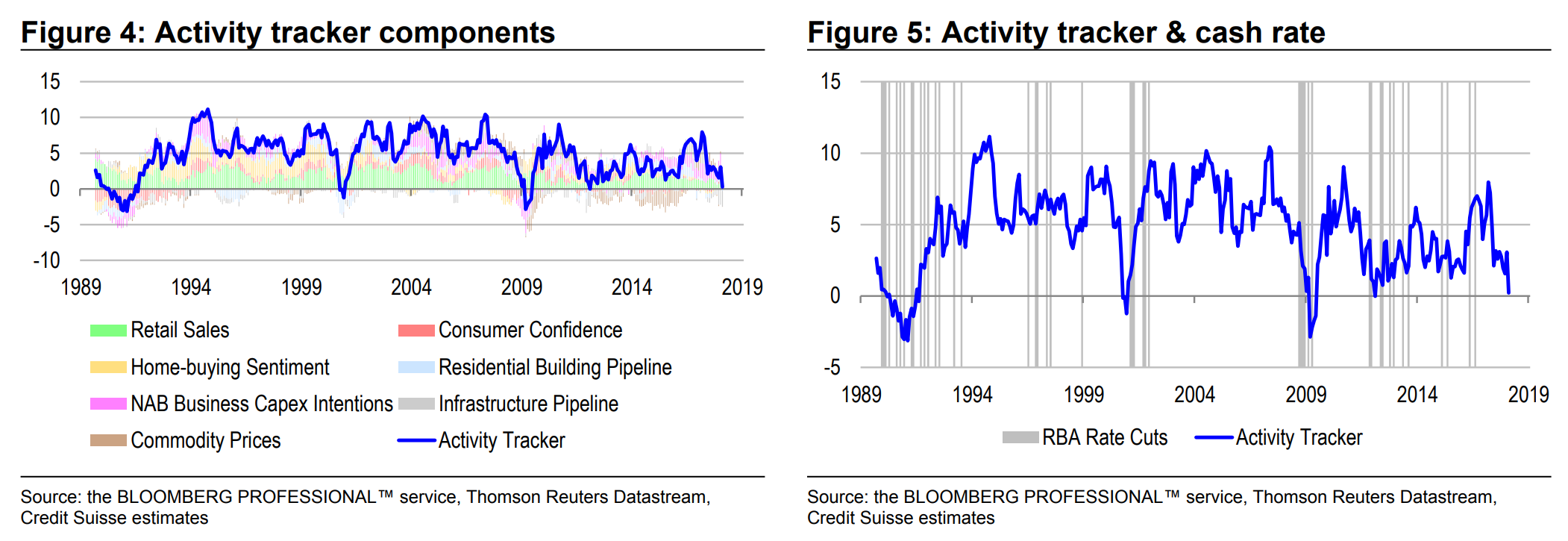

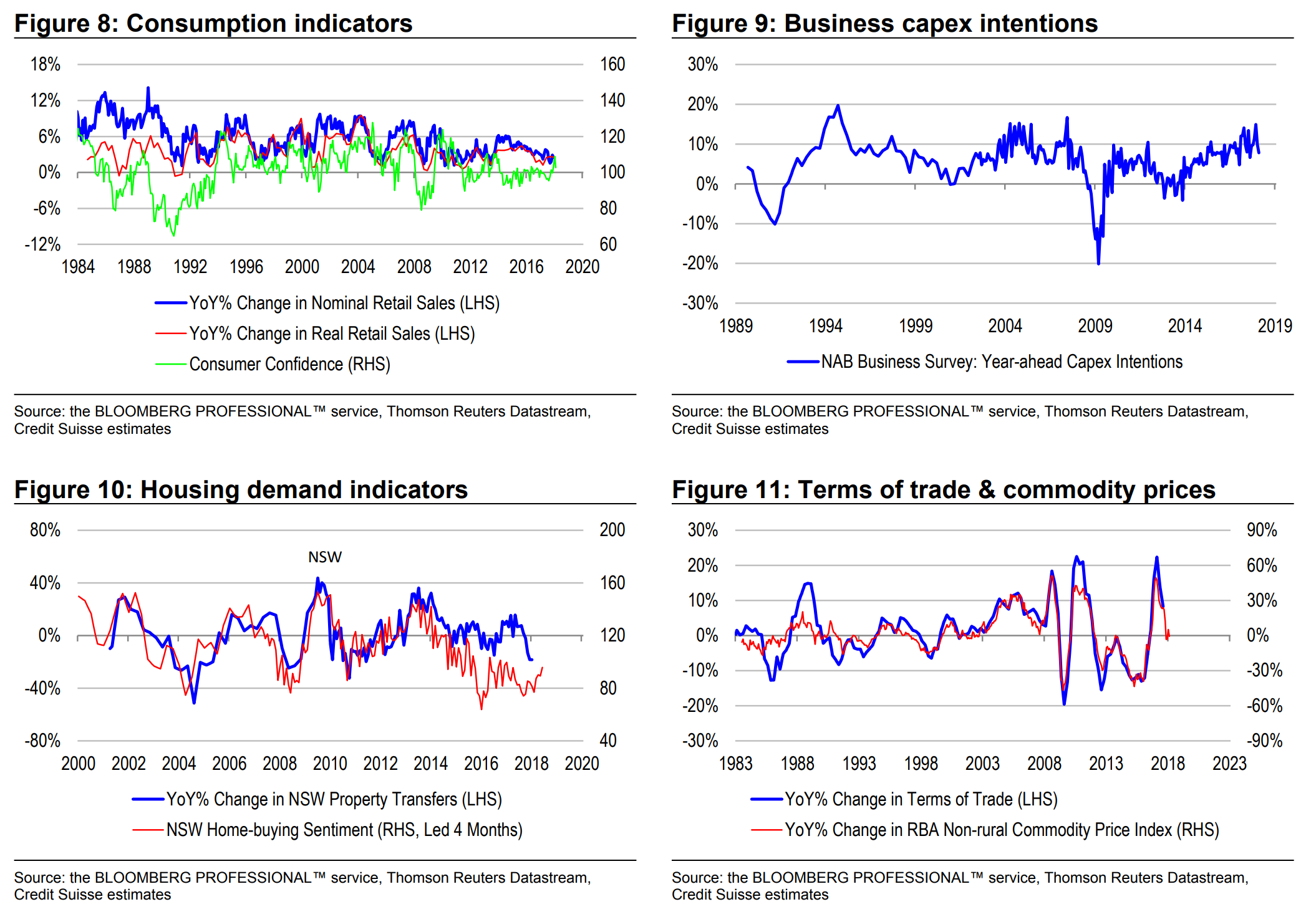

1. Trend retail sales growth, from the Australian Bureau of Statistics

2. Consumer confidence, taken from the Westpac Survey

3. Home-buying sentiment, taken from the Westpac Survey

4. Business confidence to invest, taken from the NAB survey

5. The depth of the residential building pipeline, measured as the spread between dwelling approvals and completions

6. The depth of the infrastructure spending pipeline, measured as the spread between project commencement and completions

7. Commodity price inflation, as measured by the RBA index Our tracker is the sum of these components, after standardising each of them by their historical volatilities. The tracker leads actual real GDA growth by roughly a quarter.

Our tracker has fallen sharply in recent times owing to:

1. Greatly diminished depth of the infrastructure spending pipeline. Project work done has increased very sharply throughout 2017, without many new commencements to keep up a strong pace of growth. Actual work done is now 33% below the level of commencements.

2. Sharp deterioration in forward indicators of residential building activity. Building approvals collapsed in December, with apartment approvals falling particularly sharply. Approvals are now running below completion levels, consistent with weakness in demand and prices.

3. Soft consumption indicators. Trend retail sales growth remains very soft, while consumer confidence relapsed in early February on share market weakness (after showing tentative signs of recovery in 4Q17).

4. Slowing business capex intentions. The NAB survey measure remains positive, consistent with capex growth. But growth seems to be slowing from a high base.

