DXY is trying to find traction but without much success yet:

AUD remains hot against DMs:

Less so against EMs:

Advertisement

Gold is also sniffing around for DXY strength:

Oil was firm:

Base metals too:

Advertisement

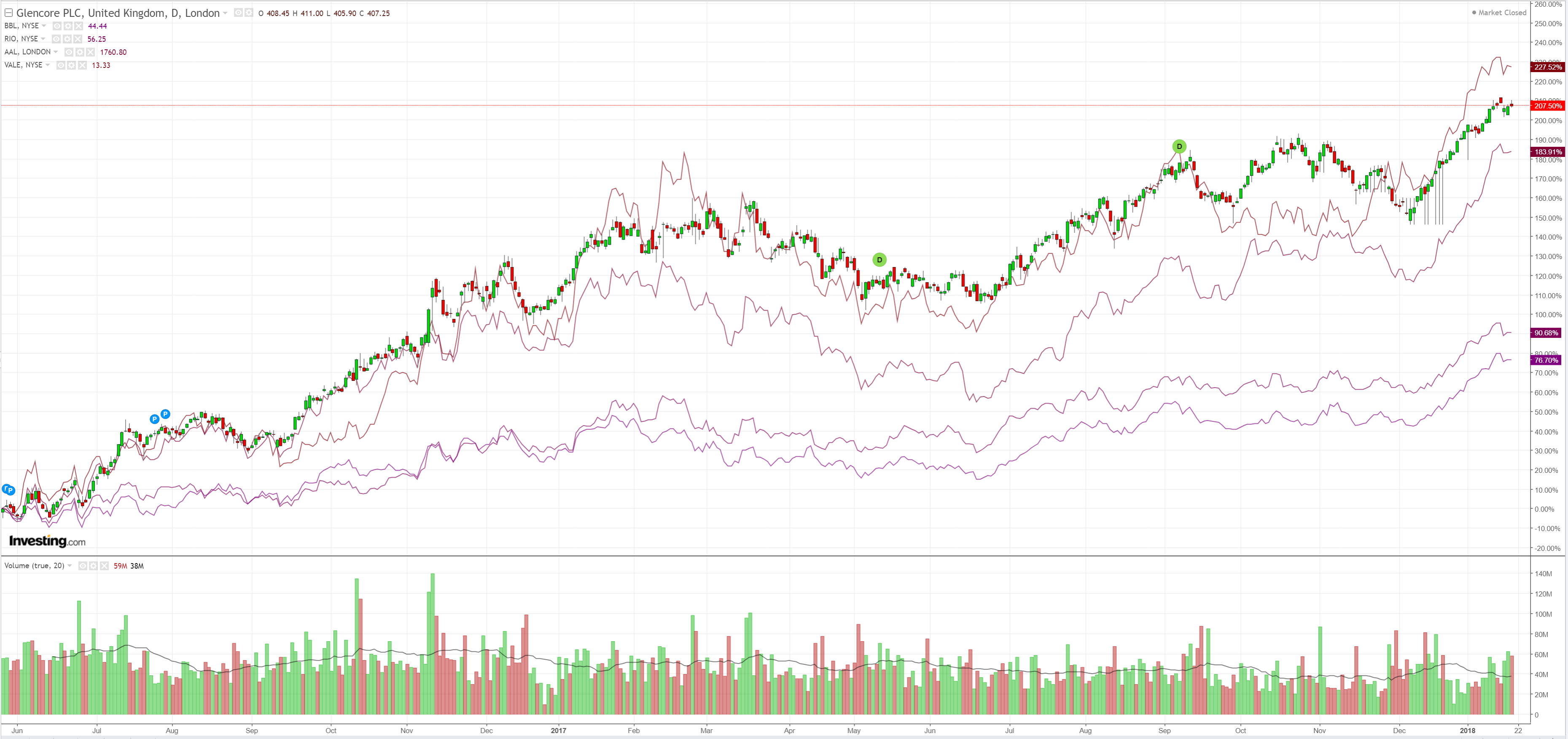

Big miners were soft:

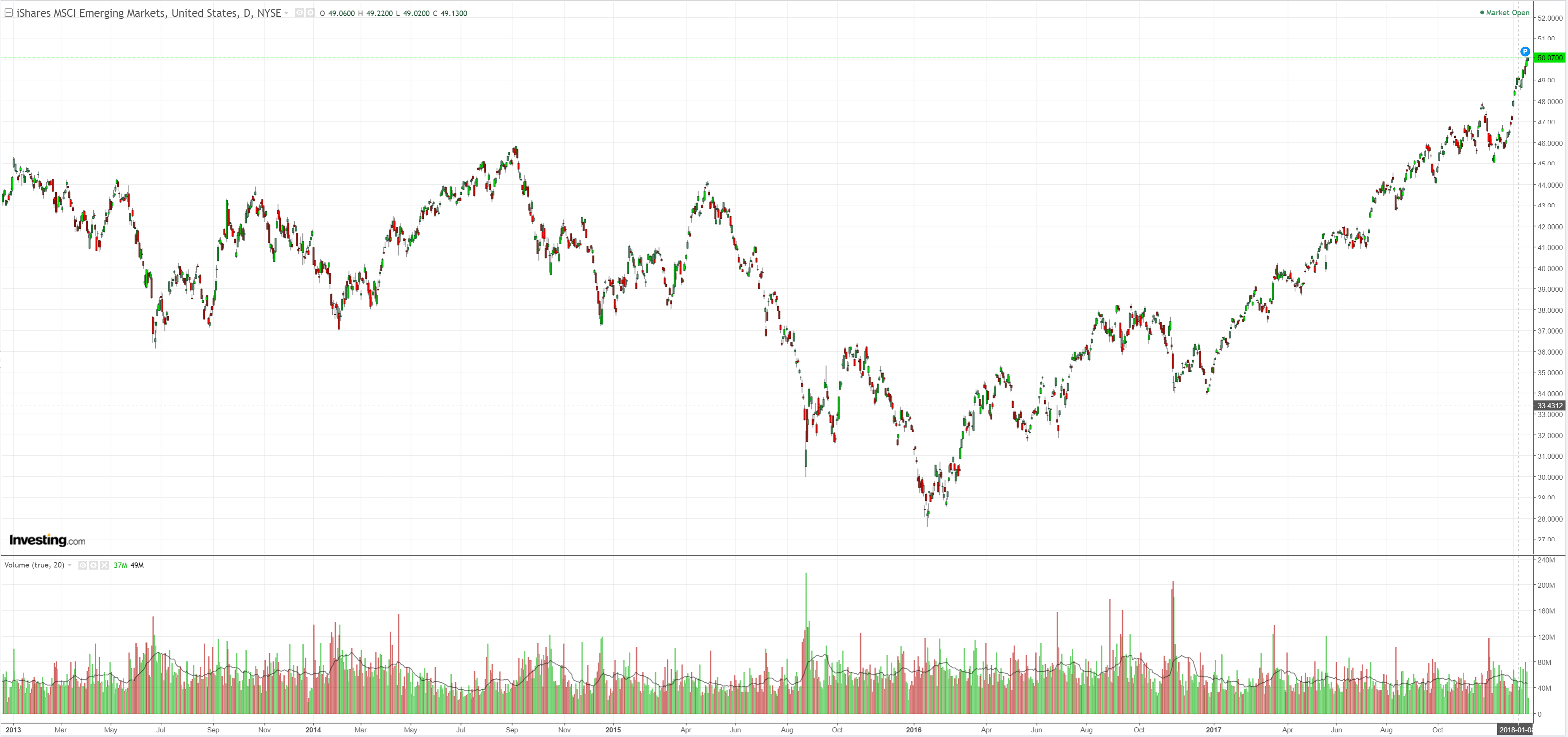

EM stocks weren’t:

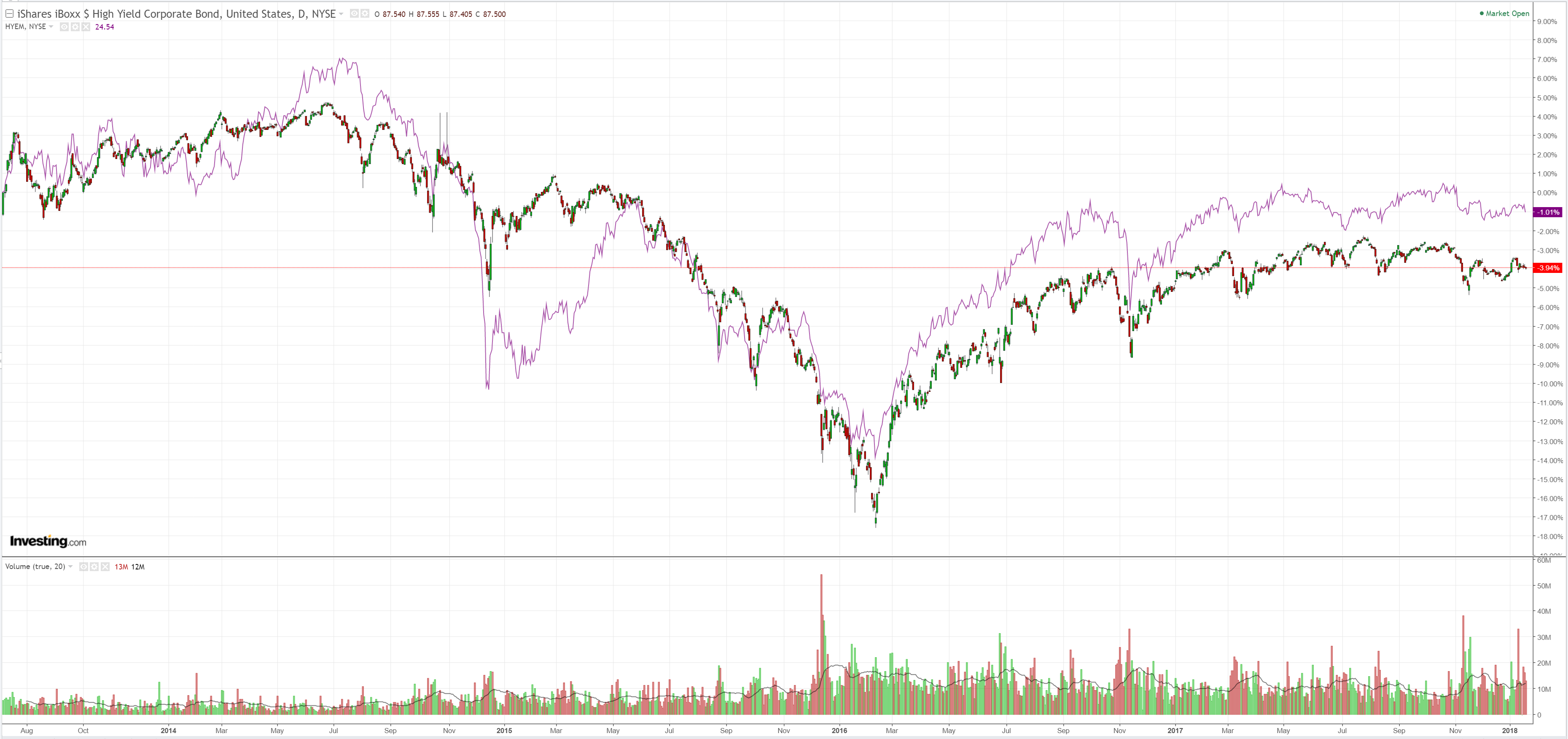

Junk fell:

Advertisement

US yields rose and the curve steepened:

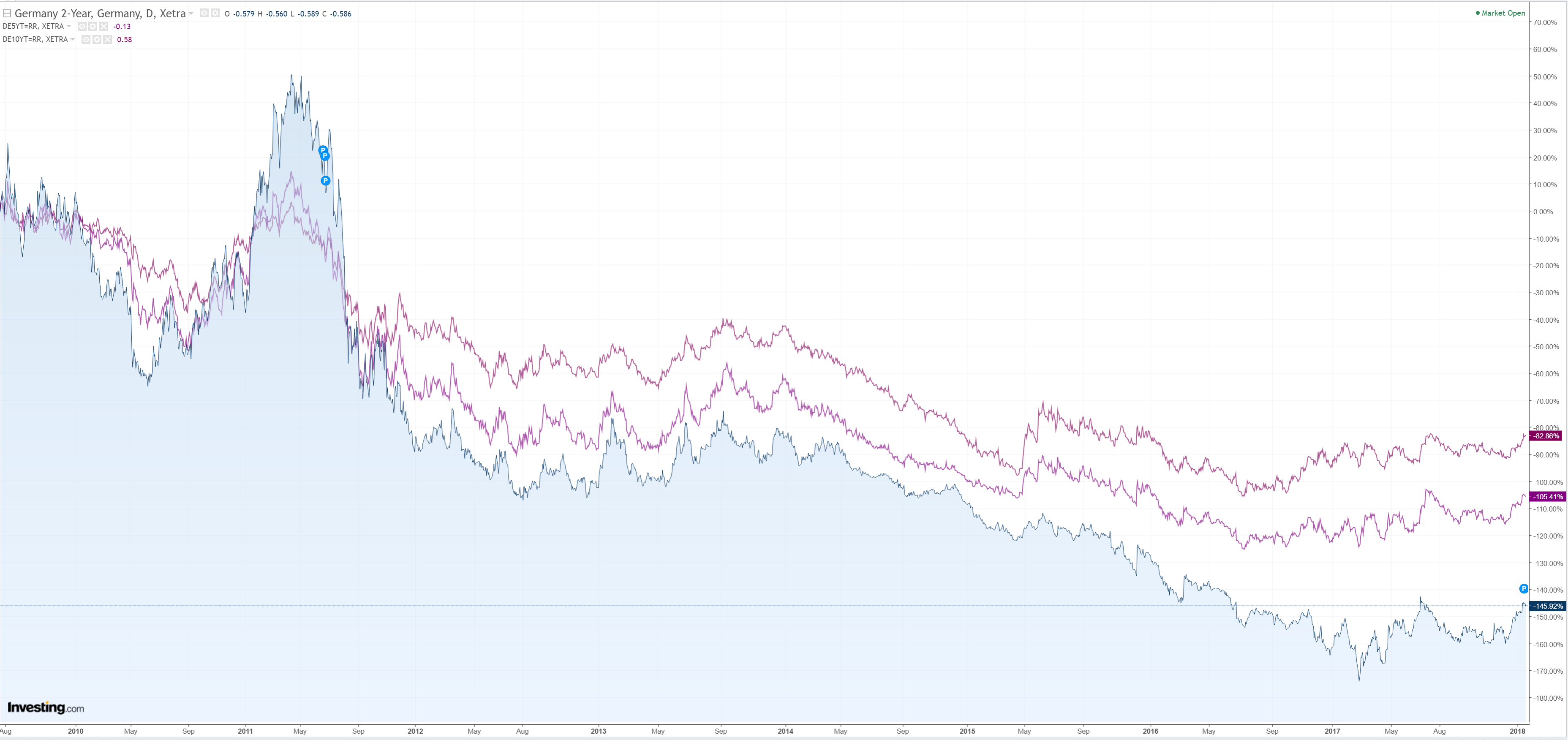

Bunds are stuck still:

Stocks paused:

Advertisement

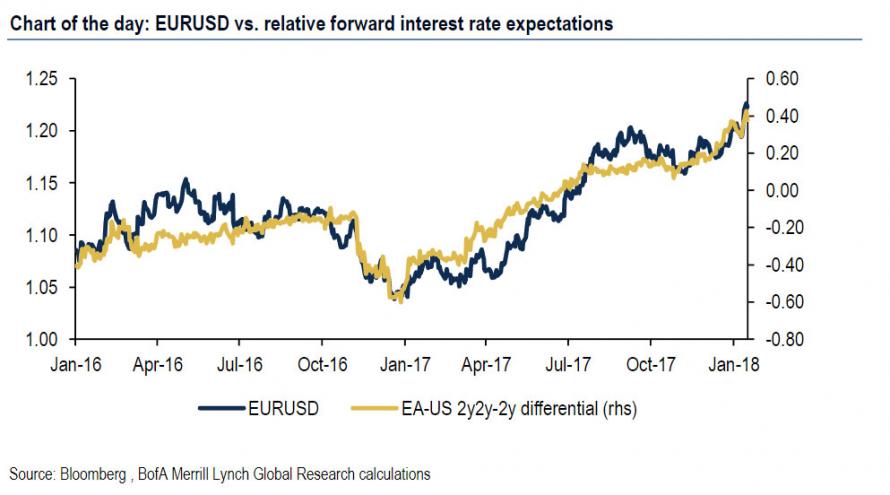

As noted many times, the strong AUD is really a strong EUR story. More on that today from BofAML:

Pressure on the dollar has intensified in the opening weeks of the year despite a supportive macro backdrop. US data had had a strong run, fiscal stimulus is expected to provide further tailwinds to the already-solid growth outlook this year and the Fed continues to tighten. Yet the synchronized global recovery is focusing market attention on other major central banks. As we have argued before, the USD traditionally benefits from first-mover advantage as the Fed leads other central banks into a global tightening cycle. That was the primary driver of dollar appreciation in 2014-15. However, as other G10 central banks follow the Fed’s lead, the USD has been faltering despite ongoing tightening. This is because interest-rate expectations outside of the US have undergone a profound shift. With respect to EURUSD specifically, relative forward interest-rate spreads explain the sustained rise in the exchange rate since early 2017, though upside looks limited for now.

The fundamental link between global central bank repricing and USD-based exchange rates (emphasis: EURUSD) cannot be seen through the traditional lens of spot interest rate differentials, which have broadly continued to move in a direction favorable for the dollar. Indeed, the US two-year swap rate has risen a full 65bp from levels prevailing in early September (for reference, only the CAD 2y rate rose by more).

FX markets are in a regime defined by interest rate expectations.

So while the EUR 2y swap rate has increased by a mere 8bp over this period, the EUR 2y2y-2y forward spread has steepened by nearly 30bp, most of which since early December. Conversely, the US 2y2y-2y forward spread has remained essentially unchanged, if not marginally flatter, reflecting expectations of a reduced pace of Fed tightening ahead, potentially representing entrenched beliefs regarding the maturity of the US economic cycle.

Our Chart of the day: EURUSD vs. relative forward interest rate expectations shows EURUSD plotted alongside the EUR-USD 2y2y-2y forward spread differential, which measures the amount by which the market expects the EUR-USD 2y spot differential to move over the next two years. We think this is a convincing framework to assess EURUSD from the standpoint of monetary policy divergence as it focuses on expectations. Over the last year, the shift in this differential has been large at about +100bp, roughly coincident with the shifts in relative EUR-USD growth during this cycle. Specifically, the market went from pricing a 60bp decline in EUR-USD 2y rate differential over a two-year horizon to presently pricing in a 40bp rise (hence the 100bp delta). EURUSD has tracked the 2y forward curve differential closely, with daily changes in the latter explaining nearly 30% of changes in the former and justifying the 15% EURUSD rally since early 2017.

While the October ECB meeting had provided a sense of medium term stability for ECB policy, comments from Coeure on 21 November questioning the open-endedness of QE kick-started a repricing of EUR front-end rates. In our view, it was precisely the open ended nature of QE, and the ECB’s ambiguity around the program’s end date, that had, up to then, acted as an anchor for short term rates, the two being linked by the ECB’s commitment to keeping rates at their current levels “well past” the end of net asset purchases, which the market had been interpreting as a six-month period.

