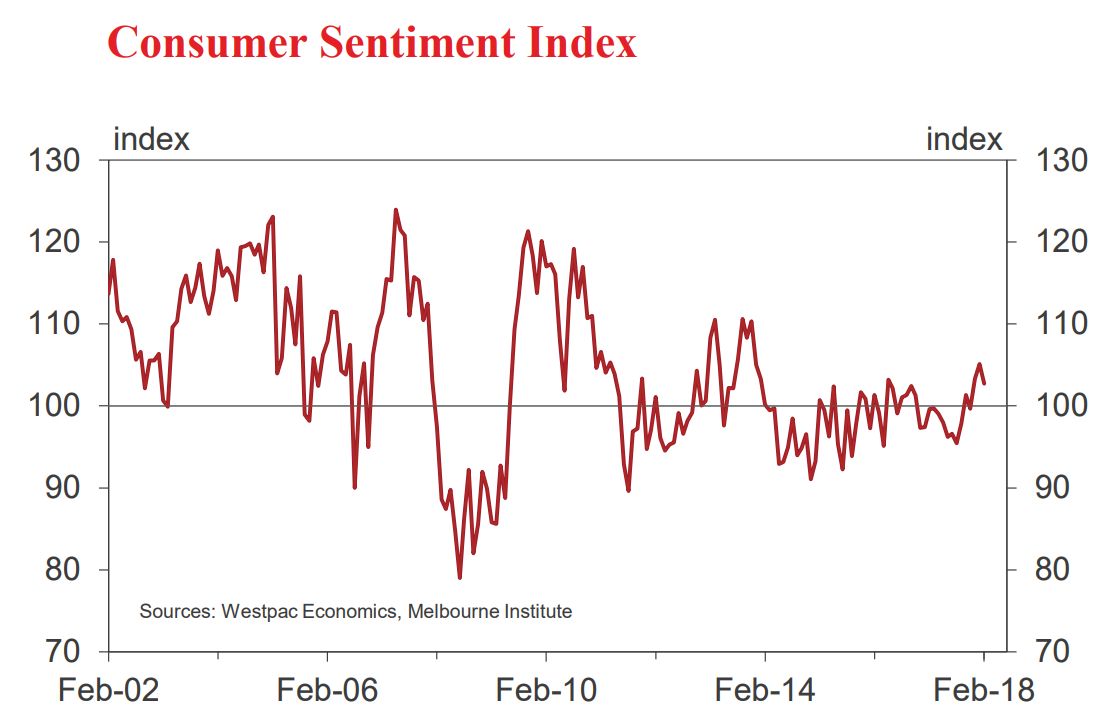

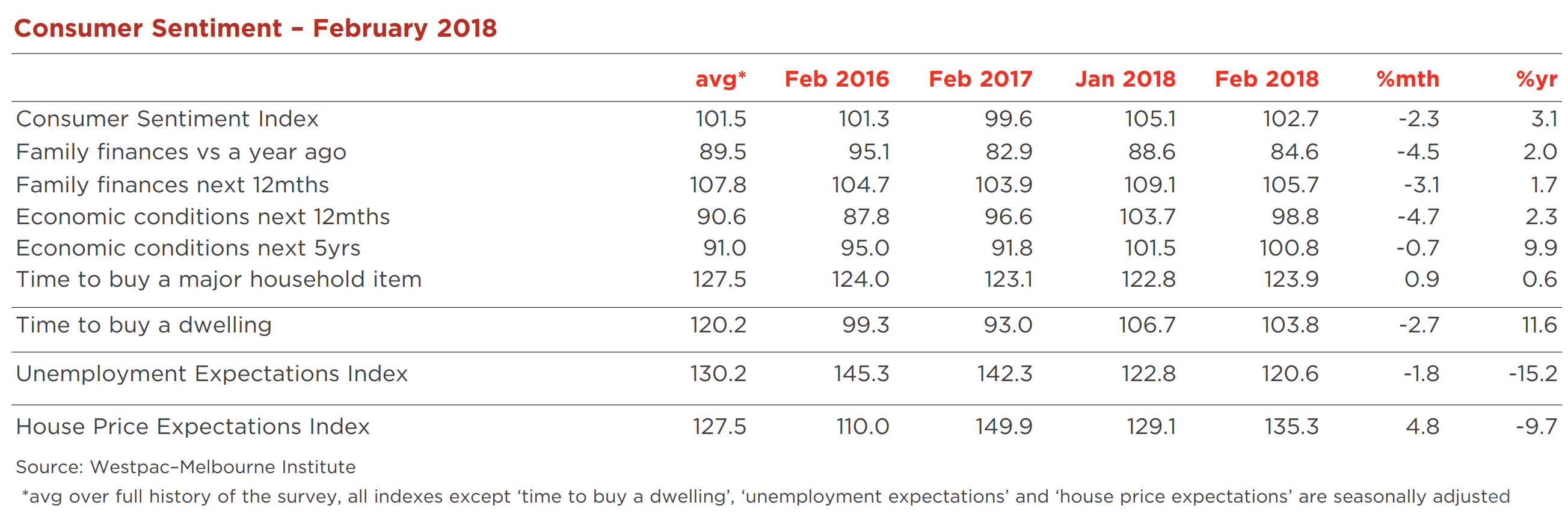

• The Westpac Melbourne Institute Index of Consumer Sentiment fell by 2.3% to 102.7 in February from 105.1 in January.

The survey was conducted over the week of February 5 – February 11. That week was marked by a wave of volatility in global share markets. The Australian market, which was more stable than most, still experienced some significant swings, being down a net 4.6% for the week while the US market (S&P 500) was down by a net 7.2%.

Extensive media coverage of these developments would have unnerved respondents on two fronts – the impact on their own financial position and concerns for general global stability.

These concerns appear to have been acutely felt by retirees whose confidence fell by 13.5%.

In those circumstances the 2.3% fall in the Index is a decent result and is now registering a fourth consecutive month where optimists outnumber pessimists. Recall that this sequence follows 12 consecutive months where pessimists were in the ascendency for all but one month.

Having said that the level of the Index is still well below levels typically associated with a robust consumer.

Every six months we gauge respondents’ outlook for interest rates. In August last year 61% of respondents expected interest rates to rise over the next year. That was an uplift from 54% in February 2017. The proportion has fallen back to 58%, partly explaining the boost to confidence since the middle of last year.

Developments in the components of the Index are consistent with the likely impact from last week’s market volatility. In particular respondents’ assessments of their own finances suffered, the ‘finances vs a year ago’ subindex fell by 4.5%; and the ‘finances, next 12 months’ sub-index fell by 3.1%. We assume that these components have suffered temporary set- backs associated with market volatility. On face value the ‘year ago’ component is sending a very weak signal about likely spending prospects.

Not surprisingly the ‘economic conditions, next 12 months’ component fell sharply by 4.7% while the ‘economic conditions, next 5 years’ component was stable.

The ‘time to buy a major Item’ sub-index increased by a modest 0.9%. Despite the overall Index still being 3.1% higher than a year ago this component is only up by 0.6% over the year – signalling ongoing reluctance from households to commit to large purchases.”