5. A flattening out in commodity prices. Although commodity prices have been on the rise since October 2017, they remain flat over the past year. This signals a trend flattening-out of the terms of trade as well. The tracker has now fallen close to zero, consistent with stagnation in real GDA. It is interesting to note that when this has occurred historically, the RBA has been cutting, rather than raising, rates in contrast to current market pricing.

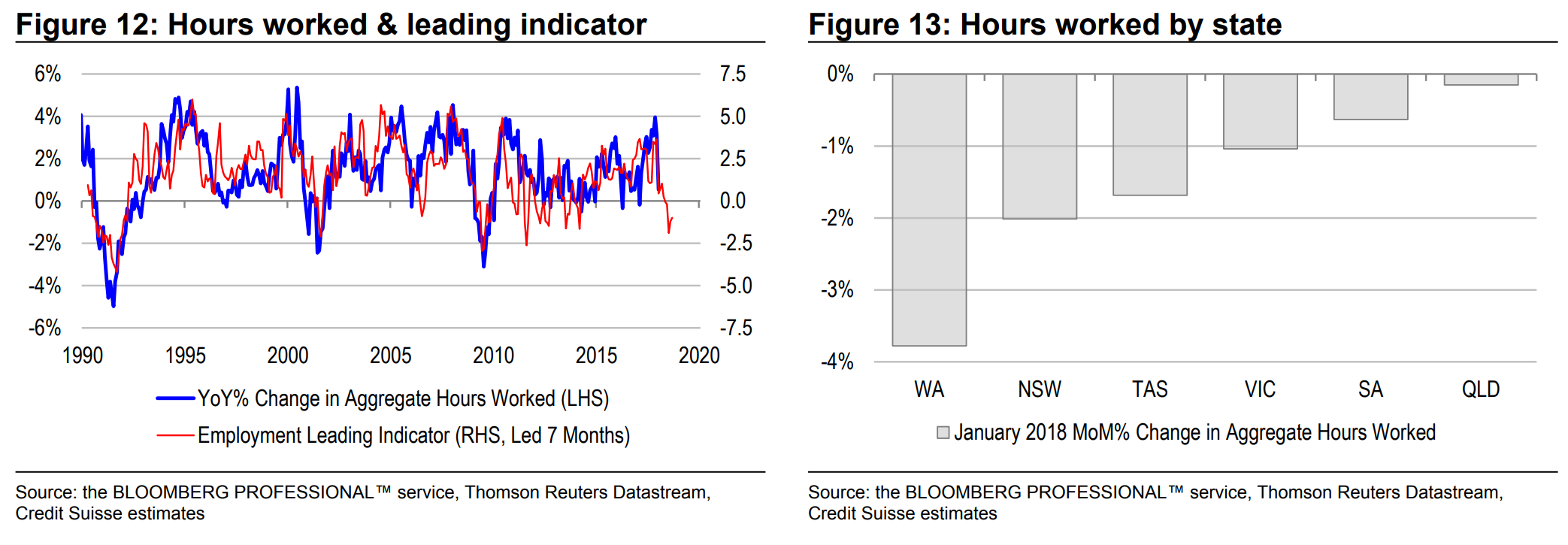

Employment growth slows sharply

Employment is normally a lagging indicator of activity. But the data are released with only a very short delay, and as such, can be used to corroborate signals from our activity tracker. Aggregate hours worked fell very sharply by 1.4% in January, following a sizeable 0.5% fall in December. Year-end growth in hours worked has slowed dramatically to a meagre 0.5% from a peak of almost 4% in November 2017.

We believe that this slowing is broadly consistent with what our tracker is suggesting. Indeed, our employment leading indicator based on a sub-set of activity tracker components (retail sales, business confidence and the depth of the infrastructure pipeline) has been pointing to a very sharp slowdown in job creation for some time. The concern for RBA officials is that real labour income growth is not improving to support consumption.

Moving from growth rates to levels, we note that full-time equivalent employment shares of the labour force and population dropped sharply in January. This is at odds with the NAB survey, which suggests that capacity utilisation rose to new cyclical highs. Looking across the labour market and survey-based measures of slack, the output gap remains quite wide. Our models are not raising alarm bells with regards to inflation.

Investment implications

Bond and money markets are suggesting that the RBA is likely to raise rates. Yet real-time activity trackers point to sharply slowing growth momentum. The disconnect is startling. If there is tightening on the horizon, it is not necessarily a sign of good growth. Alternatively, perhaps the economy is merely navigating a temporary soft patch. Our quantitative models suggest that there is sufficient reason to be contrarian and bearish, favouring quality exposures. One needs to have a very strong view about cyclical recovery to embrace value exposures at this juncture.

But wait, there’s more. Wage disinflation is about to get worse:

Desperately seeking wage inflation

RBA looking for signs of accelerating wage inflation RBA officials have repeatedly said that accelerating wage inflation is a trigger for rate hikes, especially if this is occurring against the backdrop of labour market tightening. Indeed recently, Governor Lowe has highlighted anecdotal evidence of pockets of labour market tightness in the economy, and building wage pressures therein. It is not just the mechanical influence of wages on CPI that the Bank is interested in. Rather, officials still believe in a traditional model of inflation based on slack in the economy, and are looking for signs that fundamentals are re-asserting themselves.

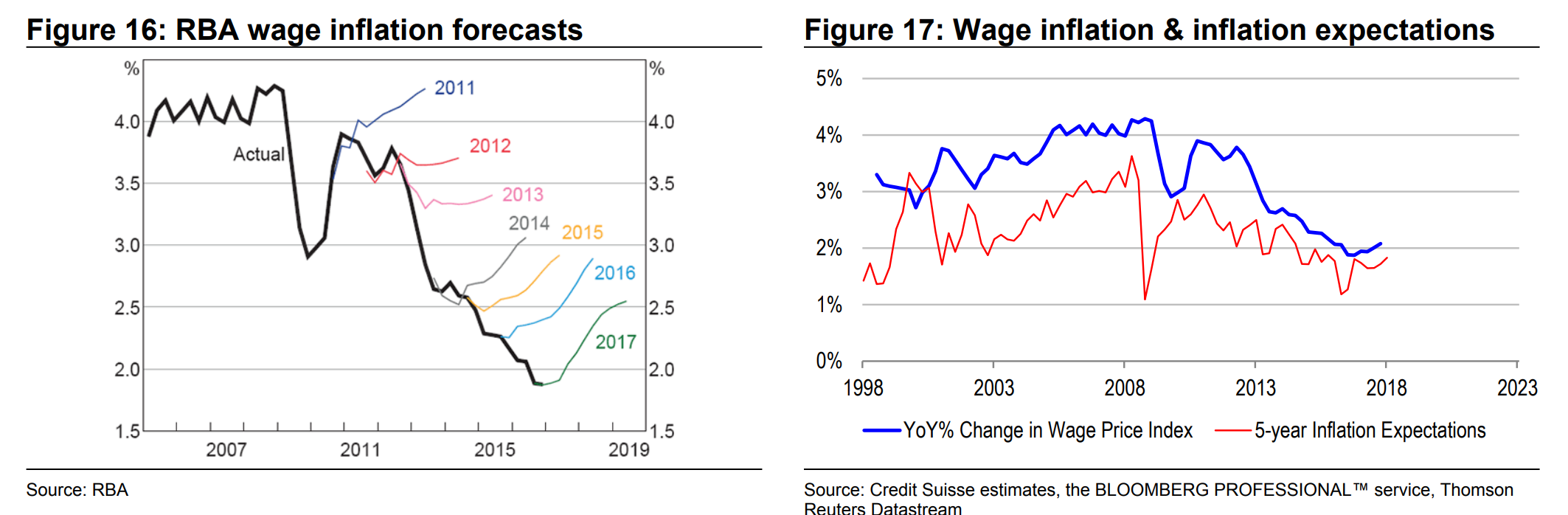

Interestingly, the Bank’s track record in forecasting wage inflation has not been great. Since 2011, officials have consistently over-predicted the pace of wage inflation. Whereas wage inflation has consistently slowed over the past few years, officials have consistently forecast acceleration. This has meant that subdued wage inflation has been something of a mystery for the Bank, and has forced officials to re-evaluate their analytical framework, or at least, the inputs they have been using. Over the past few years, staff efforts have concentrated on broadening the Bank’s concept of labour market slack beyond the unemployment rate, conventionally measured. This makes a lot of sense given that the inverse correlation between wage inflation and the unemployment rate has become much weaker through time. Officials have embraced concepts of underemployment and full-time equivalent employment to capture the slack masked by the unemployment rate.

