Dick Smith Fair Go (DSFG) has produced a new 31-page easy-to-read document, entitled “Australia’s Debt: an Honest Debate”, examining Australia’s debt position and whether or not it poses a problem for the Australian economy. The report concludes that it is not public debt that is the problem, but rather Australia’s world-leading private debt load, which is concentrated in our expensive homes.

Below are the key extracts from the DSFG report regarding private debt:

Australia’s government debt does need to be reduced, however it appears to be far from the danger zone and far less than many other developed countries.

Australia’s bigger problem is private debt.

The theory goes that when the private sector takes on debt, there’s nothing to worry about because, motivated by the profit incentive, the private sector will always make choices that are ultimately productive.

This may be true in the case of big operators like the mining industry; they borrow billions and the profits that result from all this borrowing more than takes care of the debt burden.

But that isn’t always the case with smaller businesses, investors or, especially, individuals.

When it comes to household debt – which includes people’s mortgages, credit cards, overdrafts, and personal loans – Australian households are the second most indebted in the world (after Switzerland) when measured against the size of the economy, or Gross Domestic Product (GDP).

In 1990, overall household debt accounted for about 70% of household disposable income. The Reserve Bank’s data on household debt shows that it has since risen to 194% of annual household disposable income in 2017. This ratio is the highest it has ever been since the commencement of official data (dating back to 1988) and almost 50% higher than it was in the US ahead of the sub-prime mortgage crash of 2008 that caused the Global Financial Crisis.

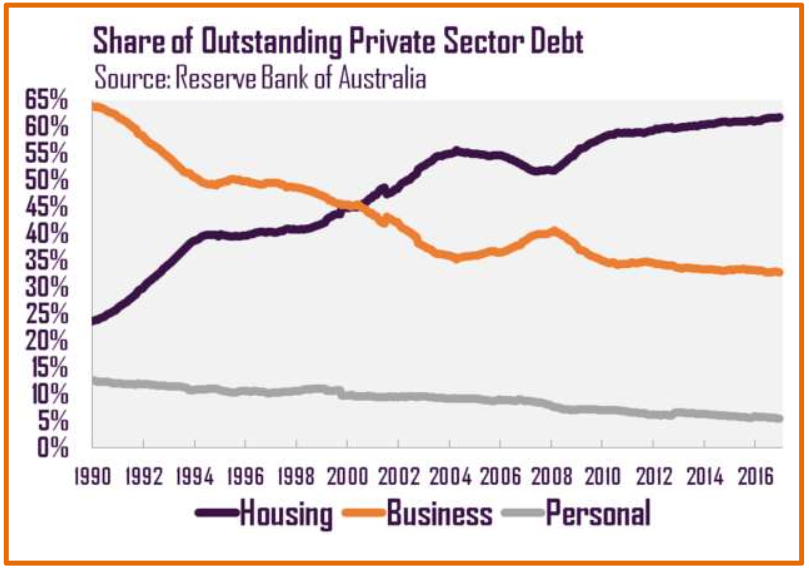

Like America, Australia’s private debt levels are mostly because of home loans. Ever since the stock market collapse in 1987, when many business got into financial difficulties, Australian banks have shifted their focus to lending to invest in property and pumped money into home loans.

This was turbocharged after the Global Financial Crisis when interest rates were driven to historical lows in an attempt to spur ‘economic growth’ by making it very cheap for people to borrow to invest.

In fact, the share of total lending going to housing has increased from roughly 25% in 1990 to more than 60% currently, which has come at the expense of productive business lending.

The more money the banks pumped in, the higher real estate prices rose to meet the increased spending power of buyers. The higher the prices, the more that was needed in loans. This is a business model that some would call a type of Ponzi scheme – which is illegal in Australia.

Aided and abetted by negative gearing and the discount on the capital gains tax, it was very profitable for all involved – for more information about this see our other publication: ‘The Aussie Housing Affordability Crisis: An Honest Debate’.

As a result, we now have some of the most inflated house prices in the world and Australian home loan borrowers are among the world’s most indebted, with an eye watering $1.7 trillion owing on their houses.

There are two big hidden threats to our whole economy lurking behind all this.

Unproductive Debt, offshore borrowings, and Interest Rates

Substantial amounts of the money that Australians are borrowing from our big banks to buy these houses were originally borrowed by the big banks from overseas, which contributes to our national debt.

Selling the same house half a dozen times produces very little in terms of expanding the economy, or creating any new jobs.

More than 90% of this lending for property investment was for existing houses, not even to build new ones that would help boost supply.

Borrowing money from overseas and investing in unproductive assets that don’t help us to pay it back, like housing, sounds like a recipe to damage the economy to me.

