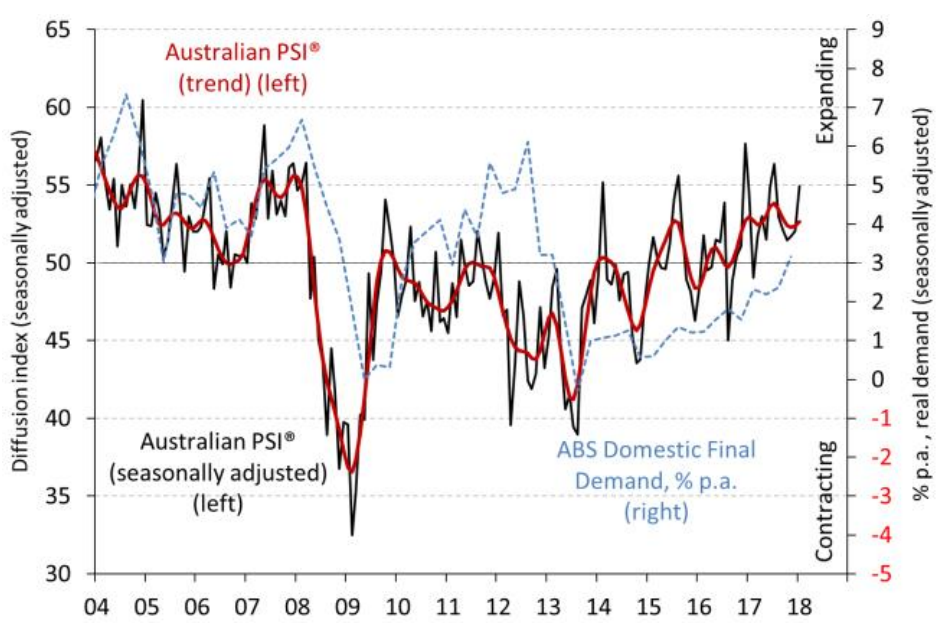

• The Australian Industry Group Australian Performance of Services Index (Australian PSI® ) increased by 2.9 points to 54.9 points in January 2018 (seasonally adjusted), indicating a faster rate of expansion from late 2017. Australian PSI® results above 50 points indicate expansion, with higher numbers indicating stronger rates of growth.

• January 2018 marked eleven consecutive months of positive results in the Australian PSI® (seasonally adjusted), the longest such run since March 2008 (18 months).

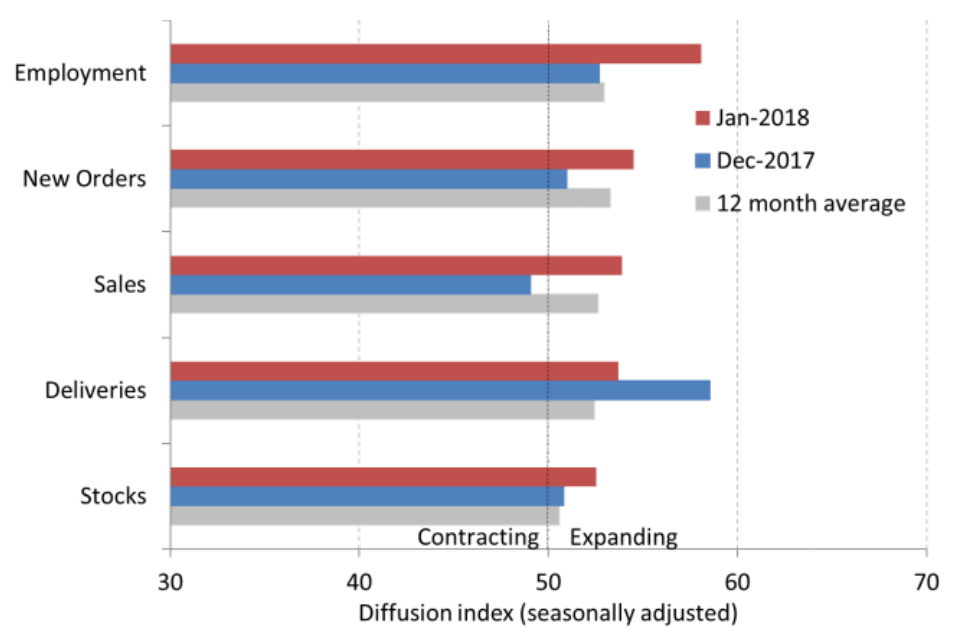

• All five of the activity sub-indexes in the Australian PSI® expanded (results over 50 points) in January 2018. The employment sub-index was especially strong in January. It lifted by 5.4 points to 58.1 points, its highest monthly result since December 2004. Employment was stronger across all services sub-sectors except wholesale trade in the Australian PSI® in January. Capacity utilisation is also relatively elevated at 81.1% of available capacity in January, just shy of its peak of 81.4% in August 2017.

• The Australian PSI® continues to show considerable variation in activity across subsectors in January, as it did through 2017. Conditions are generally looking better in the business-oriented sub-sectors than in consumer-oriented sub-sectors. Three of the nine sub-sectors expanded in January (transport, finance, property & business), two were approximately stable (hospitality and personal services) and four contracted (wholesale, retail, communications and health, education & community services).

• Respondents to the Australian PSI® noted improved business confidence and orders from business customers in January, boosted by a rebound in real estate transactions in some locations. Excessive heat was a plus for some businesses, as more customers sought out air-conditioned shops, restaurants and recreation services. Stronger labour demand is evident in the increase in reports of skill shortages in specialized fields.

• Businesses across all sub-sectors continue to report problems absorbing higher input costs including higher energy costs and annual increases in regulatory costs. These cost rises are eating into margins and increasing pressure to raise selling prices.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.