From Morgan Stanley today:

We see the RBA firmly on hold in 2018 as the headwinds from a consumer crunch and evolution of a housing slowdown prevent Australia from joining the global tightening bias to monetary policy.

The lack of carry for the Australian dollar makes rates differentials and rate expectations much more important in driving near term direction of the Australian dollar, particularly as the optics and direction of the commodity pulse stays muted over the quieter Northern hemisphere winter months.

Selling AUD is a top recommended trade in our global 2018 outlook across asset classes .

High real returns in EM and rising US rates mean that the yield advantage offered by the AUD relative to G10 counterparts may no longer be sufficient to compensate investors

When we look to the ASX 200 – we also note that the prospective dividend yield for the market is now trending below the long run average, standing at 4.4 per cent.

We explain this as a reality that after years of giving back cash to shareholders at the expense of growth, companies now realise that some increase in capital allocation to replacement and growth opportunities is required to achieve strategic goals.

Add this to a market earnings cycle for industrials that has decelerated as domestic headwinds mount,and lower earnings and reducing payout ratios are a logical outcome of the current state of play.

The combination of less carry in the AUD and domestic headwinds for consumer and housing linked Industrials are key drivers of our continued preference for outsized positioning in global growers.

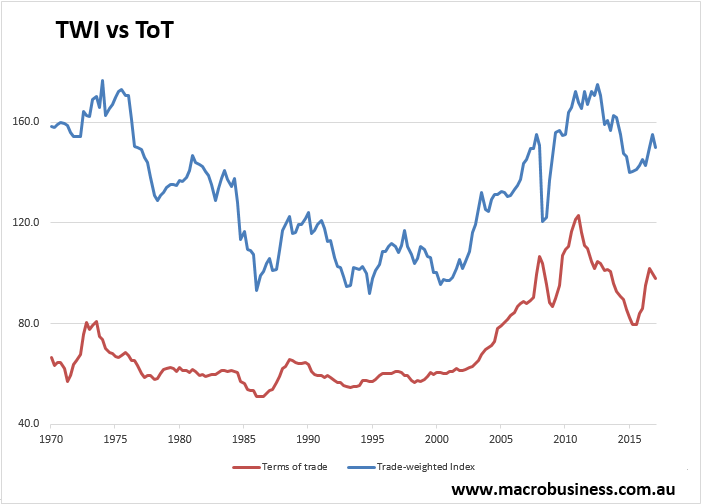

Too bullish. The EM trade is going to falter right along with Chinese growth and commodity prices, putting even more pressure on the AUD. We can see this in the history of the relationship between the trade-weighted index (which the currency plus inflation) versus the terms of trade:

Where one goes, the other follows.

———————————————————————–

David Llewellyn-Smith is chief strategist at the MB Fund which is currently long local bonds and international equities that offer superior growth and benefit from a falling AUD so he is definitely talking his book.

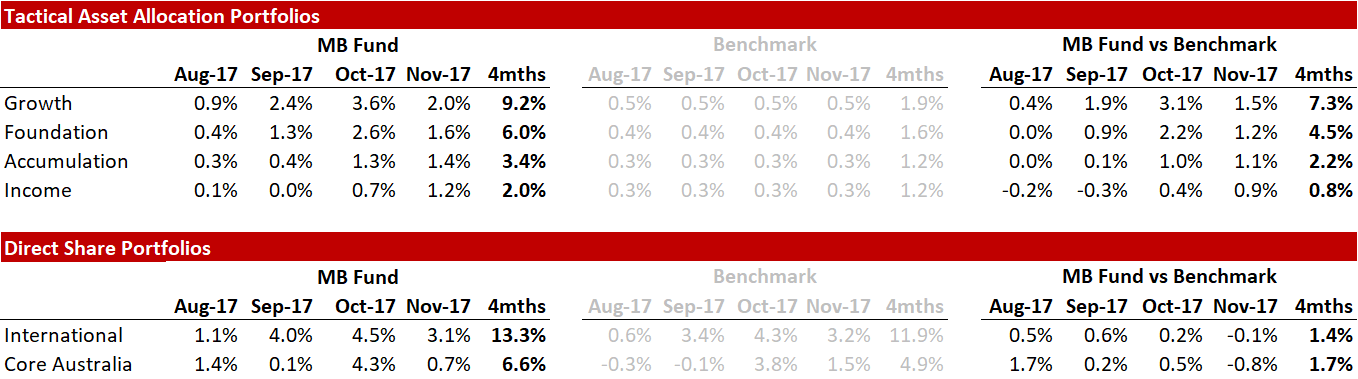

Here’s the recent fund performance:

Source: Linear, Factset

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. October monthly returns are currently at 4.9% for international and 4.2% for local shares.

If the themes in this post and the fund interest you then register below and we’ll be in touch:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. The MB Fund is a partnership with Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.