Mid-December saw an extension of the front-end selloff as the December ECB meeting provided little additional information. However, it was the release of that meeting’s minutes last week that triggered the most significant moves. More specifically, reference to the fact that a “gradual shift” in forward guidance may be warranted by early 2018 appeared to catch the market off guard. The result was a sharp move in rates, driven by 5s, but also affecting the very front end. Specifically, the market now prices in a 70% chance of a 10bp hike in the Depo rate as early as December 2018, and Eonia forwards imply the Depo rate would be brought back to zero by December2019.

The change in tone in the December ECB minutes has admittedly come earlier than we had anticipated. We expected the shift in emphasis in forward guidance from QE toward policy rates to provide support for EURUSD in the second half of the year.

… historical correlations that have driven the EUR have been distorted by the ECB QE-wedge. A return to a conventional policy setting offers the prospect of a reversion back to these historical correlations which broke down in 2015. Moreover, the impact is likely to extend beyond the EUR, specifically, and to currencies whose central banks have implicitly pegged their own policy to the ECB.

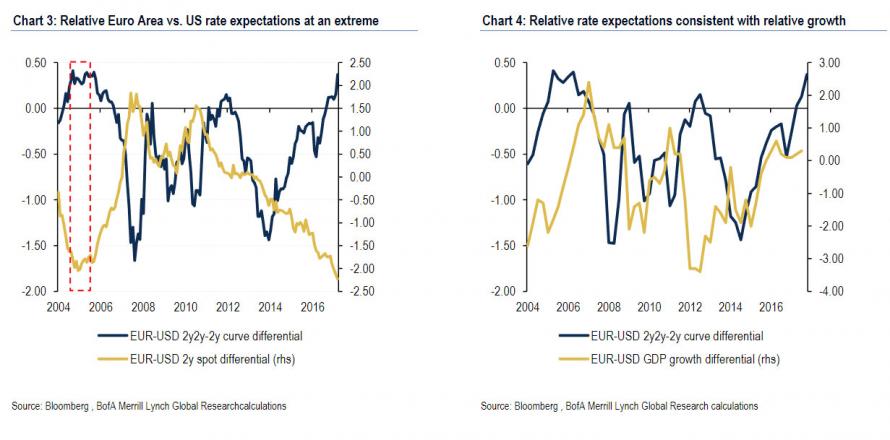

The EUR-USD 2y2y-2y curve differential is now at the highest since the global financial crisis and is approaching 2005-06 extremes, a period in which it reached +50bp (Chart 3). We think that the 2005 analog is instructive regarding the empirical upper bound on relative 2y2y-2y rate expectations. Assuming the market retests the +50bp level (another 10bp from here), we think this should translate to only modest (roughly 2%) higher EURUSD, ceteris paribus. This means we are approaching limits to long EURUSD predicated on ECB normalization expectations.

From a narrow standpoint of relative monetary policy, a sustained EURUSD move above 1.25 probably requires spot interest rate differentials begin to move higher, as they ultimately did in 2H06, roughly two years after the Fed initiated its first interest rate hike and after a lengthy (one year) bottoming process. Incidentally, this was driven by a sharp (-3%) decline in US inflation, which we think is highly unlikely anytime soon. It is also worth noting that back in 2005, unlike now, the EUR-USD growth differential was highly negative at about -2%. It ended up rebounding strongly over subsequent years, supporting a sustained rise in EURUSD to 2008 highs (Chart 4). At present, however, this growth differential has already surged higher into positive territory (relatively rare historically). Note that our current economic forecasts point to a reversal-not an acceleration-of the current EUR growth advantage.

A simple comparison to the US at this point in 2014 (10 months before the end of QE) suggests upside potential could be 50-100bp over the next two years (Chart 5), even as rate expectations (using 2y2y-2y) begin to soften (Chart 6).

