US markets continued grinding higher overnight, most of the news was about the tax cuts.

Ray Dalio (who runs Bridgewater, one of the world’s largest macro funds) posted his thoughts on the tax cuts – largely echoing my thoughts from yesterday:

When we look at the tax plan holistically, it looks to me like it’s a short-term minor boost to the economy that will have some minor positive longer-term impacts, but by and large it doesn’t deal with the impediments that are holding back investment and productivity in the US economy, and it won’t have any notable effect on our biggest economic, social, and political issue, which is the conditions of the bottom 60% and the growing disparity with the top 40% (especially the growing disparity between the bottom 90% and the top 10%).

In the short term, the tax law changes and regulatory reductions will provide a very modest one-time boost to after-tax incomes that will be stimulative. How “good” the tax law changes are depends on one’s own perspective because some things will benefit and hurt some people more than others—but, net, it won’t be big. For example, it will typically move after-tax incomes by about 0.5% in total, which will be made up for by a nearly comparable increase in the budget deficit (which doesn’t come at no cost).

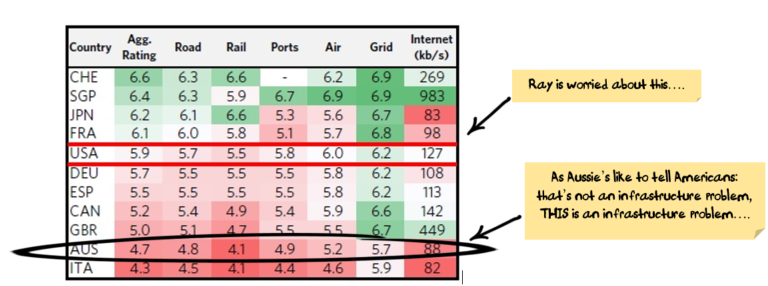

Ray then followed my line of thought on infrastructure, pointing out how this would be a much more effective stimulus than tax cuts. He showed the below chart (comments are mine) from the World Economic Forum:

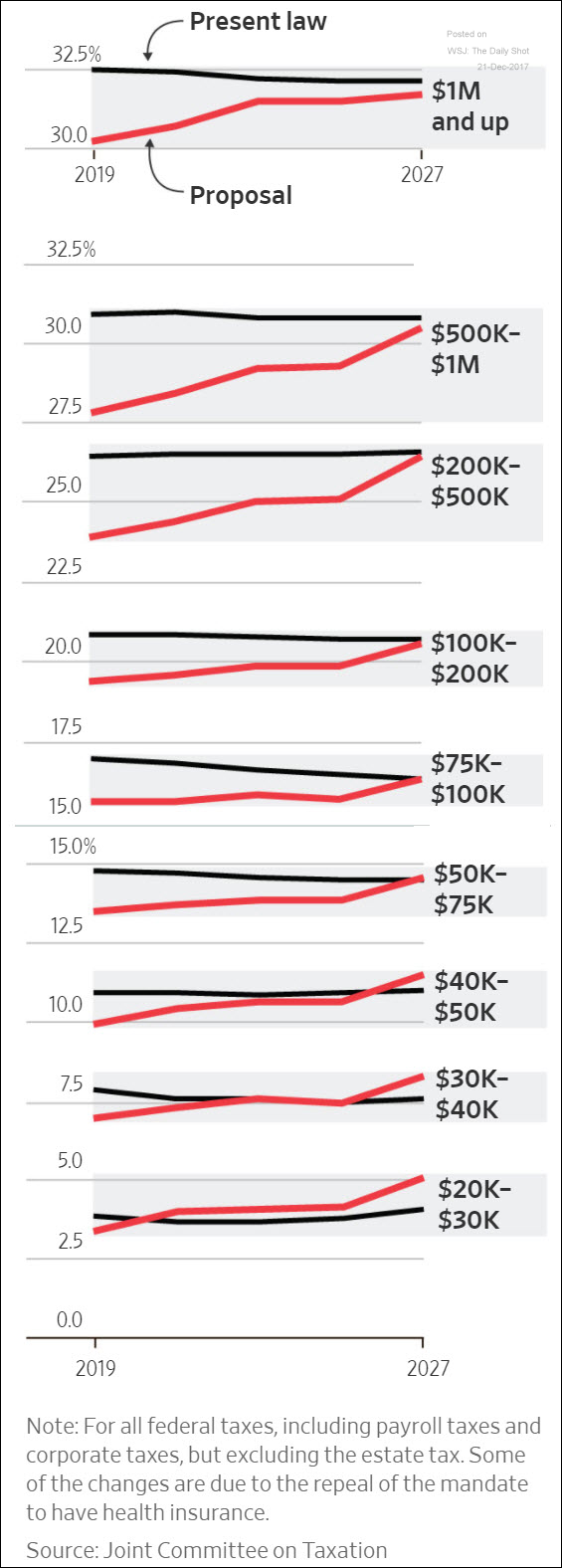

The Wall Street Journal has a good series of charts showing the effect on taxes. The bottom chart surprised me… I knew the tax cuts were better for the richest but I hadn’t realised how quickly the poorest went to paying more tax.