The official view is that traditional inflation models still work, albeit with a longer lead time, and with wider uncertainty bands. Even if the economy were to reach full employment, it is possible that wage inflation may remain subdued for longer, in keeping with the global experience. But by the same token, if wage inflation were to pick up in the short term, perhaps the pace of mean reversion in the Bank’s inflation models could be seen as quickening again, supporting the case for tightening.

For now, officials seem quite uncertain about short-term prospects for a pick-up in wage inflation. They have a high conviction that wage inflation will gradually pick up in the medium term. But equally, they are creating room in their narrative for more disappointing data in the short term. In the February 2018 SOMP, we note that Bank officials inserted several dovish qualifications around their hawkish medium-term view of wage inflation:

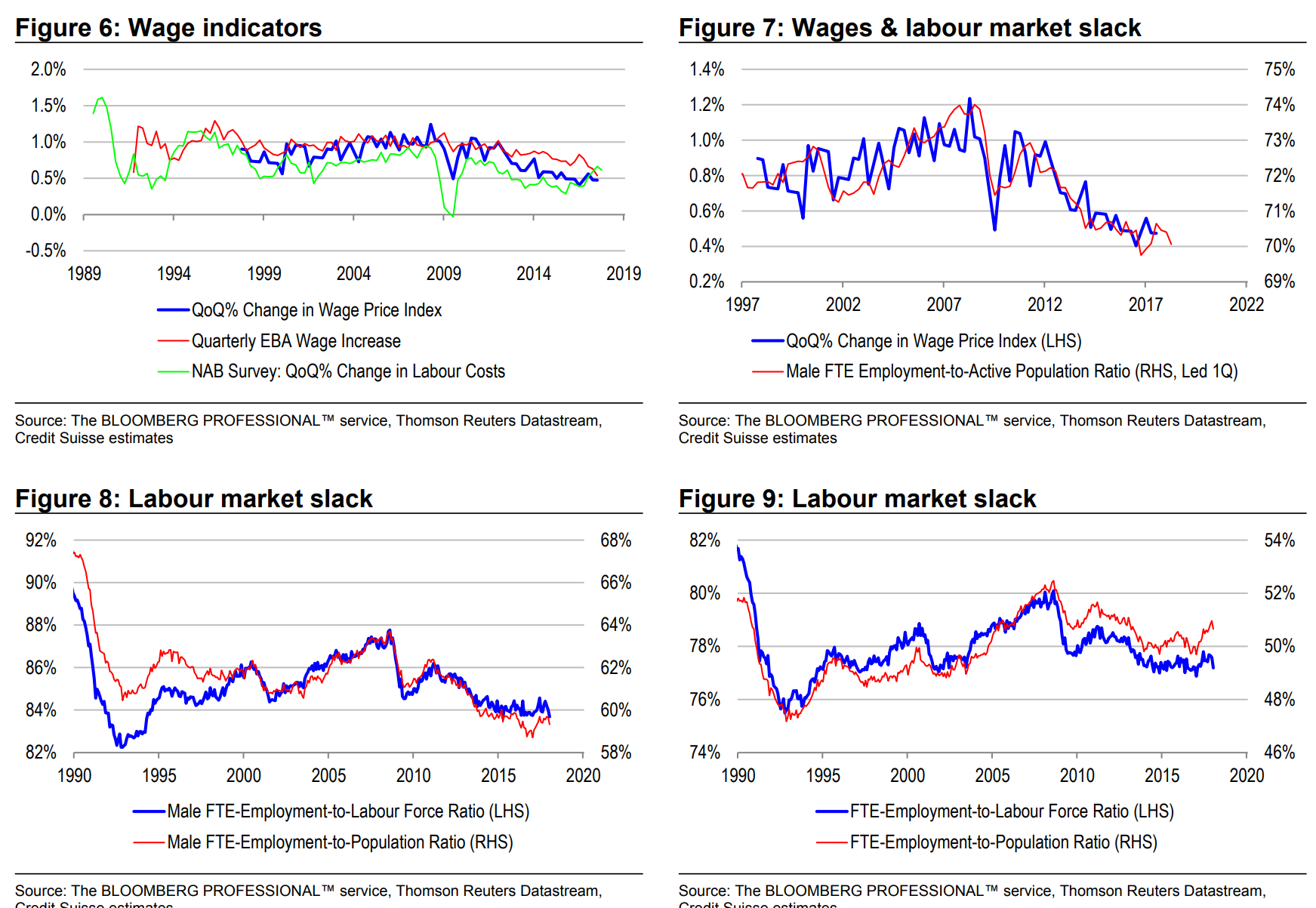

1. Subdued wage increases in recent enterprise bargaining agreements (EBAs): Despite sizeable minimum wage increases in 3Q, annualised EBA wage inflation slowed to new historical lows. As EBAs have an average duration of over three years, the Bank expects that average wage growth for those on EBAs will slow as current agreements are replaced by new agreements that have lower average wage growth outcomes.

2. Dispersion in wage indicators: The commonly followed wage price index is a composition- or quality-adjusted measure of wage inflation. However, average hourly earnings in the national accounts are not adjusted for mix-shifts in the labour force. Bank officials noted that average hourly earnings are growing at a much slower pace than the wage price index.

3. Compositional change dampening growth in average earnings: Not only are industry mix-shifts weighing on average hourly earnings, but subdued labour market turnover is also exerting a dampening influence. Bank officials note that wage inflation for employees remaining with the same employer has been much weaker than wage inflation for workers changing jobs. In this article, we explain why we do not think wage inflation will materially pick up anytime soon based on a model which has historically outperformed conventional models. Indeed, we think that wage inflation could actually slow further. Not only does this have implications for the timing of RBA rate adjustments, but it also has negative implications for the consumption outlook.

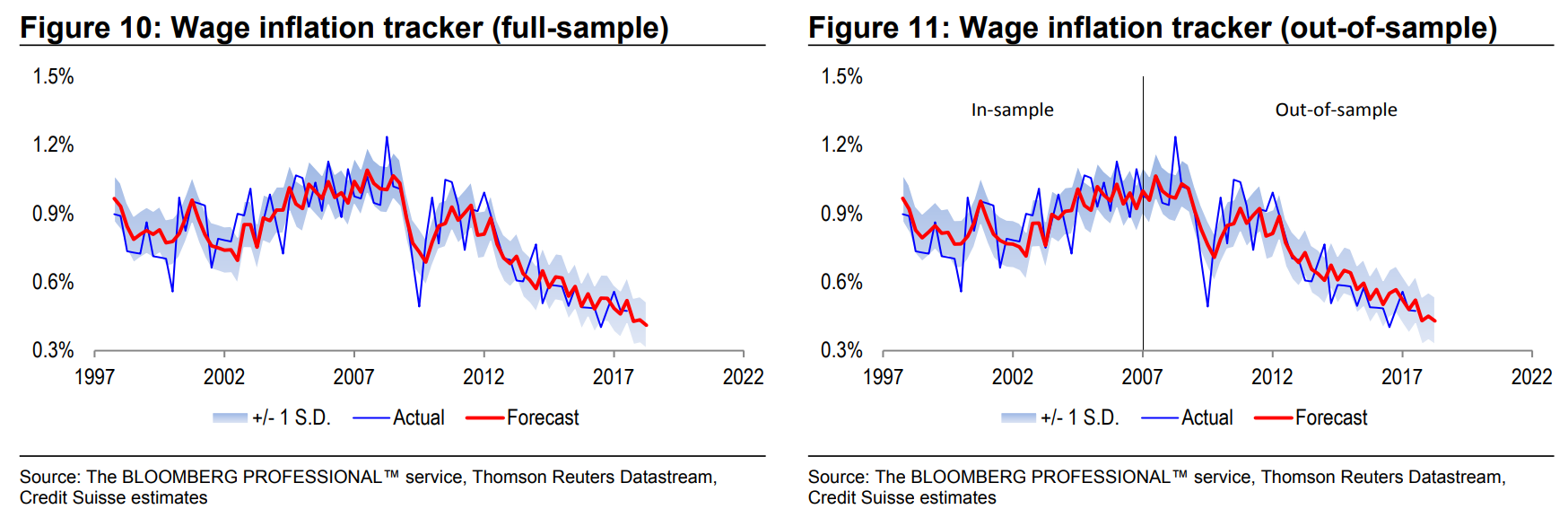

Wage inflation model points to further softness

We have constructed a real-time model of wage price index inflation using a combination of now-casts and fundamentals.