Obviously, conditions in the Euro Area are different to those of the US back in 2014, but the context may be helpful. The more relevant question is what happens to the EUR-USD spot interest rate differential, because this will at some point over the next one to two years re-emerge as the relevant monetary policy variable for EURUSD, as the expectations channel wanes in importance. On this subject, we think that upside in USD 2y rates could well match, and probably exceed, that of EUR 2y rates, particularly over the near term.

Very nice work that. To wit, from Karen Moley today:

Advertisement

Already top European and Japanese officials have run the risk of antagonising the Trump administration by voicing their displeasure as the greenback brushes against three-year lows.

…This week, the deputy head of the European Central Bank, Vitor Constancio, voiced his concerns over the euro’s sharp appreciation against the US dollar.

“I am concerned about sudden movements [in the euro] which don’t reflect changes in fundamentals,” he said in an Italian newspaper interview.

Japanese finance minister, Taro Aso, joined in the “jawboning”. He said he didn’t see any problems with the yen hovering at the level of ¥110.80 to the US dollar, but that rapid currency moves would be a problem.

…some top analysts believe that markets are over-estimating the speed with which both the ECB and the Bank of Japan will withdraw monetary stimulus.

They argue that traders are paying undue attention to the comments of ECB board members – such as Bundesbank chief Jens Weidmann – who want the central bank to set a clear date for ending its bond buying program, and ignoring the fact that most ECB board members are in favour of a very cautious withdrawal of monetary stimulus.

And that markets are simply ignoring Bank of Japan chief Haruhiko Kuroda, who has emphasised that weak inflation means that the central bank will continue to run an ultra-loose monetary policy for a long time.

A few points to add:

as stock markets are clearly indicating, the Eurozone area is more sensitive to currency movements that the US;

as China slows into the year it will dent German growth more than US and keep inflation in check more generally.

The rebalancing of rate expectations we’ve seen was fair enough but if it runs much further it’ll trigger its own demise. Ditto the Australian dollar.

Advertisement

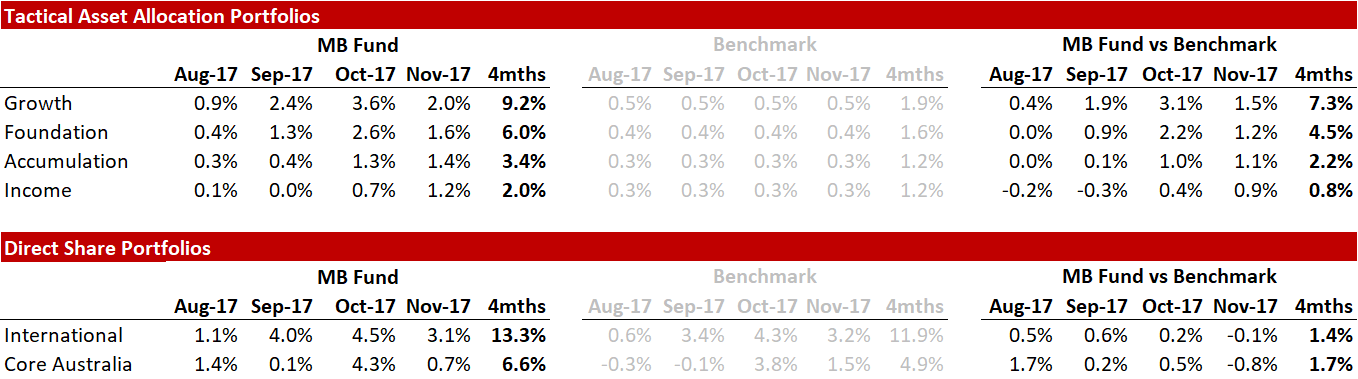

David Llewellyn-Smith is chief strategist at the MB Fund which is currently long international equities that offer superior growth so he is definitely talking his book.

Here’s the recent fund performance:

Source: Linear, Factset

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. October monthly returns are currently at 4.9% for international and 4.2% for local shares.

Advertisement

If the themes in this post and the fund interest you then register below and we’ll be in touch:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. The MB Fund is a partnership with Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Source: Linear, Factset

Source: Linear, Factset