In 2006, then Treasurer Peter Costello announced that the taper rate by which the Aged Pension is phased-out would be halved from $3 per $1,000 of assets over the threshold to $1.50.

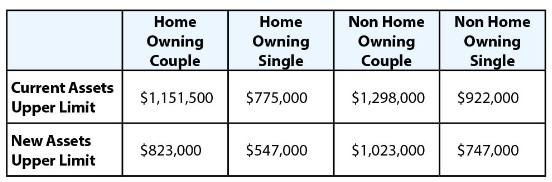

This change greatly relaxed the assets test for the Pension, and led to the ridiculous situation whereby retiree home owning couples with $1.15 million in other assets, and home owning singles with $775,000 of other assets, could still qualify for the part Aged Pension along with the Pensioner Concession Card.

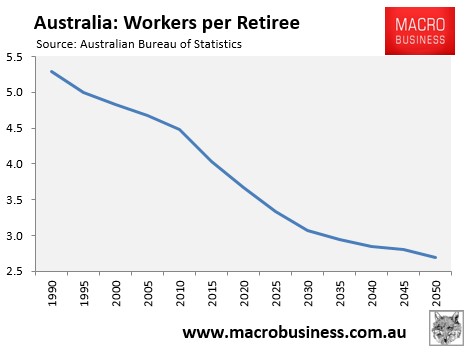

In effect, a large number of wealthy retirees were able to qualify for welfare – an unsustainable and inequitable situation given the rapid ageing of the population and the projected diminishing number of workers available to support retirees (see next chart).

Last January, the Coalition Government’s sensible reforms to the Aged Pension came into effect, which greatly improved the equity and sustainability of the system. As part of this package, the taper rate was reversed back to its pre-2006 level.

While some wealthy retirees would no longer keep receiving the part Aged Pension (but would keep their concession card):

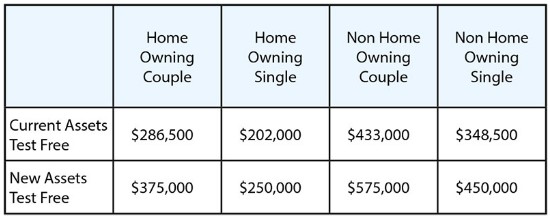

The Government would provide additional funding to pensioners with fewer assets:

The reform package was projected to save the Budget (and younger Australians footing the bill) some $2.4 billion over four years, whilst improving the lot of pensioners without significant assets – i.e. a policy no-brainer.

Amazingly, industry lobbyists continue to wail against the reforms, as illustrated today in The Australian:

It has been a year since stricter asset tests for the age pension came into force…

The Self-Managed Superannuation Fund Association threw a spotlight on the issue yesterday.

In a statement, chief executive John Maroney said it was now apparent that the changes to the means test taper rates and thresholds have had “significantly adverse and presumably unintended consequences”.

He said the steeper taper rate that took effect from January 1 last year is now actively discouraging middle-income wage earners from saving to be self-sufficient in retirement.

Maroney argues that the changes have created a “black hole” for people directly affected by the changes that makes them worse off in terms of income — encouraging them to spend up (or cut back on their savings) to reduce their assets to qualify for the pension. He cites the example of a home-owning couple who have a superannuation balance of between $500,000 and $800,000.

For couples in this situation, he says the taper rate (the rate at which higher assets reduce entitlement for the pension) is the equivalent of about 7.8 per cent a year. With today’s low interest rates, this is well above the amount that a retiree could expect to be receiving from their investment or time deposit…

The couple in question is better off spending their money, reducing their assets to enable them to qualify for the pension, or shifting their assets from financial assets into non-financial assets such as the family home and getting as much of the pension as they can…

Assistant Treasurer Michael Sukkar… that it is not the role of the age pension to support retirees with a higher level of assets to maintain their capital base.

He argues that the steeper taper rate was introduced to encourage people to draw down their private savings more rapidly.

It’s amazing how merely returning the taper rate back to its old level, as well as providing additional funding to pensioners with fewer assets, can be seen as cruel and unfair by the industry.

Clearly, returning the Budget back to surplus is only a priority as long as someone else (i.e. everyone other than wealthy older Australians) pays.

unconventionaleconomist@hotmail.com