With Trump looking increasingly likely to leave tax cuts under the Christmas tree for all the good boys and girls (i.e. anyone who is rich), and lumps of coal for anyone concerned about climate change, the US market powered on again overnight:

The US dollar took a breather:

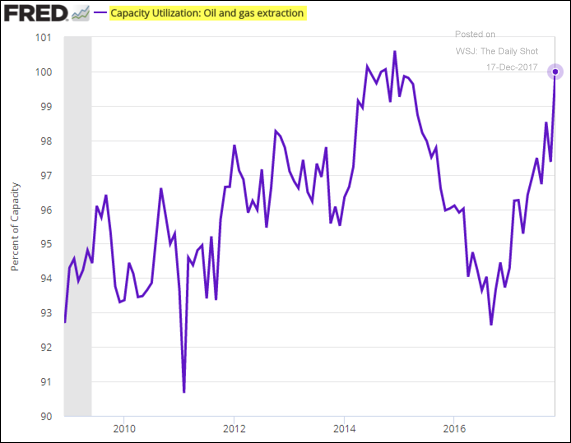

Oil was largely flat overnight, but two oil charts caught my eye from the WSJ – first was FRED suggesting that oil has reached its capacity, suggesting that capex is going to be needed for any further increases:

Advertisement