Via the excellent Paul Dales at the AFR:

…while GDP growth may rise from about 2.2 per cent last year to 2.5 per cent this year, it will fall short of the consensus forecast of almost 3 per cent and leave Australia growing at much the same pace as the average OECD economy.

This may generate four surprises for investors. First, official interest rates in Australia will be lower than rates in America for the first time since 2001. This loss of Australia’s official interest rate premium is widely expected. But the extent of the shift will probably be bigger than most anticipate.

…Second, 10-year government bond yields in Australia may soon be lower than 10-year yields in the US. The consensus view is that 10-year yields in the two economies will rise in lockstep, resulting in Australia hanging on to its yield premium. But late last year two-year yields in the US rose above those in Australia. And the extent of the divergence in official interest rates we expect suggests that 10-year yields in the US will rise by more than in Australia.

…Third, this erosion of Australia’s yield premium will surely contribute to a weaker Australian dollar. This hasn’t already happened because the dollar takes its cue from commodity prices as much as interest rate differentials, and their strength has driven it up to $US0.80. But if my yield forecasts are correct and if an easing in economic growth in China prompts the iron ore price to fall in line with my forecast, from US$77 per tonne now to US$55, then the dollar may slip to $US0.70 this year.

The good news is that this relative underperformance may not last long. Due to its more favourable demographics and higher rates of net migration, Australia may grow by 2.75-3 per cent a year over the next decade. In contrast, America’s potential growth rate may be 1.5 per cent and the euro-zone’s may be about 1 per cent. So it is only a matter of time before Australia is back at the top of the ladder.

Not while house prices fall and they will do so unless household leverage rises. Haven’t regulators forsworn that?

David Llewellyn-Smith is chief strategist at the MB Fund which is currently long international equities that offer superior growth and upside potential if the AUD falls so he is definitely talking his book.

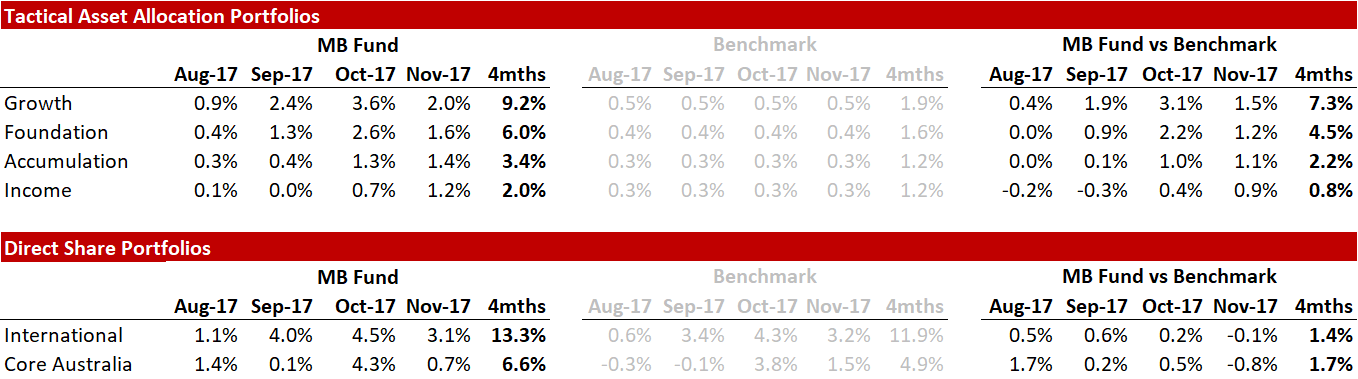

Here’s the recent fund performance:

Source: Linear, Factset

Source: Linear, FactsetThe returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. October monthly returns are currently at 4.9% for international and 4.2% for local shares.

If the themes in this post and the fund interest you then register below and we’ll be in touch:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. The MB Fund is a partnership with Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.