From LF Economicscomes a blog post questioning whether population growth drives house price growth:

With the latest demographic figures recently released, population growth in Australia continues at a rapid pace. Unlike many other developed nations i.e. Eurozone which have experienced little to no population growth over the last couple of decades, Australia is a significant outlier.

A major concern is that the government’s immigration program – where the vast majority of population growth is coming from – is, in part, a factor in Australia’s extraordinarily high dwelling prices (houses more so than units). Although it would seem straightforward to link population growth to dwelling prices, the situation is more nuanced than it seems.

What has led to confusion over this link is the differentiation between fundamental and speculative dwelling price growth. The former is based on fundamental metrics such as rents, incomes, inflation, etc. while the latter is based on debt-financed speculation.

If population growth is exceeding the number of dwellings needed to house said population, it should be expected that rents will rise. This would most obviously be indicated by rising market rents for investment properties, but also imputed rents for owner-occupier dwellings.

As is demonstrated below, construction, adjusted for demolitions and secondary dwellings i.e. holiday homes and second owner-occupier homes, has often exceeded the flow of new households, decomposed from population flows. When surpluses occur, rent growth is low. In contrast, when deficits arise, rent growth is high. From a fundamental perspective, population growth influences dwelling prices to the extent that is causes rents to rise.

As an aside, it is fascinating to see that most dwelling price growth occurred during periods of surpluses, while price growth flattened between 2007 – 2013 when deficits occurred. This is in complete contrast to the claim by government, industry and mainstream economists that strong price growth is due to the alleged dwelling shortage. This should come as no surprise to those who understand the dynamics of prices and construction.

Dwelling prices, on the other hand, do not demonstrate the same trend with population flows. International evidence also indicates a lack of correlation. Ireland, for instance, had strong population growth during its boom. Yet the one country with the greatest boom of all, Lithuania, where real housing prices escalated by 375% between 2001 and 2007, has had negative population growth since independence in 1990.

These outcomes suggest that dwelling prices tend to be influenced by factors other than what is suggested by fundamental metrics like population growth. The obvious culprit would be debt-financed speculation as the GFC demonstrated.

Could it be that higher population growth results in more speculation than would otherwise be the case? If this were true, the highest dwelling price growth should’ve occurred during 2008/09 and 2011/12 as population growth peaked but instead prices actually declined.

It will take a carefully calibrated empirical study to determine the effects of population growth on dwelling prices, including being able to differentiate between fundamental and speculative sources of price growth.

That said, the program of population quantitative easing (PopQE) the government is running is causing real problems. Is Australia’s immigration policy now aimed towards holding up the housing market in Sydney and Melbourne? There seems little other explanation as to why the government would allow such an influx of new residents knowing that the quality of life in these two cities are diminishing by the day.

An aging population with more disability is facing increased competition, which is especially acute among the fifth of aged pensioners who rent. The social housing sector is under immense strain after two decades of disinvestment by the federal and state governments. Underutilisation is growing, with many dwellings left uninhabited. This all serves to increase private market rents.

It is high time that government publicly reviewed its immigration policy, taking these factors into account.

My own view is that the debt explosion was the primary driver of house prices over the first half of the bubble. But the population ponzi has been the primary driver over this decade.

Advertisement

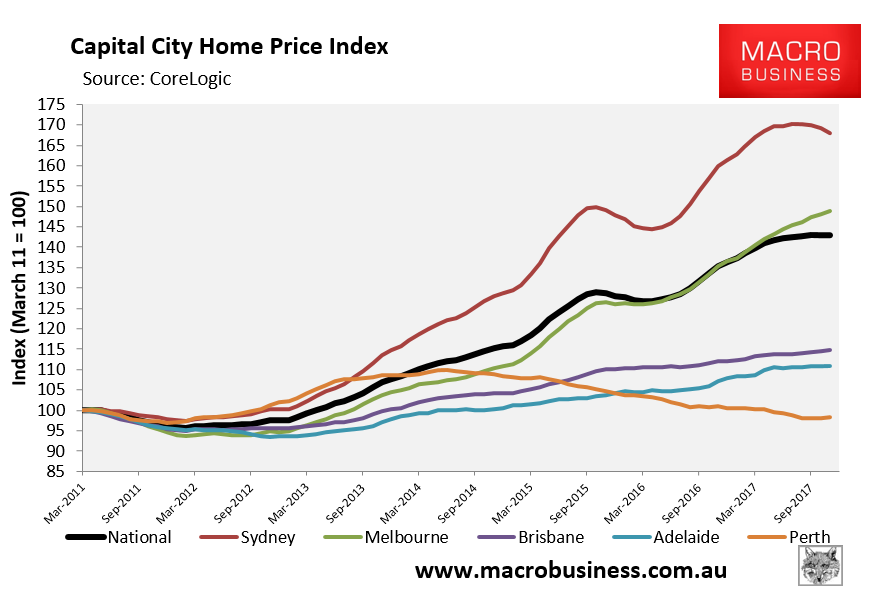

One only has to look at the explosive price growth in Sydney and Melbourne, where values have diverged so strongly from the other capitals:

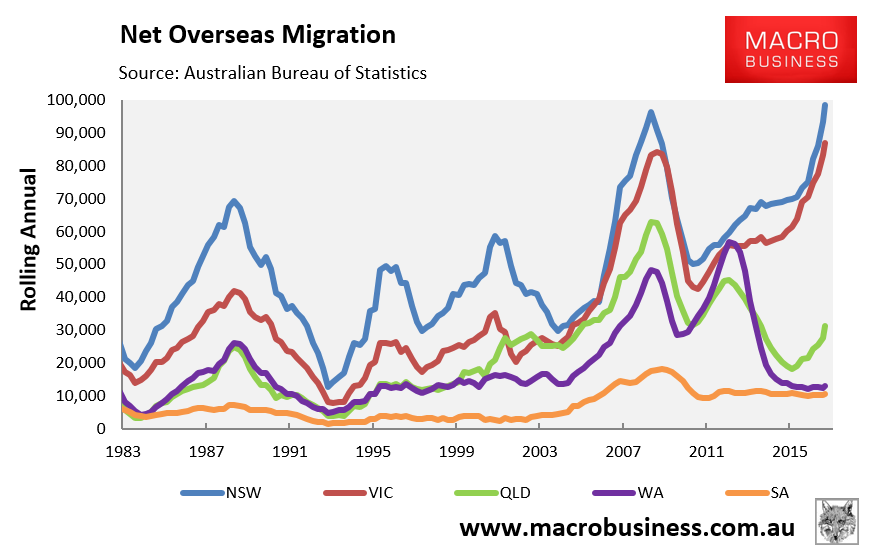

Which mirrors the explosion in the migrant intake (population growth):

Advertisement

There’s also the associated issue that more people means more debt. So, it’s all part of the same Ponzi dynamic.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.