1. Now-casts: We use EBA wage increases, and reported increases in labour costs in the NAB survey to gauge real-time wage pressures.

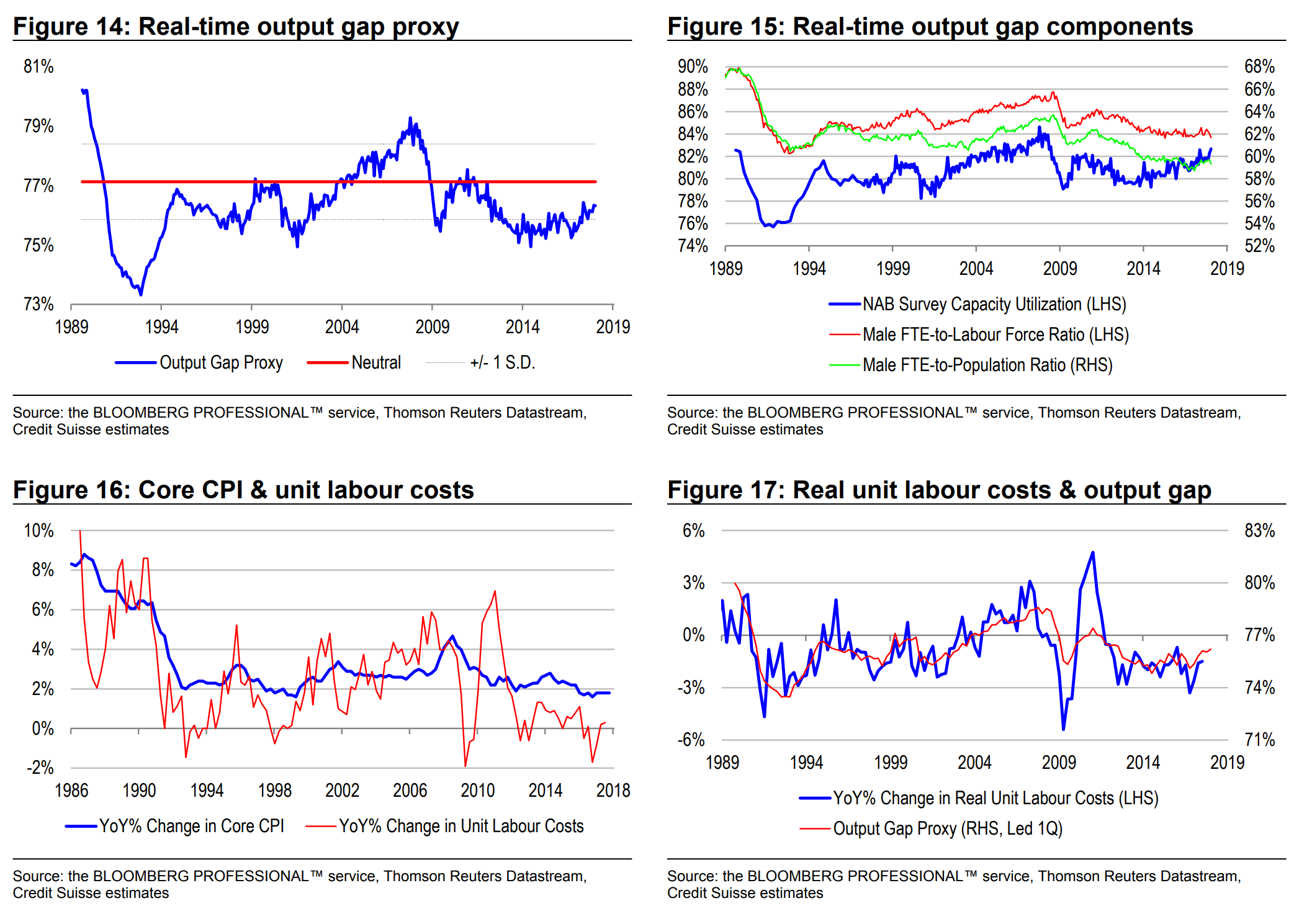

2. Fundamentals: We use a proprietary measure of labour market slack, based on male full-time equivalent employment as a share of the active population, to estimate labour market tightness, and the strength of wage bargaining power. In deriving our measure of labour market slack, we use average hours worked data to convert part-time employment into a full-time equivalent employment number. We use only male data to focus on cyclical developments, because the rise of female participation has had a structurally positive influence on the labour market. We are also agnostic as to whether it is the size of the official labour force, or the size of the civilian population which best captures of the pool of active labour. Therefore, we take an average of the two measures.

Another way of conceptualising our model is as follows. EBA and NAB survey-based measures of wage increases capture valuable information about worker inflation expectations and productivity growth, while our labour market slack indicator captures workers ability to get employers to reward these claims. Our model has good diagnostics:

1. Fit: It explains more than 70% of the quarterly variation in wage inflation since the inception of the data in 1997.

2. Statistical significance: All model parameters are statistically significant, and correctly signed. Faster (slower) EBA wage increases, NAB survey labour cost inflation and full-time equivalent employment growth (relative to labour supply) each lead to faster (slower) wage inflation outcomes.

3. Causality: There is evidence of Granger causality, because EBA wage increases, NAB labour cost inflation and our measure of labour market slack each lead quarterly wage inflation by roughly a quarter.

4. Stability: Model parameters are quite stable through time, as evidenced by reasonable out-of-sample forecasting performance over the past decade or so. Stability means that our model can be used for forecasting purposes, and has not been overfitted. One might argue that the strong forecasting performance of our model is due to the inclusion of “now-casting” variables. Indeed, the RBA in making its longer-term forecasts does not strictly have this information advantage. However, we find that historically, it has been our measure of labour market slack which has driven forecasting accuracy, rather than EBA wage increases or NAB survey labour cost inflation. As such, we think that our male full-time equivalent employment ratio is a superior measure of slack to the unemployment and underemployment rates.

Our model currently points to wage inflation slowing to an 0.4–0.45% quarterly pace (1.6– 1.8% annualised) all the way through to 2Q 2018. This is because:

1. Labour market slack has increased, with male full-time equivalent employment falling sharply in recent months, and the population growing solidly on the back of immigration.

3. Labour cost inflation in the NAB survey may be peaking.

Consensus is forecasting a 0.5% quarterly increase in wages in 4Q 2017. Some economists believe that there may be some technical payback for soft data in 3Q, with mandated minimum wage increases perhaps taking a longer-than-expected time to feed through to the data. For what it is worth, the Consensus forecast is above our mean forecast, but within a one standard deviation error band. It is distinctly possible that Consensus will be right in the very short term – but our point is that the trend in wage inflation remains remarkably subdued, and that we should therefore be careful not to extrapolate a trend from one data point. Indeed, we think that RBA officials have been quite clever in nuancing their short-term wage inflation views ahead of the release of the 4Q data.

