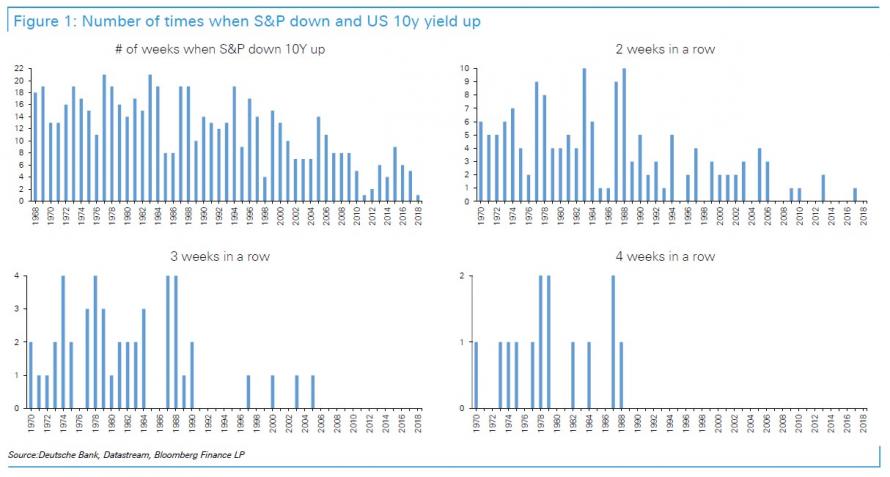

Three weeks of equities down, 10y yields up, has not happened for more than a decade.

Bond and equity prices falling sharply on the week may feel like an unusual environment, because in the last decade, it has become unusual. However, especially as we go back to the 1980s and 1990s it was a more frequent occurrence to see the following causal chain develop: Equities go up, supporting growth with a lag, pushing bond yields up, to the point where higher bond yields eventually pull equities down. In this way the equity – bond causality and correlation shifts, from a positive correlation where equities drive up yields, to a negative correlation as bond yields take the causal lead in pushing equities down.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.