Via Adam Creighton:

The Reserve Bank took a cautious stance yesterday, sitting on its policy hands for the 18th month in a row. After its first board meeting of the year, Philip Lowe, the RBA governor, indicated official rates were unlikely to rise soon.

“Long-term bond yields have risen but are still low. As conditions have improved in the global economy, a number of central banks have withdrawn some monetary stimulus,” Lowe said.

“Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual.”

McKibbin explains how rising expectations of future rates affect activity. “They just sit pat for a few board meetings if they want to see rates rise.”

There was about an 85 per cent chance yesterday of official interest rates increasing to 1.75 per cent before the end of the year.

“The RBA doesn’t want to go on record saying that lower equity prices are justified or not, but the health of the global and local economies should provide some support to equities,” says Capital Economics chief economist Paul Dales.

“Raising interest rates at this point would just make things more difficult for the bank by strengthening the dollar, crimping business investment just as it got going, hurting households when income growth is still low, and it would be tantamount to taking an axe to the housing market rather than the scalpel used by the banking regulator,” he adds.

If the Reserve Bank does try to insulate rates from the expected rise in the US, the Australian dollar is likely to fall further. Historically, Australian interest rates have been higher than in the US.

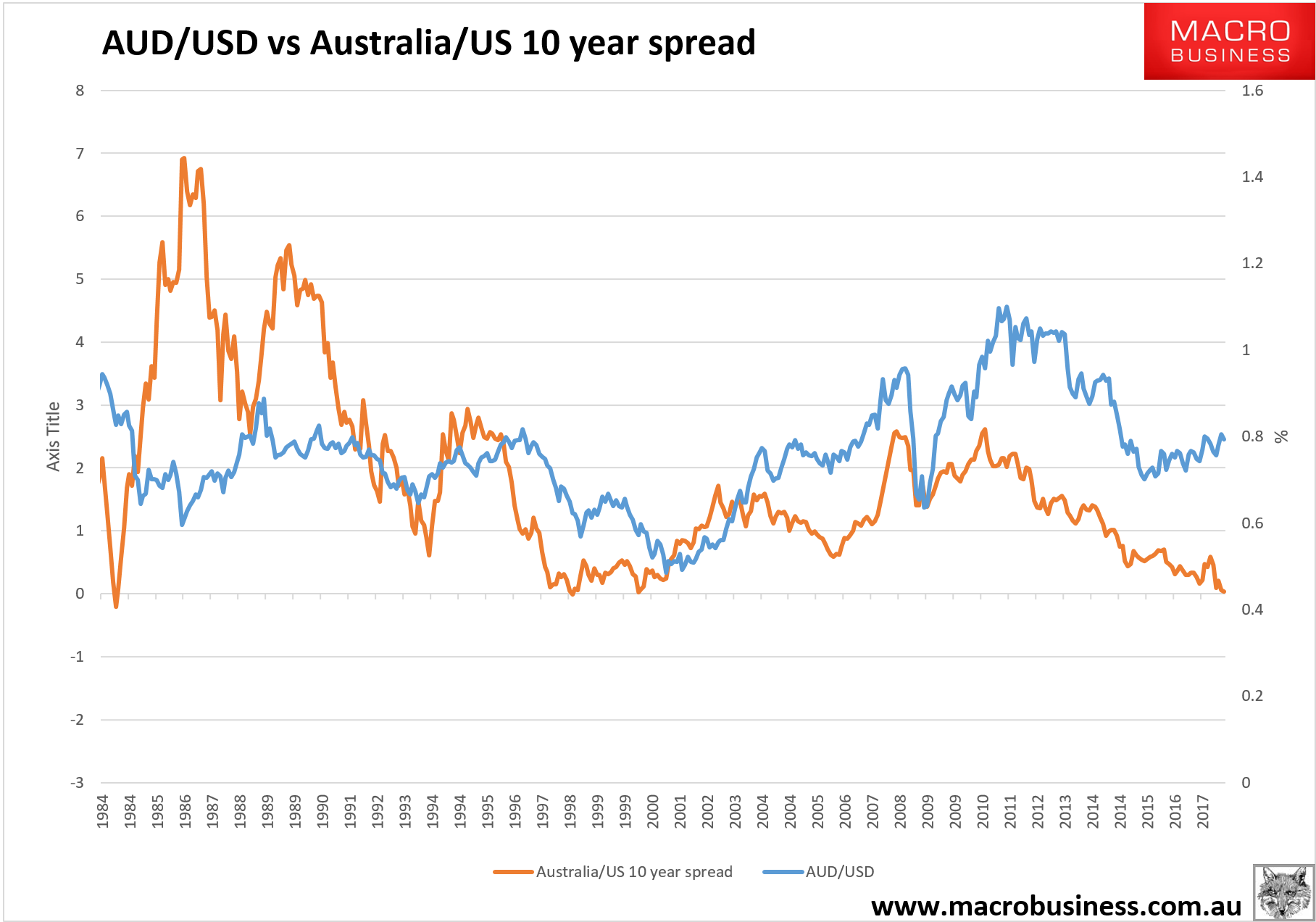

“It is striking the last time the rate difference was this narrow the Australian dollar was struggling to hold above US50c,” says Eslake. Conventional economics hasn’t been much help in predicting exchange rate movements for some years. “You would tend to expect that with further widening of the spread the Australian dollar would start to fall,” noting the gap between the 10-year Australian and US government bond yield had shrunk dramatically. Yesterday the Australian 10-year bond rate was 2.81 per cent, just a 0.04 percentage point higher than the US.

But if the price of iron ore eases our defensive shields might disintegrate. Policymakers like a weaker exchange rate, but it is hard to see anything below US65c being very popular.

Here’s the chart:

Notice how the last two years is the first time since the float that the AUD/USD trend has diverged from the 10 year bond spread. That wedge is the high terms of trade (largely iron ore and coking coal prices).

When they fall two things will happen. The 10 year spread will invert and keep falling. And the AUD/USD will resume its former very strong relationship.

My best guess for the next period of iron ore weakness is Q2 but I expect it to trend down all year as China slows.

————————————–

David Llewellyn-Smith is Chief Strategist at the Macrobusiness Fund which is currently overweight international stocks that will benefit from a falling AUD so he is definitely talking his book!

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.