Investment implications

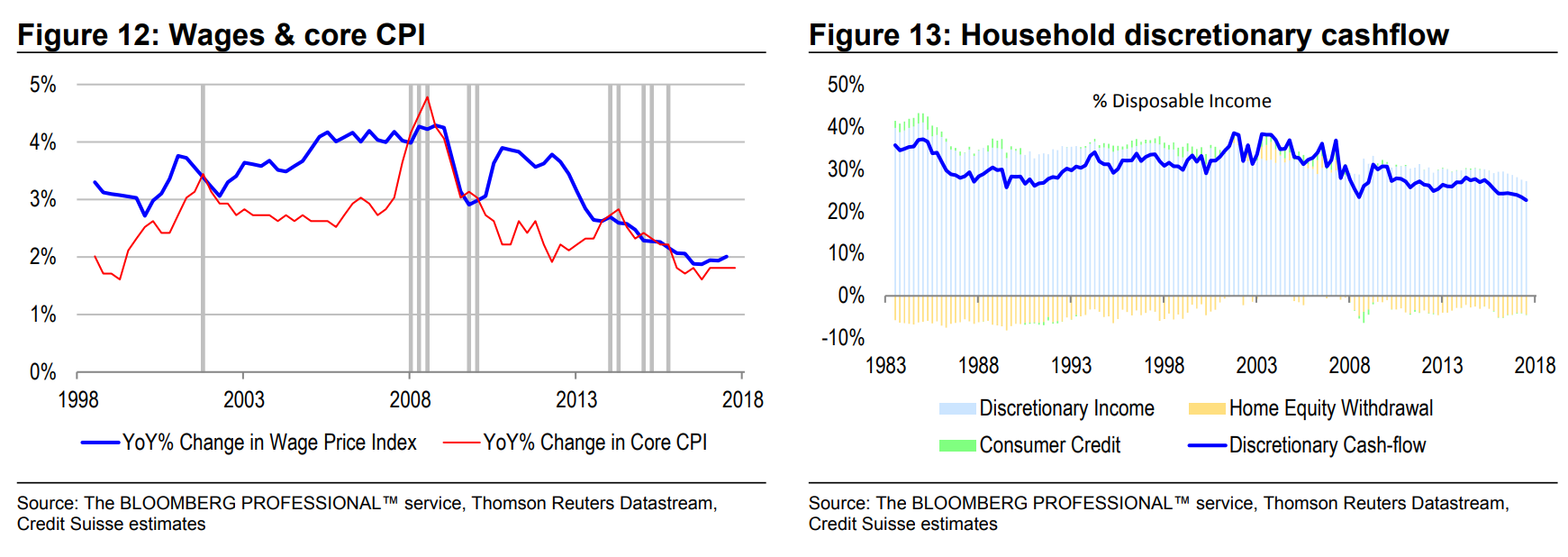

Most investors and market commentators are closely monitoring the 4Q wage data for clues on the timing of potential RBA rate hikes. However, we think that there is a risk of over-emphasizing one data point, because the underlying trend in wage is actually quite soft based on forward indicators. As it stands, RBA officials are backing away from strong short-term views on wage inflation. We think that the greater concern about soft and potentially slowing wage inflation is that it could weigh on the consumption outlook, especially when we consider that growth in hours worked is slowing sharply, and that house prices are declining moderately. Historically, whenever wage inflation has dipped below the pace of core CPI inflation, it is core CPI inflation that has adjusted lower. There are several explanations for this phenomenon – but the key one for us is that falling real wages represent a cash flow squeeze for consumers which weighs on spending growth, and eventually, firms’ pricing power. Indeed, our preferred measure of household discretionary cash flow (at an aggregate level) is currently at historical lows.

And, finally, one of the great recent serves for the RBA:

Why RBA forecasting errors matter A legacy of excessive optimism…

Everyone makes mistakes. The question is whether we learn from them. And we only tend to learn from our mistakes if we are held to account for them.

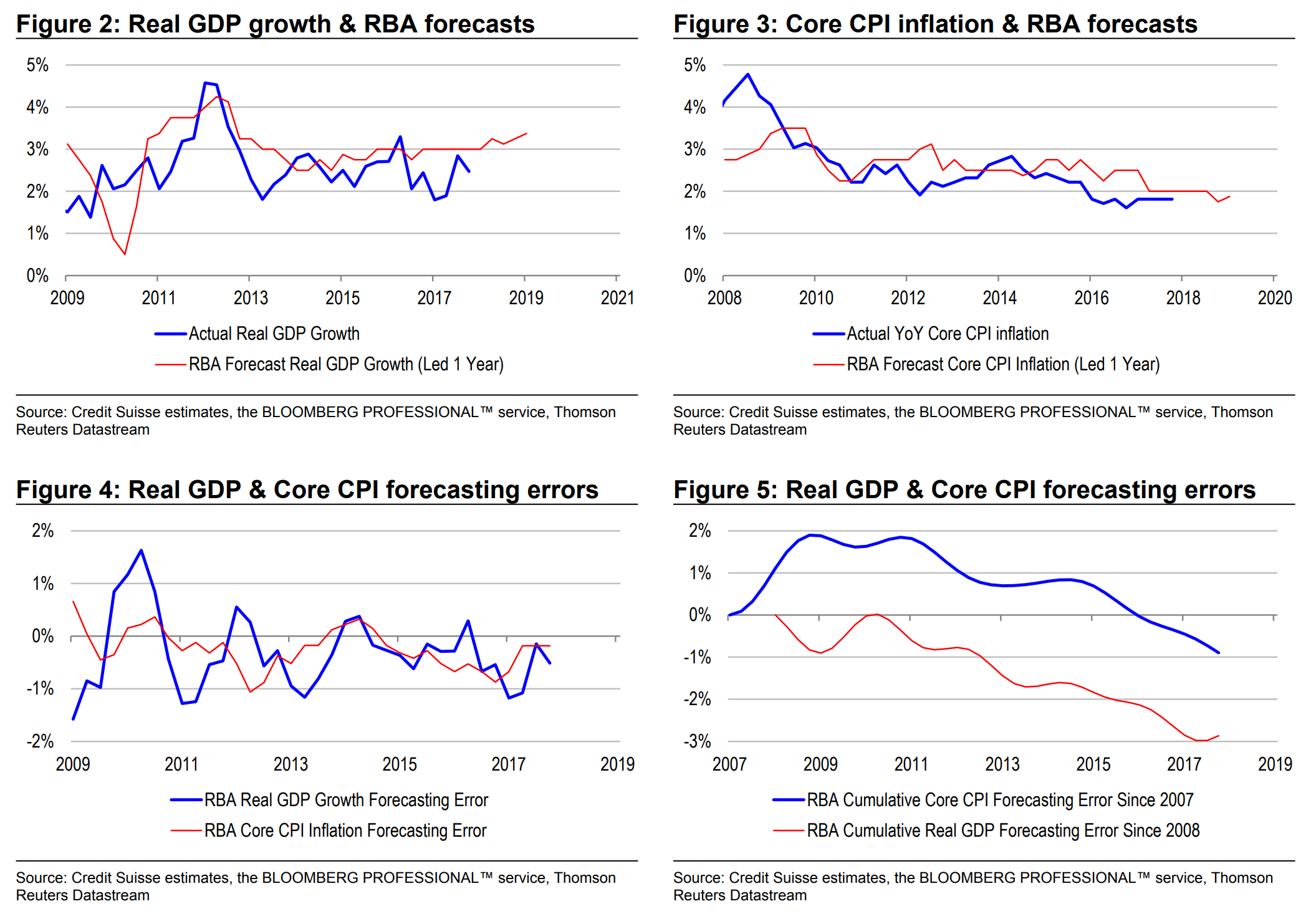

In this note, we examine the RBA’s forecasting track record on growth and inflation. The Bank has been publishing its official real GDP growth forecasts since 2008, and its official core CPI inflation forecasts since 2007. We have a short, but statistically meaningful sample to assess the Bank’s forecasting behaviour through various cycles.

Currently, the RBA is forecasting an uplift in real GDP growth to an above-trend pace of 3.25% in 2018 and 2019. The Bank is also forecasting a gradual uplift in core CPI inflation to 1.75% in 2018, and 2% in 2019.