That is one reason why politicians are being disingenuous when they crow about the government debt, but ignore the level of household debt, which would appear to be a far bigger threat to our economy.

The reality is that Australia’s government debt and private (mainly housing) debt are inter-related.

Most of Australia’s $1 trillion dollars in net foreign debt has been borrowed through the banking system and used to increase home lending.

As at June 2017, the banking sector had borrowed some $850 billion from offshore, equating to 49% of Australia’s GDP.

Australia’s banks would never have experienced anywhere near the same degree of asset (loan) growth without this tapping of offshore funding markets. Accordingly, the total value of Australian home loan debt would never have grown so strongly, and Australian house prices would be materially lower as a result.

Australia’s banking system is also now so large that it is considered ‘too-big-to-fail’ by the ratings agencies, which means that the federal government (read taxpayers) would be required to bail the banks out in the event that there was a banking crisis. Accordingly, the major banks’ credit ratings are now inextricably linked to Australia’s sovereign AAA credit-rating.

The higher the rating, the safer bet you’re seen to be by lenders who will be willing to extendlarger amounts at a cheaper rate of interest.

The key risk is that the banking system’s ability to continue borrowing from offshore rests with foreigners’ willingness to continue extending credit to them. This willingness will be tested in the event that Australia’s AAA sovereign credit rating is downgraded (automatically downgrading the banks’ credit ratings), if there is another global shock, or a sharp deterioration in the Australian economy (raising Australia’s riskiness as a borrower).

While Australia’s government debt is currently low, the Federal Budget is hostage to the banks’ offshore borrowing excess as it cannot borrow to spend on infrastructure or other initiatives for fear that Australia will lose its AAA credit rating, automatically downgrading the banks’ credit ratings and causing an unravelling of the private debt bubble created by the banks.

Indeed, credit ratings agency, Moody’s, last year noted that “A key issue for the Australian sovereign and the country’s banking sector is their reliance on overseas funding… This means a relatively greater vulnerability to ‘event risk’ than most other AAA – rated sovereigns”.

In a similar vein, the Murray Financial System Inquiry warned that “Australia’s banking system is highly concentrated, with the four major banks using broadly similar business models and having large offshore funding exposures… Australia is susceptible to the dislocation of international funding markets or a sudden change in international sentiment towards Australia, which would reduce access to, and increase the cost of, foreign funding [and] a severe disruption via one of these channels would have broad economic and financial consequences for Australia”.

Domestically, the build -up in private debt has been sustainable while interest rates have been at record lows.

However, loans run for 25 to 30 years. Anyone who thinks rates will stay at record lows for that length of time has their head in the sand.

There are plenty of people who’ve bought into the frenzy, borrowed to the hilt, and given themselves little room to move in the event of a rise in interest rates.

In the 1990s when mortgage interest rates peaked at 17%, lots of typical Australians lost every thing. It could happen again, and interest rates don’t need to go anywhere near as high to start causing financial strife.

Work by the Grattan Institute shows that if interest rates went up just 2 percentage points, stress levels would be the highest on record but for that 1990s 17% squeeze.

If this were to happen while wages growth remains as flat as it’s been, borrowers might not be able to afford their loan repayments. When this happens en-mass it puts our banks in dire straits.

Higher loan costs would lead to less spending, which would affect employment rates, hit the government’s budget, and plunge us into a recession.

The Link Between Population Growth and Debt:

There is one final aspect of Australia’s debt debate that is rarely discussed and not widely understood: the link between the federal government’s 200,000 strong ‘Big Australia’ immigration program and private debt.

The lion’s share of Australia’s export revenue comes from commodities and from Western Australia and Queensland. But the majority of Australia’s imports and indeed private debt flows to our biggest states (and cities), New South Wales (Sydney) and Victoria (Melbourne). Sydney and Melbourne also happen to be the key magnets for migrants.

Increasing the number of people via mass immigration does not materially boost Australia’s exports but does significantly increase imports (think flat screen TVs, imported cars, etc). These imports must be paid for – either by accumulating foreign debt, or by selling -off the nation’s assets. We’ve been doing both.

So basically high immigration is affecting the trade balance via more people coming in each year (mostly to Sydney and Melbourne) because of the additional imports purchased, as well as driving Australia’s external vulnerability via the build-up in non-productive private debt.

Conclusion…

While it may be more politically astute to focus on the government debt (because they can more easily blame their opponents for it), it will be better for the country if the Australian people, the voters, are informed that it’s private and household debt that is most likely going to cause major problems in the future and that our record high immigration-fuelled population growth is making the problem worse.

Advertisement

MB was consulted on this paper and provided extensive input regarding Australia’s private debt.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.