A relatively modest start to the week here in Asia with most stock markets having small gains or pauses in their large rallies, embiggened by a weaker USD even as the Trump Presidency tries to jawbone it three ways to Friday. Earnings season has begun in Australia, which has given the local bourse a lift, while industrial commodities also gained.

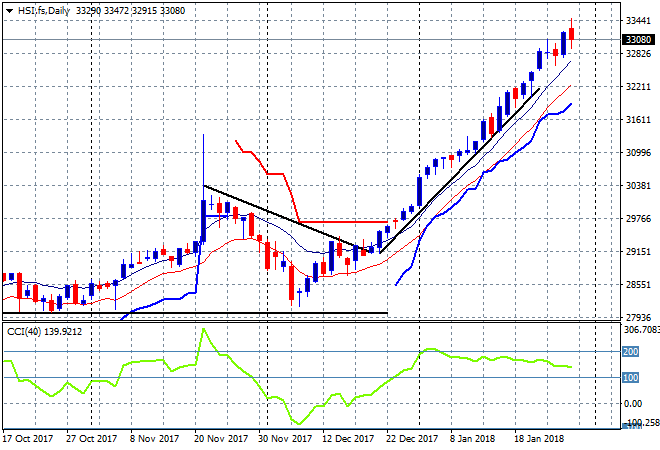

In mainland China the Shanghai Composite is fighting the trend after making great inroads previously, closing 0.5% lower to 3540 points. The Hang Seng Index is also in a pause phase, down 0.1% to finish slightly above the 33,000 point level in a welcome consolidation in this too-perfect uptrend:

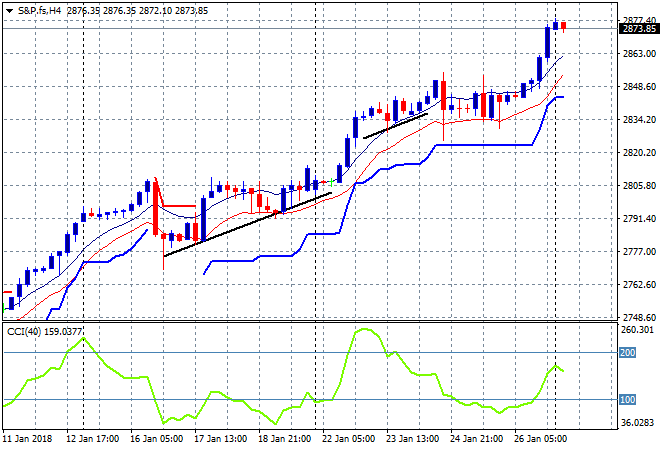

S&P futures are elevated, gapping up to slightly exceed the Friday night exuberant highs. Going into Trump’s first State of the Union speech (bigly) tomorrow night plus more earnings to come, its going to be another interesting week!

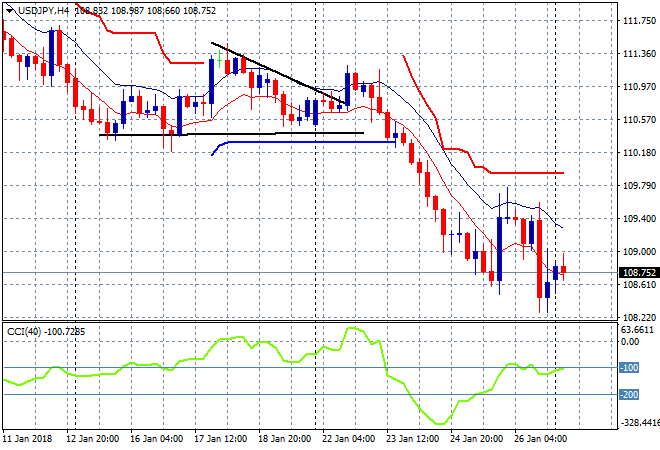

Japanese stocks have done remarkably well given the gains in Yen, with the Nikkei 225 up 0.2% to 23666 points still hanging on. The USDJPY pair gapped up slightly on the weekend news, still dicing with the 109 handle now with barely any upside support, so 108 proper looks set to be the next target:

The ASX200 did the best in the region which is a surprise, closing 0.4% higher to 6075 points. Fairfax had a good day, up nearly 6% while the banks did most of the heavy lifting as the iron ore triumvarate retreated.

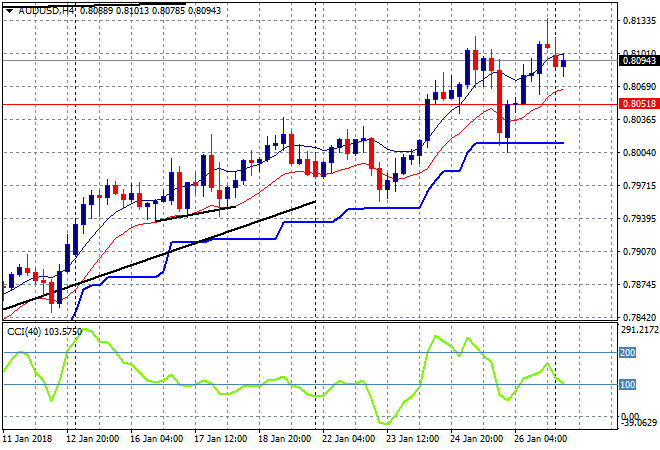

The Aussie dollar is still firm here just below 81 cents versus the USD, having gapped down slightly after being overextended in the last session on Friday night. Support at 80.50 must hold here for another step up:

The economic calendar starts the week with a key ingredient to US GDP, namely personal consumption expenditure (PCE) for December and the Dallas Fed manufacturing activity for January.