Regardless of one’s personal convictions about where the cycle is at, none of this is very surprising. For context, the RBA has become renowned over the years for:

1. Delivering hawkish and arguably credible narratives, supported by…

2. Consistent upward inflection points in its growth and inflation forecasts, virtually dismissing near-term undershoots, resulting in…

3. Consistent over-prediction of real GDP growth and core CPI inflation. We can see that over-prediction has become a consistent problem on a one-year rolling basis since the European crisis.

We note that rolling one-year forecasting errors in real GDP growth and core CPI inflation are loosely connected through time. There is some correlation – but it is far from perfect, presumably because there are other factors that drive inflation apart from growth. That said, looking through the volatility, we also note that cumulative real GDP growth and core CPI inflation forecasting errors exhibit very similar profiles through time. In other words, in the medium term, over-optimism on growth is leading to over-optimism on reflation prospects.

…has seemingly gone unpunished

Seemingly, RBA officials do not seem to mind any of this. After all:

1. There is a false precision in forecasts, especially considering that there are already significant error bands in measuring yesterday’s growth and inflation.

2. The Bank is less wedded to setting policy on the basis of mean growth and inflation forecasts, and more focused on a balance of risks approach to rate adjustments. 3.

In Governor Lowe’s era, the RBA has explicitly said that it has an asymmetric response function to core inflation. The Bank is prepared to raise rates in response to (or in anticipation of) inflation overshoots – but it is not so willing to cut rates in response to (or in anticipation of) inflation undershoots, because at this juncture, the longer-term costs to financial stability arguably outweigh the shorter-term benefits from reflation.

Most importantly, the bond market has continued to give the Bank the benefit of the doubt, with longer-term inflation expectations remaining relatively well anchored over the past few years, despite a legacy of persistent inflation undershoots. So far, it appears as though the bond market has not held the RBA accountable for its forecasting errors. Going one step further, there has been no real market compulsion for the RBA to change its forecasting process, nor re-assess the credibility of its hawkish narratives.

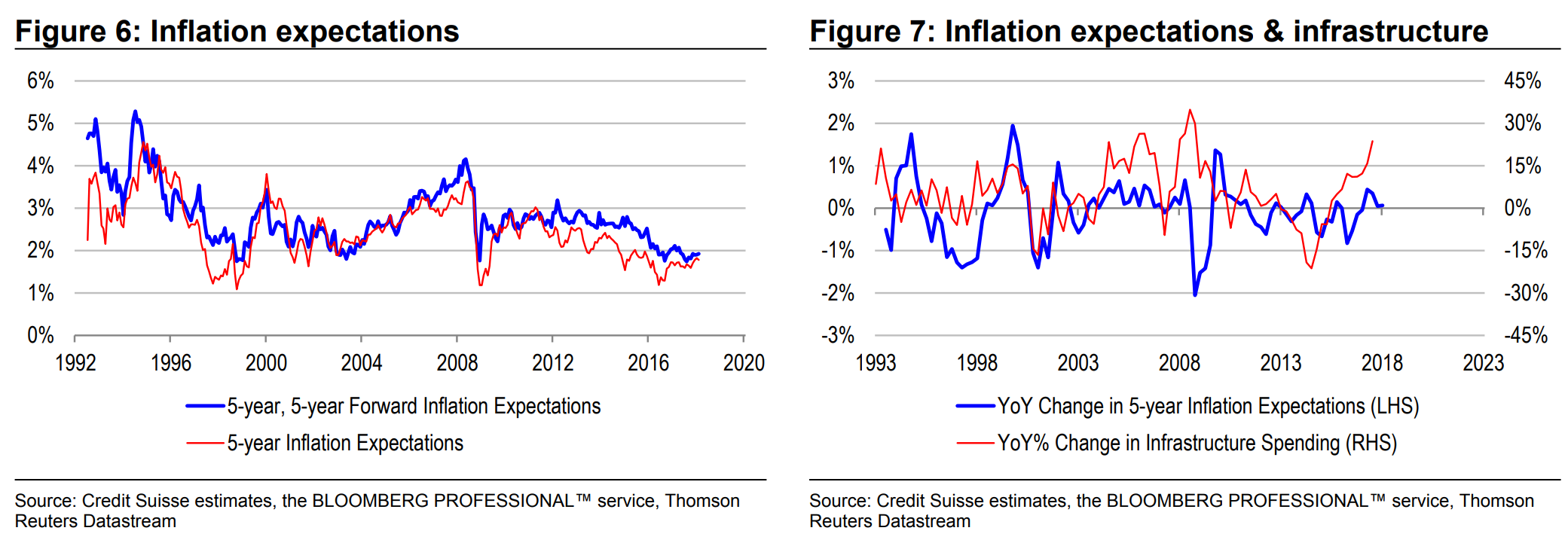

But looking a little deeper, we think that there is indeed evidence that the bond market is starting to take notice, and that the RBA’s forecasting misses are starting to matter from a credibility perspective. After all, while 5-year, 5-year forward inflation expectations remain close to 2%, they have fallen to the lower bound of the RBA’s target zone. We also note that apart from the RBA’s inflation targeting credibility, there are other factors which drive inflation expectations:

1. Global factors: The bond market behaves as if inflation is “always and everywhere” a monetary phenomenon. Stronger global inflation expectations and USD weakness tend to drive up commodity prices, which in turn boost Australian national income via the terms of trade, and headline CPI.

2. Domestic fiscal policy: Just as bank loans create deposits, fiscal spending (on overdraft-like terms with the RBA) creates deposits. It is possible for the government to ramp up inflation independently (and arguably more effectively) than the central bank simply through deficit spending.

In our view, these factors have masked the loss of RBA inflation targeting credibility in bond market pricing over the past few years. But if the RBA continues on its merry way, lost credibility may become a more significant factor weighing on inflation expectations and bond yields, notwithstanding how global factors evolve. This means that either the Bank materially revises down its forecasts (and adjusts rates accordingly) to win more credibility, or fiscal policy makers need to take on more responsibility to help keep inflation within the target band.

