There was an interesting Wall Street Journal article yesterday on mobile payments in China – I knew mobile payments were big in China (and that the US is a long way behind on cashless) but I hadn’t realised how stark the difference is:

BEIJING—Soliciting handouts near a grocery store, Zhao Shenji, a slender man with shorn hair, made giving easy for Beijing residents accustomed to relying on their smartphones.

“Recommend using WeChat Pay,” said a placard the beggar displayed.

It was a literal sign of the times. Payment via mobile-phone services such as WeChat is sweeping the country. After gaining a beachhead as a means to buy things online, mobile payments moved on to store purchases and are fast becoming the way many people in China pay for just about everything.

…

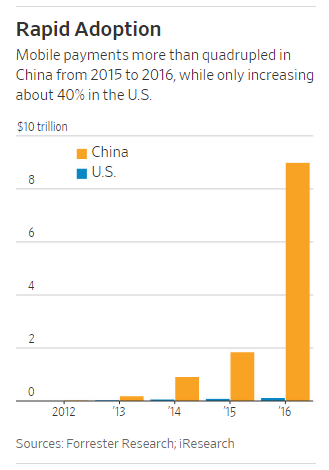

Though the U.S. saw $112 billion of mobile payments in 2016, by a Forrester Research estimate, such payments in China totaled $9 trillion, according to iResearch Consulting Group, a Chinese firm.

For Alibaba and Tencent, the payoff isn’t just the transaction fees they make from merchants, typically 0.6%. It’s also the consumer data collected, which can transform their apps into marketing platforms for an expanding array of services, from bike sharing to travel.

Some of the repercussions of increasing mobile payments are just coming into view. The payments haven’t been required to go through the central bank’s clearing system, making it harder for China’s monetary authorities to follow capital flows and watch for money laundering and fraud. The People’s Bank of China has ordered a new payment-clearing platform that will require nonbank financial firms to give it a clearer view of mobile payments by the summer of 2018.

Consumers also are being offered more pitches for loans, investments and other financial products via smartphone. Short-term consumer credit in China soared 160% in the first eight months of 2017 from a year earlier, according to the central bank. Some analysts think the growing ease of borrowing is part of the reason.

There are a lot of interesting angles on this. I have some initial thoughts and I’m interested in reader views… bomb away in the comments:

Why so big in China? Apple and Android payment systems are in many countries but they never took off like these mobile payments have in China

Chinese GDP per capita is around USD15k per person. This is suggesting USD6.5 is being spent per person on mobile payments. This seems high. Maybe the numbers are wrong, or they are counting “both sides” of the transaction. Need to look more at this.

Is it a precursor to a similar explosion elsewhere or are there China-specific issues?

Some of this is ease of use – you can easily send “strangers” instant payments. You don’t need a card reader, you can send phone to phone which makes it much easier than requiring a merchant to have a card reader

Some of this is “regulatory arbitrage”, getting around the banks. Seems like it is soon to come under banking scrutiny in China – maybe there was a “one-off” window to do this in China before the regulators cracked down

Some of the growth may be due to restrictions that China put on Mastercard/Visa (but that doesn’t explain the size)

China never big on credit cards and so they might be “leapfrogging” the credit card era

WeChat is ubiquitous in China – most of the rest of the world doesn’t have a common platform so it might be much harder

At first blush, seems like a big threat for Mastercard and Visa

Is there a technology that could cause the US to do the same? The US is a dinosaur in terms of the widespread use of cheques still – could mobile payments finally kill the personal cheque? I’m guessing not, but something to watch

Advertisement

Damien Klassen is Head of Investments at the Macrobusiness Fund, which is powered by Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.