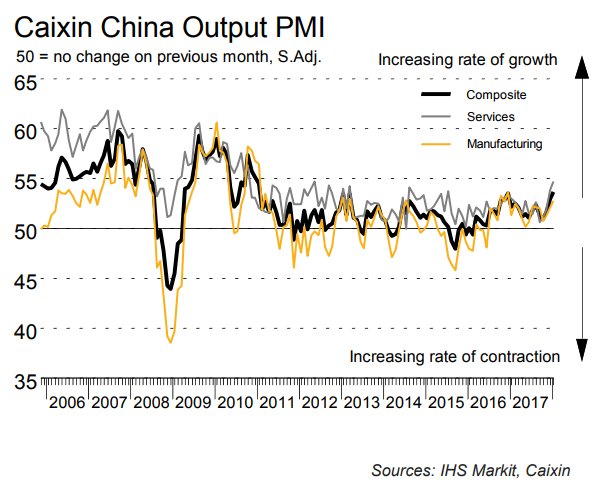

The Caixin China Composite PMI™ data (which covers both manufacturing and services) indicated that growth momentum across China picked up for the third straight month in January. Furthermore, the Composite Output Index rose to a seven-year high of 53.7, from 53.0 in December, to signal a solid pace of expansion.

January survey data signalled accelerated rates of activity growth across both the manufacturing and service sectors in China. The steeper pace of expansion was registered by services companies, which saw the most marked increase in activity since May 2012. This was highlighted by the seasonally adjusted Caixin China General Services Business Activity Index posting 54.7 at the start of 2018, up from 53.9 in December. At the same time, manufacturers signalled the quickest upturn in production levels since December 2016.

Similar to the trends for activity, both service providers and manufacturers noted a further increase in new business during the opening month of the year amid reports of firmer client demand. Furthermore, new order growth accelerated to a 32-month record across the service sector. Meanwhile, goods producers registered a modest increase in new work that was softer than in December. At the composite level, total new orders rose at a solid pace that was similar to that recorded at the end of 2017.

Employment data continued to signal divergent trends, with rising headcounts at services companies contrasting with further job cuts at manufacturers. Service sector staff numbers have now risen for seventeen months in succession, with some firms adding to their payrolls due to greater business requirements. Moreover, the rate of job creation edged up to a five-month high. Manufacturing workforce numbers meanwhile declined at the softest pace for nearly three years. As a result, composite employment rose slightly, after broadly stagnating between August and December last year.

After falling in each of the prior four months, backlogs of work were unchanged at services companies in January. In contrast, manufacturers signalled sustained pressures on operating capacity, with outstanding work rising for the twenty-third month in a row and to the greatest extent since March 2011. Consequently, unfinished business rose at a stronger, albeit modest, pace at the composite level.

The rate of input price inflation continued to soften across China’s manufacturing sector at the start of the year. Though sharp overall, the pace of increase was the weakest since last August. Service providers meanwhile registered a faster rise in cost burdens, with the rate of inflation the steepest since April 2012. Nonetheless, the marked slowdown in the manufacturing sector led composite input prices to increase at the slowest pace for five months.

Despite strong cost pressures, manufacturers and service providers raised their output charges at softer rates in January. In fact, selling prices rose only marginally in both cases. At the composite level, average charges increased at the slowest pace in seven months.

Chinese companies were generally optimistic that activity would increase over the next 12 months. However, improved confidence across the manufacturing sector (four-month high) contrasted with a slight dip in sentiment at service providers (four-month low). Nonetheless, expectations remained relatively subdued across both sectors compared to their long-run trends.

I don’t often discount data but I’d take this one with a grain of salt given slowing credit and the Winter shutdowns.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.