Exclusively from Gerard Minack

Australia seems set for another year of desultory growth, avoiding a statistical recession but experiencing per capita pain. Weak wages and a fading contribution from housing are now headwinds. Improved corporate sentiment suggests some upside risk to this scenario, but the most likely outcome is unchanged monetary policy, moderate A$ declines and domestic equities continuing to lag global markets.

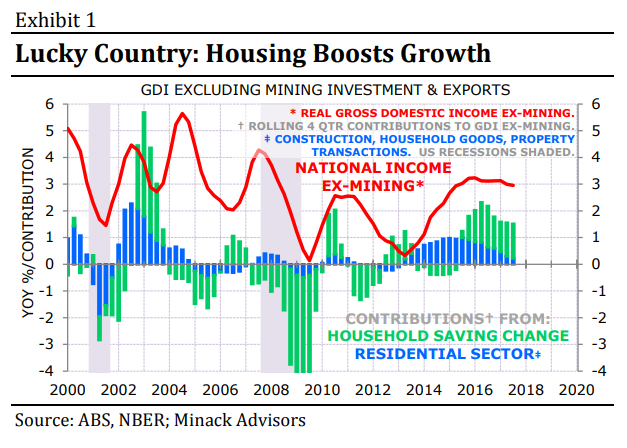

A bust in mining investment and export earnings through 2014-15 could easily have pushed Australia into recession. However – in the nick of time – activity in other sectors expanded to avoid a hard landing. Housing-related spending – both the direct contribution from building and furnishing homes, as well as indirect wealth effects – was the key to the expansion in non-mining activity (Exhibit 1).

However, growth has been sluggish, and seems set to remain so heading into 2018. There are at least three important headwinds.

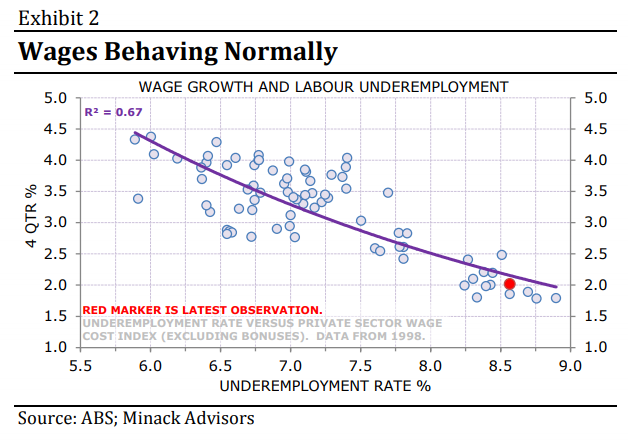

The first is the weakness in labour income. This is easy to explain: wage growth is weak because under-employment is high (Exhibit 2).

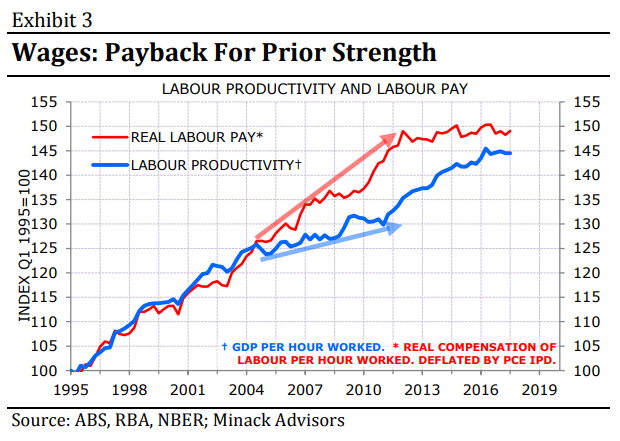

There is also an element of payback: real wage growth outstripped productivity through the boom (Exhibit 3).

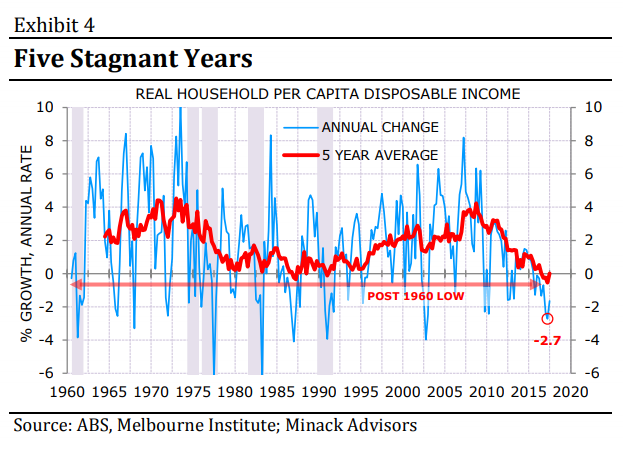

The upshot of weak wage growth plus rising effective tax rates – versus declining effective tax rates through the boom – is that real household disposable income is flat-lining, while real per

capita incomes are falling sharply (Exhibit 4).

The second headwind is the turn in the housing market. The direct contribution to growth has disappeared. The big double-barrelled uncertainty, however, is wealth effects: both how far house

prices fall, and how any fall will affect household saving. I expect single-digit house price declines next year but it’s not clear how such a wealth setback will affect saving. Recession is not my base case, but is a risk if there is an out-sized consumer reaction to falling house prices.