But bond market investors are starting to notice

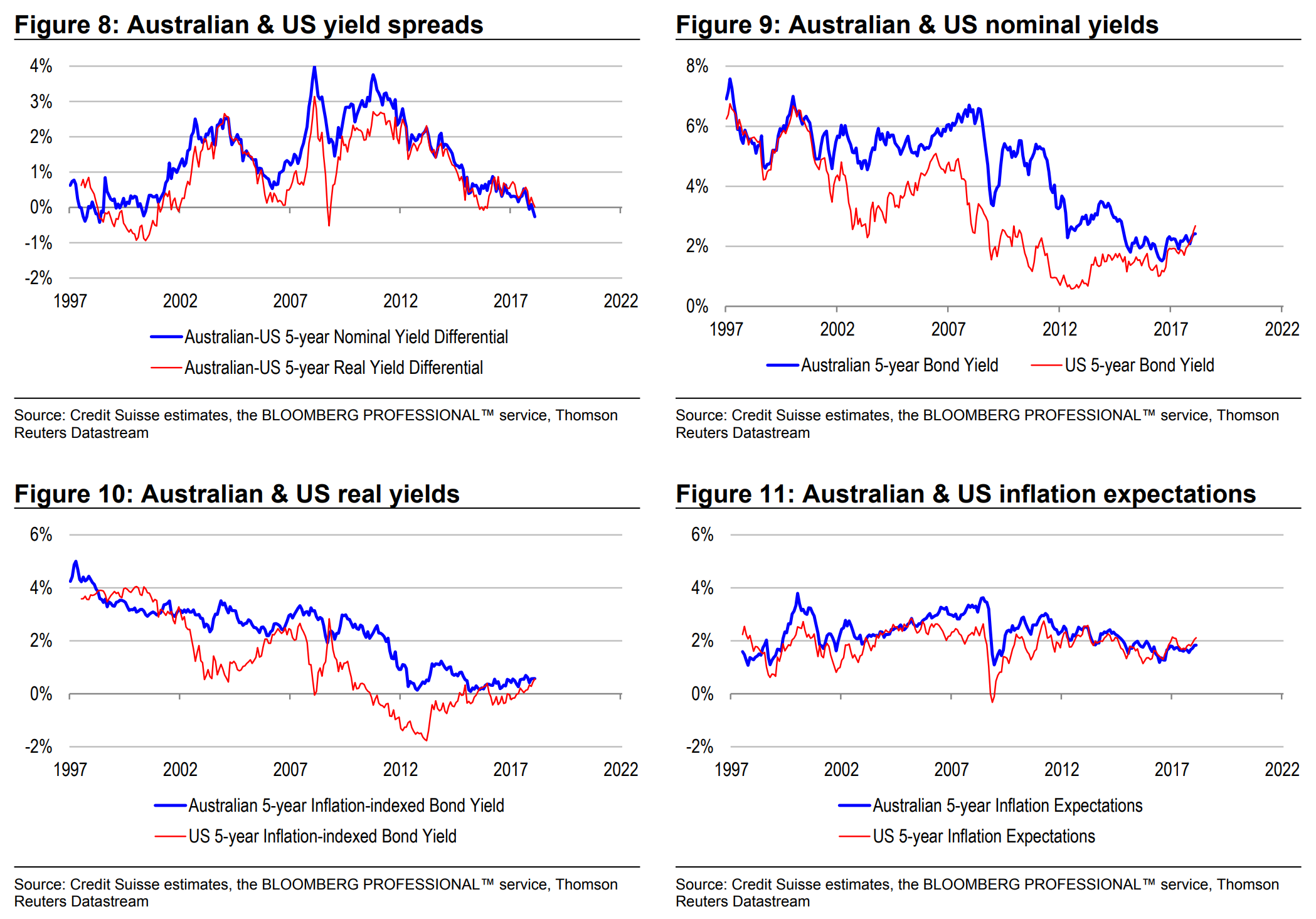

We can control for the influence of global factors on Australian bond market pricing by looking at Australian-US bond yield differentials. In other words, we can make the simplifying (but valid) assumption that all other things being equal, there is a one-for-one correlation between Australian and US yields. We can go one step further, and apply this logic to the components of bond yields – real, or inflation-indexed yields, and breakeven inflation expectations.

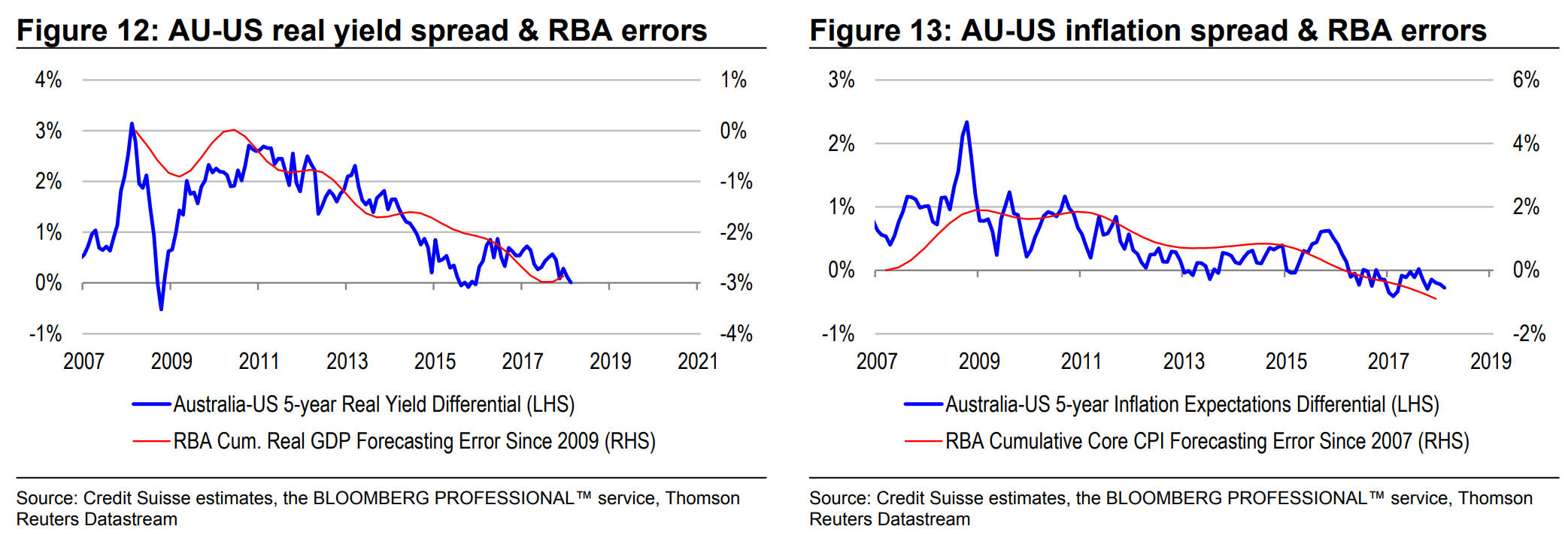

Interestingly, 5-year Australian-US real yield differentials are positively correlated with the RBA’s cumulative real GDP forecasting errors. Similarly, 5-year Australian-US inflation expectation differentials are positively correlated with the RBA’s cumulative CPI inflation forecasting errors. All of this means that it is not only marginal forecasting errors which 23 February 2018 Australian Quantitative Macro 5 impact the Bank’s credibility (after adjusting for global factors). Rather, it is the legacy of errors which starts to add up in the minds of investors. This is not a problem if through-the cycle, the Bank manages to achieve growth outcomes around potential, and inflation outcomes within the target band. But if it consistently misses, then investors could start to respond by adjusting their real terminal rate and inflation forecasts embedded in bond yields.

Considering that growth and inflation have been consistently undershooting the RBA’s forecasts over the past few years, we believe the Bank must do more than just achieve a few “quick wins” to steady the ship. Rather, we think it must achieve consistent growth and inflation overshoots to right previous wrongs, and restore credibility. In this context, we note that even if the RBA were to achieve its current inflation forecasts in the next year, cumulative inflation surprise would continue to drift lower, because current forecasts are still below previous forecasts.

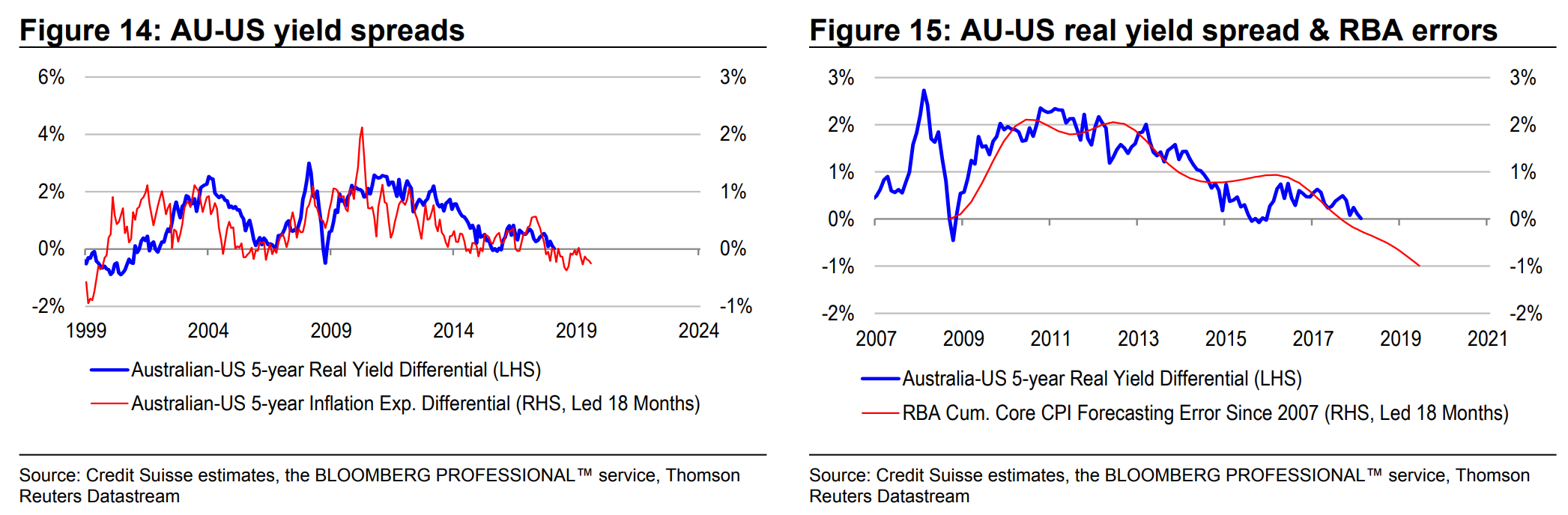

While we often think of real yields and inflation expectations as unrelated, history tells us that there is actually significant cross-over between the two components. Australian-US inflation expectation differentials tend to lead Australian-US real yield differentials by more than a year. In other words, the RBA has historically been quite sensitive to global and inflation developments at the margin, and has been prepared to adjust real rates accordingly. This means that the RBA’s cumulative misses in forecasting core CPI inflation actually matter for real yields, and not just inflation pricing. Indeed, if historical relationships are anything to go by:

