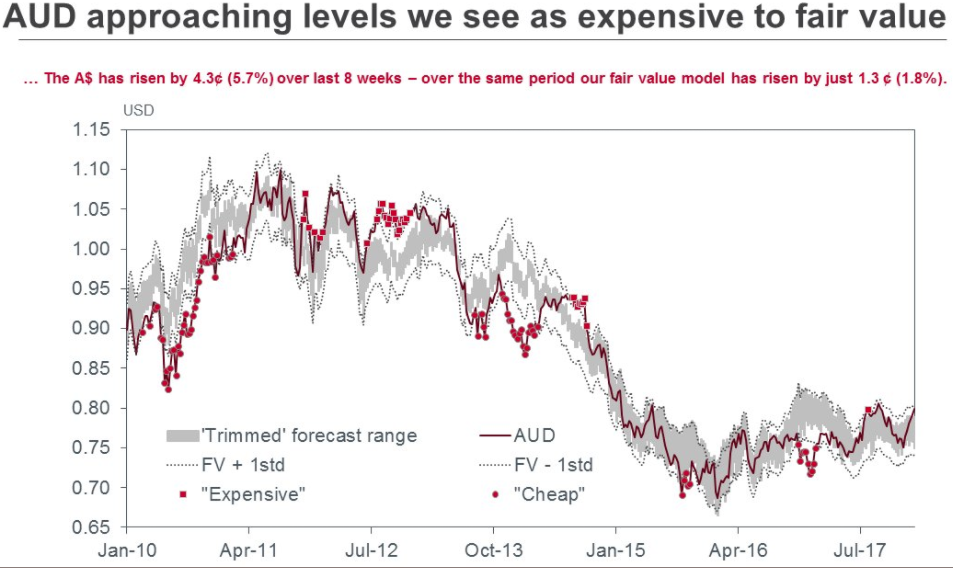

Via Westpac comes the factors in the Australian dollar rise:

Westpac Australian export weighted commodity index is at 1yr highs;

Risk sentiment in global financial markets has also been positive;

AU-US 2yr swap spread is at fresh lows back to December 2000;

Our fair value model framework thus suggests that as much as 70% of the recent rise in the A$ could have been driven by the recent slide in the US$. If history is a guide, that leaves the A$ looking ‘expensive’ at least on the basis of our fair value framework.

Could get more expensive yet given the falling USD though it never spends too long outside the WBC range (of course the range might also rise if iron ore takes off again which I doubt). Such periods of overvaluation have usually been followed by goodly falls.

Advertisement

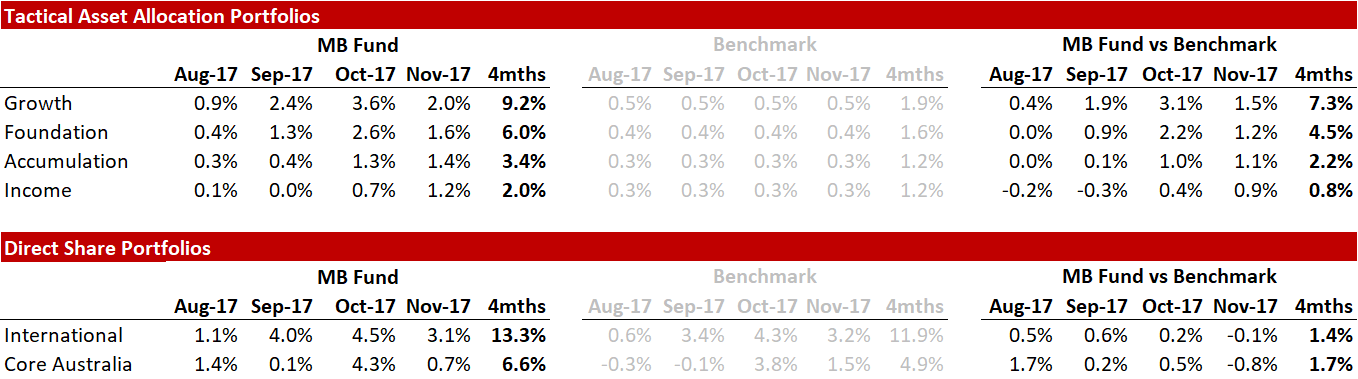

David Llewellyn-Smith is chief strategist at the MB Fund which is currently long international equities that offer superior growth and benefit if the AUD falls so he is definitely talking his book.

Here’s the recent fund performance:

Source: Linear, Factset

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. October monthly returns are currently at 4.9% for international and 4.2% for local shares.

If the themes in this post and the fund interest you then register below and we’ll be in touch:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. The MB Fund is a partnership with Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Source: Linear, Factset

Source: Linear, Factset