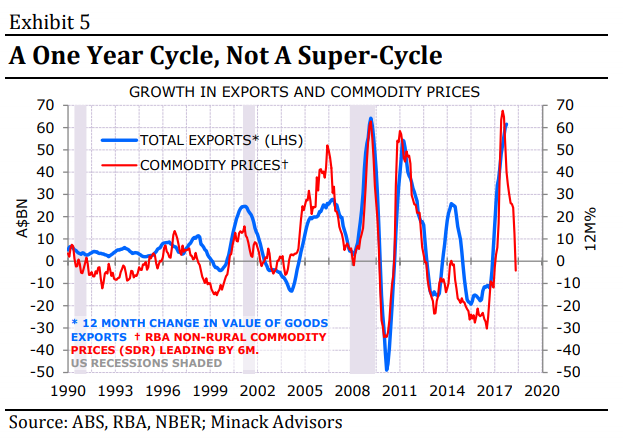

The third headwind is fading resource export growth. A spike in commodity prices delivered a surge in export income now at its apex (Exhibit 5).

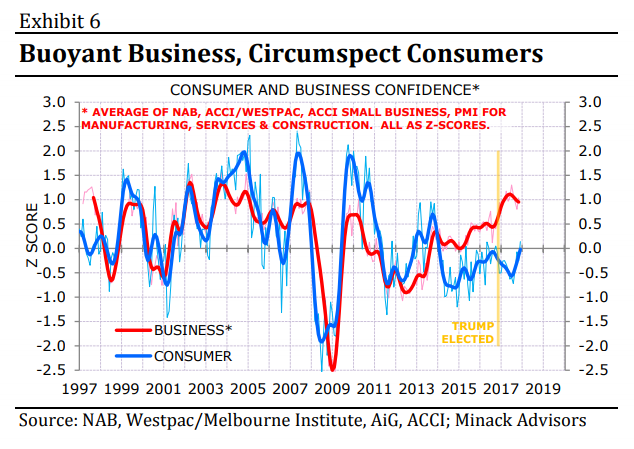

There is good news. Corporate sentiment is near its highest level this cycle (Exhibit 6).

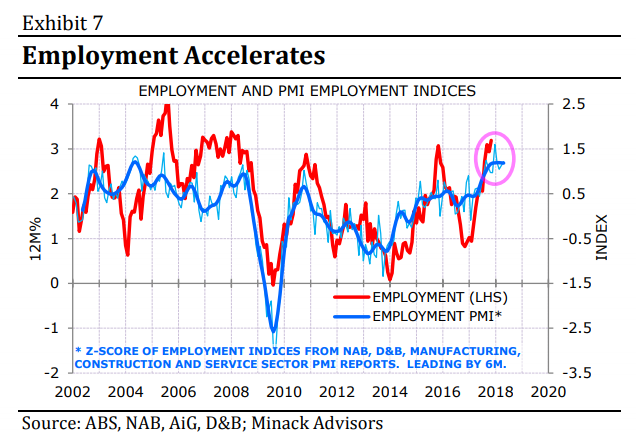

More importantly, upbeat corporates are now hiring (Exhibit 7).

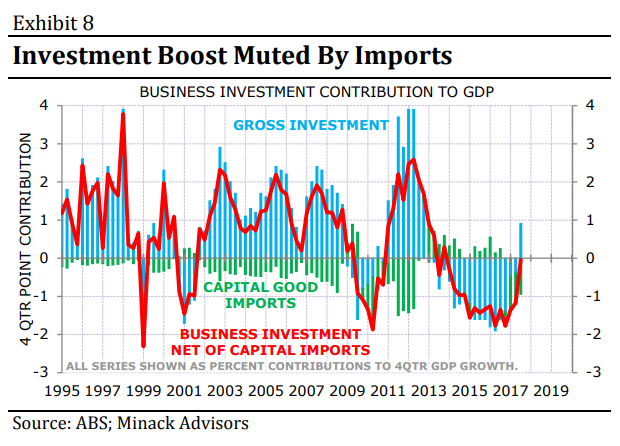

Finally, it seems that investment spending has turned the corner. The great mining capex bust has run its course, and non-mining investment is now rising. However, much investment spending spills overseas: the 1 percentage point contribution to growth from investment over the past year was largely offset by rising capital imports (Exhibit 8).

Six months ago I was very gloomy about the outlook for Australia in 2018. My base case was weak growth, but I saw a one-in-three chance of recession, and almost no upside risk. The turn in business sentiment, with the follow-through on hiring and investment spending, suggests the risks in 2018 are more balanced. The recession risk is probably no higher than 20%. In any case, it’s difficult to have a statistical recession when population growth is running at 1½-¾% – even if trend per capita income growth is weaker now than the period that included the 1990s recession.

But the base case remains one of anaemic, desultory growth. The best has been seen for housing and resource exports in this cycle. Employment growth has been solid, but fast population growth means that underemployment remains high. Wage growth is therefore likely to remain sickly.

This is a setting where there is no case for RBA rate increases, which would come on top of already-seen hikes for housing investors. A peak in commodity prices points to gentle A$ declines. And this is a combination where I would expect Australian equities to continue to under-perform global equities in common-currency terms.