1. Real yield differentials have quite some room to invert over the next few years.

2. The RBA may eventually be forced to respond to consistent inflation undershoots, despite current claims to the contrary.

The key question in this context is whether or not there has been a regime change in the Lowe era. Hawks argue that there has been a change, because the RBA has now incorporated an asymmetric response function to inflation. But we believe that there has not been a regime change – only a convenient set of circumstances to support the claim. Our fundamental issue is that for a given level of rates, falling inflation, and inflation expectations imply rising real after tax interest rates, which are a form of tightening on the economy. We think that this helps to explain why historically, Australian-US inflation expectations differentials have led real yield differentials.

To be sure, not all forms of disinflation or deflation are created equal. For example, falling prices for discretionary items, such as plasma screen televisions, may not cause households to indefinitely defer their expenditure and borrowing in anticipation of things getting cheaper in the future. But if inflation expectations more generally are low and falling, the market is suggesting that borrowing appetite is receding, and that rate settings need to reflect this reality. In this context, there are lessons that we can draw from the Japanese experience with deflation, even though Australian demographic trends are far more supportive of inflation than those in Japan.

A more direct way of seeing this tightening is in subdued wage inflation. Historically, we know that:

1. Wage inflation has consistently undershot the RBA’s forecasts, much like real GDP growth and core CPI inflation.

2. Wage inflation and bond market inflation expectations are highly correlated.

If indeed sluggish wage inflation is a problem for highly leveraged consumers, and RBA forecasting errors are contributing to low wage inflation by allowing growth and inflation expectations to become unhinged, then it stands to reason that officials bear some responsibility for anaemic consumption growth. It is not just that policy makers have underestimated the degree of slack or competitiveness in the labour market, leading to wage inflation undershoots. Rather, officials also need to entertain the possibility that inadequate forward guidance has undermined credibility to the point that it is now feeding into the wage bargaining process.

For example, highly geared households may value job stability over wage claims in order to sustain their debt load over time. And the evidence is that if they value job stability, they are unlikely to secure very large wage increases relative to their peers who change jobs more frequently. The premium for job stability increases when growth undershoots, because it becomes much harder to find new work opportunities, and risk appetite falls.

Investment implications

At a surface level, it might not look as though the bond market is noticing consistent growth and inflation undershoots relative to RBA forecasts. Also, it might not look as though the RBA will remove the classic Australian “upward inflection” in its growth and inflation forecasts any time soon. But we think that the legacy of undershoots matters, and is starting to manifest in bond market pricing. We think that:

1. Inversion of Australian-US bond yield differentials, and

2. Inversion of Australian-US inflation expectation differentials

are telling us that net of global factors, bond market investors are discounting the RBA’s credibility to achieve growth and inflation stability. Workers are seemingly doing the same. To right the wrongs, we think that it is not enough for the Bank to temporarily hit its forecasts. Rather, consistent overshoots are needed to reverse consistent undershoots. If the RBA embraces this thinking, it will likely re-shape expectations for rate adjustments over the next few years.

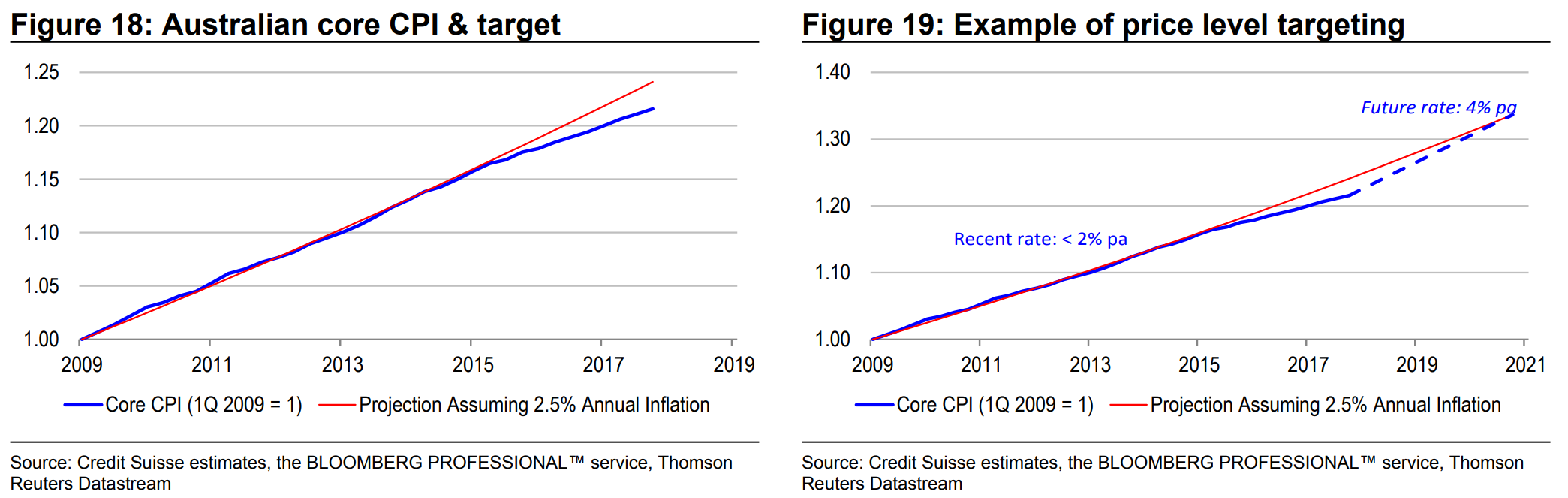

All of this resonates with Former Fed Chair Bernanke’s proposal for “price level targeting” as a way of lifting inflation expectations. A price level target is a stronger commitment from the central bank to preserve price stability than a simple inflation target. Whereas an inflation target focuses on a current rate of change in CPI, a price target focuses on the trajectory of the CPI level, and encompasses past and future over- and under-shoots. An inflation target lets “bygones be bygones”. If the central bank consistently misses its target, the misses are quickly forgotten, and everyone simply rolls forward their forecasting window, regardless of the cost to credibility. But a price level target forces the central bank to reverse undershoots with future overshoots. By implication, the central bank may have to deliberately, and credibly allow itself to fall behind the tightening curve.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Interestingly, the Bank’s track record in forecasting wage inflation has not been great. Since 2011, officials have consistently over-predicted the pace of wage inflation. Whereas wage inflation has consistently slowed over the past few years, officials have consistently forecast acceleration. This has meant that subdued wage inflation has been something of a mystery for the Bank, and has forced officials to re-evaluate their analytical framework, or at least, the inputs they have been using. Over the past few years, staff efforts have concentrated on broadening the Bank’s concept of labour market slack beyond the unemployment rate, conventionally measured. This makes a lot of sense given that the inverse correlation between wage inflation and the unemployment rate has become much weaker through time. Officials have embraced concepts of underemployment and full-time equivalent employment to capture the slack masked by the unemployment rate.