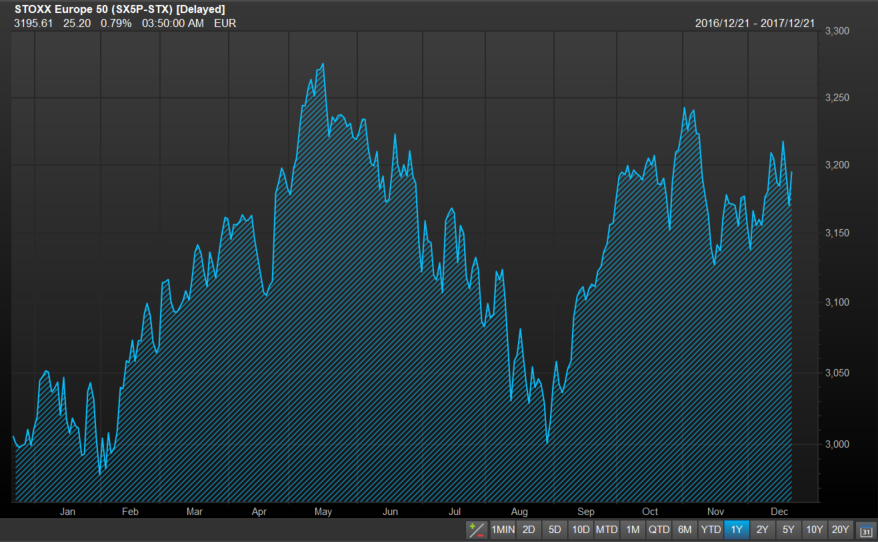

There was little movement in markets overnight.

Exceptions were European markets (which were just reversing the prior day’s losses):

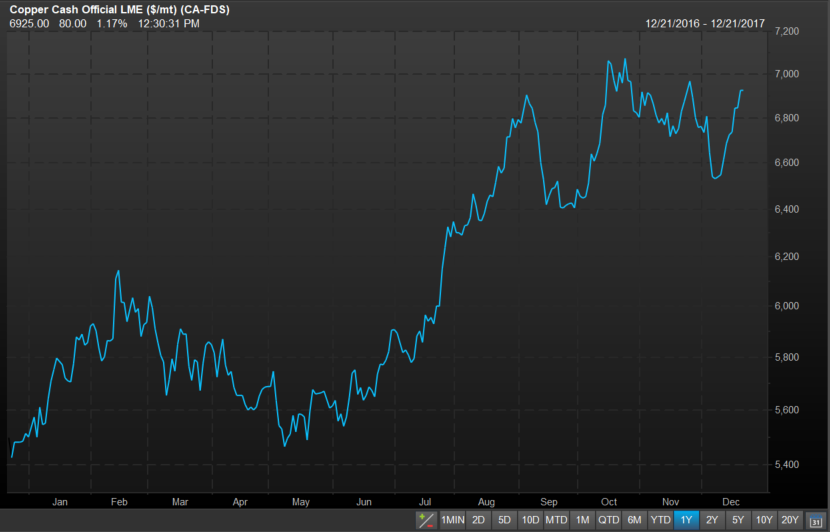

Industrial metals:

and the AUD which continues to lift higher:

We reduced our international weight last month, and its getting tempting to start adding to our international exposure again with the AUD higher.

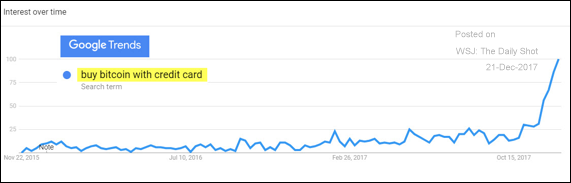

I’m trying hard not to write about bitcoin, but I couldn’t help posting this chart:

I’m sure the people doing these searches know exactly what they are doing…

Damien Klassen is Head of Investments at the Macrobusiness Fund, which is powered by Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.