By Gareth Aird, Senior Economist at CBA

- We expect the fifth estimate of 2017/18 spending plans to come in at $111bn.

- Our forecast is for the actual volume of Q4 capex to 1.7% which would leave annual growth 5.2% higher.

- We receive a first estimate of 2018/19 spending plans.

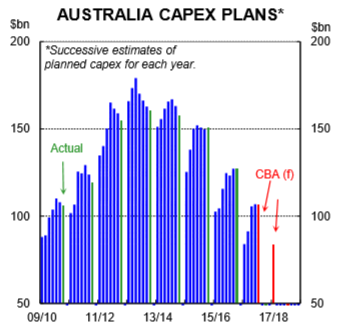

There are three key figures in this week’s capex survey (i) Q4 2017 actual spending; (ii) 2017/18 expectations (5th estimate); and (iii) 2018/19 expectations (1st estimate). Markets will focus on the forward looking expenditure plans, particularly the first cut of 2018/19 spending intentions.

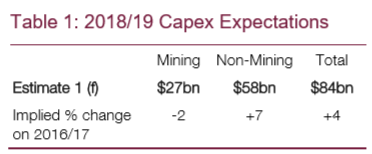

2018/19 expectations (1st estimate) – see table 1.

First estimates for spending plans can vary significantly from actual spending. A comparison of previous first estimates with actuals shows that non-mining firms will almost always underestimate their capex plans at first stab. But the magnitude of the miss can vary greatly in any given year. As the economic landscape changes, capex spending plans evolve accordingly. The first estimate is often revised up sharply if demand lifts. Mining firms, on the other hand, have tended to more accurately estimate their capex plans over the past few years – basically since the peak in the investment boom.

Our forecast is for nominal capex, as measured by the survey, to lift by 4% in 2018/19 (comprised of a 7% increase in non-mining investment and a 2% fall in mining capex). For that to materialise, we are looking for the first estimate of 2018/19 capex spending plans to come in around $84bn. We would interpret a figure above $57bn for non-mining spending plans as a good outcome as it would imply a respectable pickup in capex outside of the resources sector (note that our pick of $58bn would be a strong outcome). Mining continues to fall as a share of total capex and the drag on growth from falling resources investment is largely done.

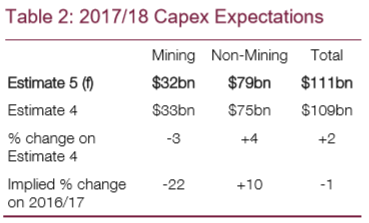

2017/18 expectations (5th estimate) – see table 2.

The last reading from three months ago implied a small of around 1% in nominal capex this financial year. The detail suggests a fall in mining capex of 22% and a healthy 10% increase in non-mining investment. Here we note that the capex survey only captures around 60% of business investment as per the national accounts. The survey excludes a number of large and important industries which include agriculture, health and education.

Q4 2017 actual

We expect the actual volume of Q4 capex to rise 1.7% after a 1.0% increase in Q3. Such an outcome would leave annual growth 5.2% higher. The actual spending data will help firm up our estimates of Q4 GDP growth (due 7 March).

Risks

Global growth has picked up and local employment growth has been strong. On balance, these factors point to upside risk on our 2017/18 capex expectations. There are a wide range of estimates for the 2018/19 forecast. At $84bn, we sit a touch below the median forecast of $86.5bn