The Aussie dollar has returned to its shock absorber roll, tumbling again overnight to hit its lowest point in 2018:

It was aided by relatively dovish comments from RBA head Phil Lowe but the US stocks crash played the major role, deterring forex risk as well.

Deutsche reckons (quite rightly) that the Aussie dollar shock absorber is back in action:

Advertisement

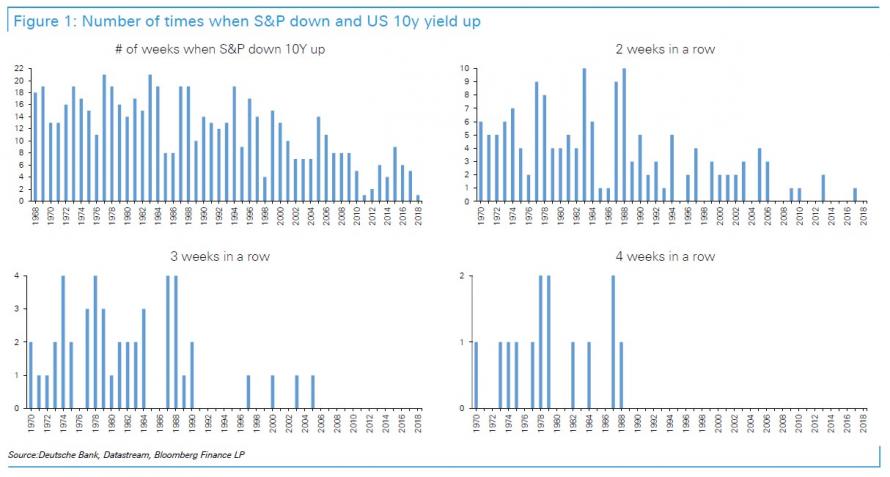

Three weeks of equities down, 10y yields up, has not happened for more than a decade.

Bond and equity prices falling sharply on the week may feel like an unusual environment, because in the last decade, it has become unusual. However, especially as we go back to the 1980s and 1990s it was a more frequent occurrence to see the following causal chain develop: Equities go up, supporting growth with a lag, pushing bond yields up, to the point where higher bond yields eventually pull equities down. In this way the equity – bond causality and correlation shifts, from a positive correlation where equities drive up yields, to a negative correlation as bond yields take the causal lead in pushing equities down.

From a macro perspective what is intriguing about this dynamic is two old school factors could be back in play: i) At least in the US there is a confluence of inflationary factors – lagged demand, tight labor markets, the tax reforms impact on wages/bonuses and growth, higher oil prices, latent protectionism, and the weak USD. All these factors are apt to have a cumulative effect, chipping away at global disinflation and inflation inertia. ii) the Fed and other Central Bank’s balance sheet adjustments, may signal the end of financial repression, and this repression likely helped risk parity trades.

Risky assets are understandably worried because these are indeed important changes.

…were bond yields to keep on going higher, it would do enough damage to stocks to start hurting growth expectations, in turn supporting bonds. Bond bears would in this way create the source of their own demise, which is not an unusual self correcting mechanism.

In that sense we do not want to exaggerate the prospect of weeks like we have gone through that threaten risk parity trades consistently. At the same time, if inflation pressures and quantitative tightening are not about to change, then the weeks where both equities and bonds sell-off will become a good deal more frequent than we have seen since the Great Financial crisis.

The percent of time when S&P is down and 10y yields are up is roughly 1 in 6 trading weeks, so not all that unusual, but certainly less common than the other scenarios.

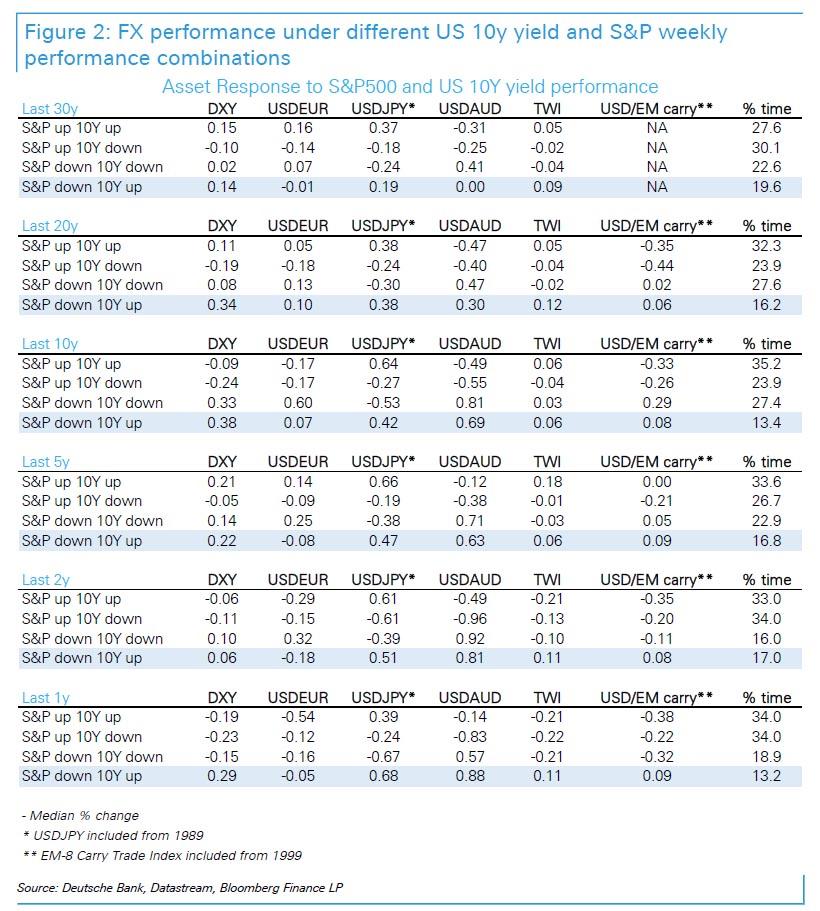

In the environment where 10y yields go up and equities go down, the USD tends to go up sharply versus the AUD at least in the past decade. The USD also goes up substantially versus the JPY. The USD is mixed to near flat versus the EUR (or before the EUR the DEM). This leaves the USD up moderately on a Trade weighted basis. Since 1999, the USD also appreciates (somewhat less than we might expect) versus EM carry – using the Bloomberg EM-8 carry index of cumulative total returns. The USD’s positive response versus EM looks much more substantial when using average weekly gains as distinct from median weekly gains. This suggests that every now and then there are some very large negative EM moves, when US bond prices and stock prices go down, which is not a huge surprise.

…history supports the thesis that when it feels like there is nowhere to hide between poor simultaneous trading conditions in the equity and fixed income markets, the USD and more recently the EUR have been the currencies to shelter in.

With bond and equity prices tumbling in the last week, the FX markets price action conformed remarkably closely to how the USD and other currencies have traded in tough risk parity environments of the past 30 years.

So long as the stock shakeout runs, AUD/USD will mitigate the downside with falls in the currency for local investors invested offshore.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.