Wall Street Journal on a theme dear to our hearts – Chinese growth slowing:

The Business Cycle Is Different This Time—Thank China

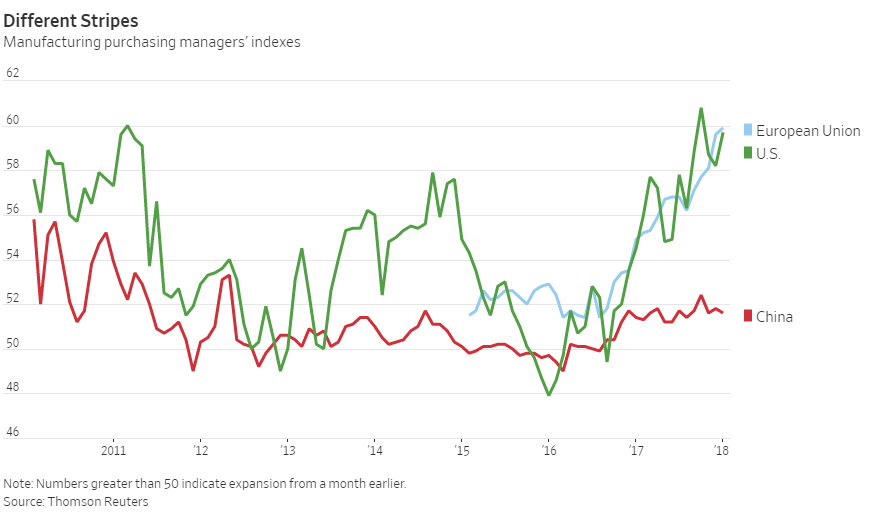

Diverging Chinese and U.S. growth are behind the confusion in global markets right now

Commodities and stocks have started 2018 with a bang. U.S. oil is trading over $60 a barrel for the first time since 2015, and the Dow has breached 25000. Inflation, though, remains in check despite a U.S. expansion in its ninth year. Investors can be forgiven for being both pleased and befuddled: where exactly are we in the business cycle?

Part of the confusion stems from widely employed language about a “simultaneous” uptick in the U.S., Europe, China and Japan. Global economic powerhouses are all growing, sure, but there are nuances. China experienced a steep slowdown in 2015 followed by a rapid rebound in early 2016, but is now cooling. The U.S. has been slowly healing from the carnage of 2009 and—until recently—hasn’t shown much sign of running up against any big constraints in labor or industrial capacity which could choke off growth.

That divergence ought to be broadly positive for developed world equities—but at best neutral for commodities this year.