Consumers continue to become more comfortable about the outlook for jobs. The Westpac Melbourne Institute Unemployment Expectations Index declined 1.8% to 120.6 in February to a new cycle low (recall that lower reads mean more consumers expect unemployment to fall in the The Index, which can be viewed as a measure of consumers’ sense of job security, is down 15.2% on this time last year and well below its long run average of 130.

The state detail shows the improvement has become more broadly based as well with all state indexes now comfortably below their long run averages. Consumer views around housing showed mixed moves with buyer sentiment softening but price expectations improving. The ‘time to buy a dwelling’ index declined 2.7% to 103.8 in February but was coming off an 18 month high in January. The index is still showing a clear improvement on last year’s very weak reads (an average of 95.7 for 2017) but is well below the positive long run average of 120. The state detail shows a significant pull-back in Victoria (down 12.7% to 93). In contrast, there was a notable lift in NSW buyer sentiment (up 7% to 96) having been at much weaker levels through 2017 (an average of 82).

The Westpac Melbourne Institute Index of House Price Expectations rose 4.8% to 135.3, reversing all of last month’s decline to be back comfortably above its long run average. The biggest gain in February was in NSW although price expectations in the state are coming from a weaker starting point and still show the biggest pull back on this time last year.

The Reserve Bank Board next meets on March 6. In a speech on February 8 the Governor concluded, “the Reserve Bank Board does not see a strong case for a near term adjustment in monetary policy”.

Clearly there will be no policy change at the March meeting.

Through 2017 Westpac has argued for rates to remain steady in 2017–2019. The Bank expects to make some progress in reducing unemployment and having inflation return to the midpoint of the target range. However, based on its recent forecasts that were released on February 9 that progress is expected to be painfully slow. Underlying inflation is expected to reach only 2%, the bottom of target range, through 2019 and the unemployment rate is expected to fall from 5.5% to 5.25% (compared to an estimated full employment rate of 5.0%) by end 2019.

While we are less optimistic about the unemployment rate and the growth outlook the Bank’s forecasts are not entirely out of line with our own view and, arguably, consistent with steady rates over the next few years

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.