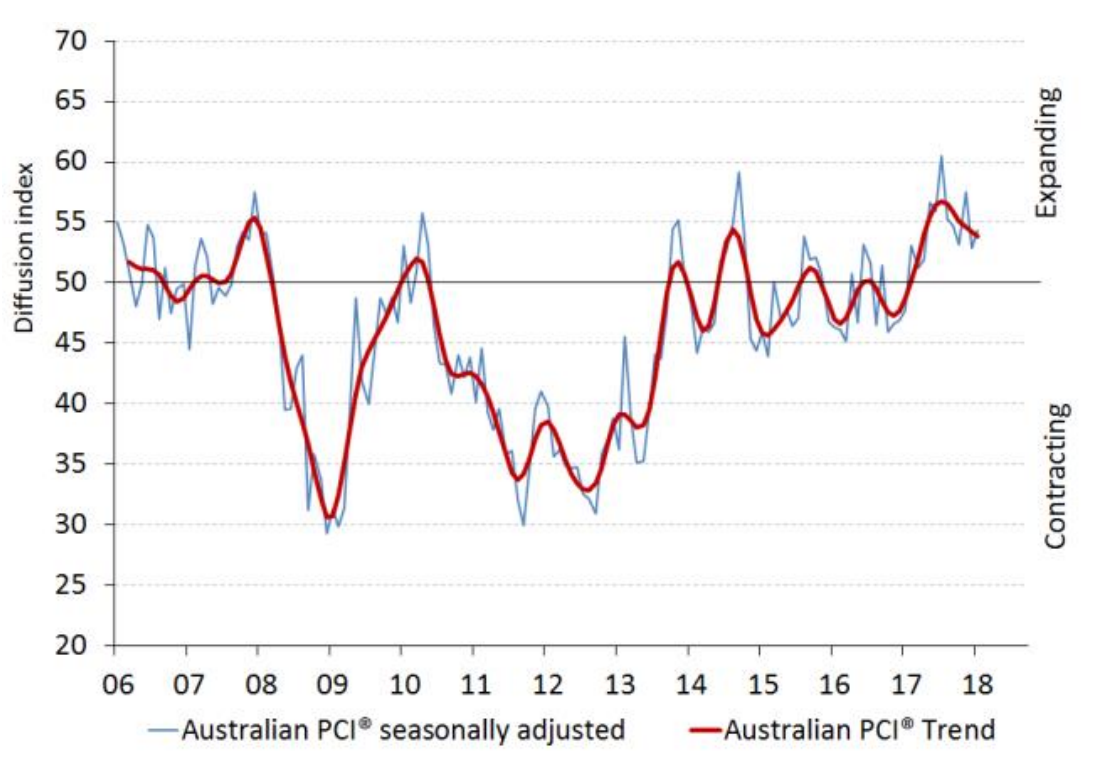

▪ The seasonally adjusted Australian Industry Group/Housing Industry Association Australian Performance of Construction Index (Australian PCI®) increased by 1.5 points to 54.3 points in January (readings above 50 points indicate expansion). This signalled industry-wide growth for a 12th consecutive month and at a slightly higher pace than in December 2017.

▪ Australian PCI® data for January revealed an improvement in demand, with the new orders sub-index returning to growth after drifting into mildly negative territory in December.

▪ The activity sub-index remained in expansion in January, at a broadly unchanged rate from December. This was associated with further growth in deliveries from suppliers.

▪ The employment sub-index accelerated to its fastest pace in six months, while capacity utilisation hit a record high of 83.4% (highest since at least 2008, when this data series began).

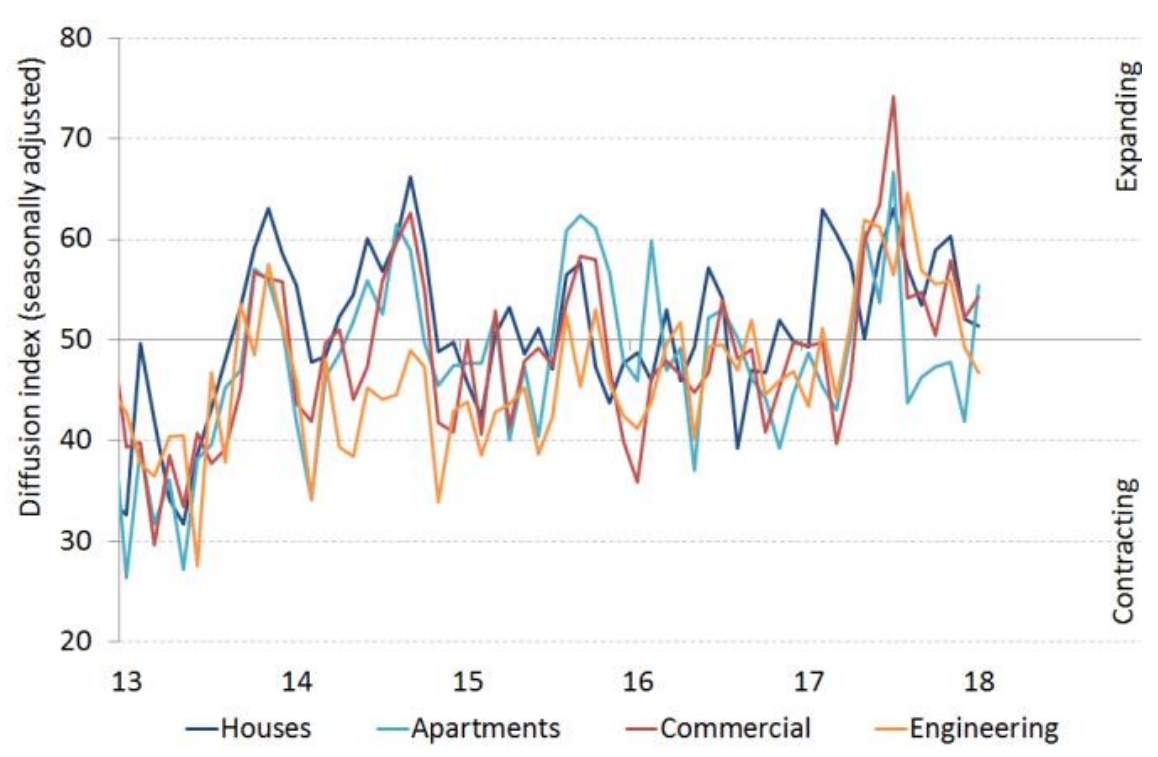

▪ Across sectors, commercial construction was the strongest performing area of industry activity in January with its sub-index jumping 7.4 points higher to 58.9 points, in line with stronger property investor sentiment and improving business conditions more generally.

▪ House building activity continued to expand although the sector’s rate of growth moderated for a second consecutive month, signalling a possible cooling in house building conditions.

▪ Engineering construction expanded at a slower rate. However, January marked the sector’s 10th consecutive month of expansion amid ongoing support from major infrastructure projects.

▪ Apartment building activity remained in positive territory in January, although the implied rate of growth was marginal and unchanged from December.

▪ House builders continued to point to a high degree of support from ongoing projects, although there were reports of slower new orders and fewer enquiries about house constructions.

▪ Respondents active in commercial and engineering construction continued to cite the positive influences on activity from rising investment in commercial building developments and major infrastructure projects underway, particularly on the east coast.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.