XJO is adding a little today:

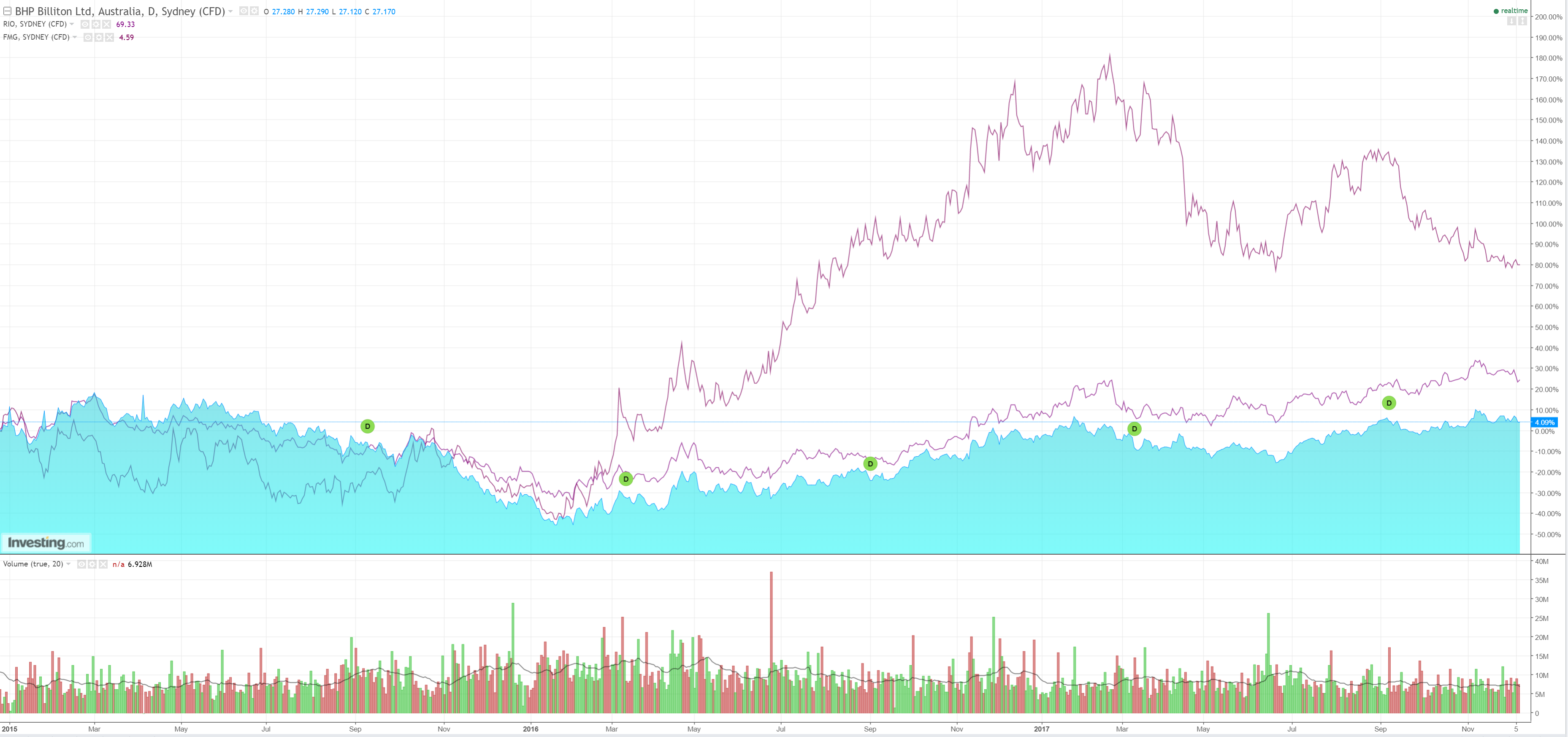

Big Iron is mixed with RIO up on ATRs, BHP down on oil and FMG still at the brink:

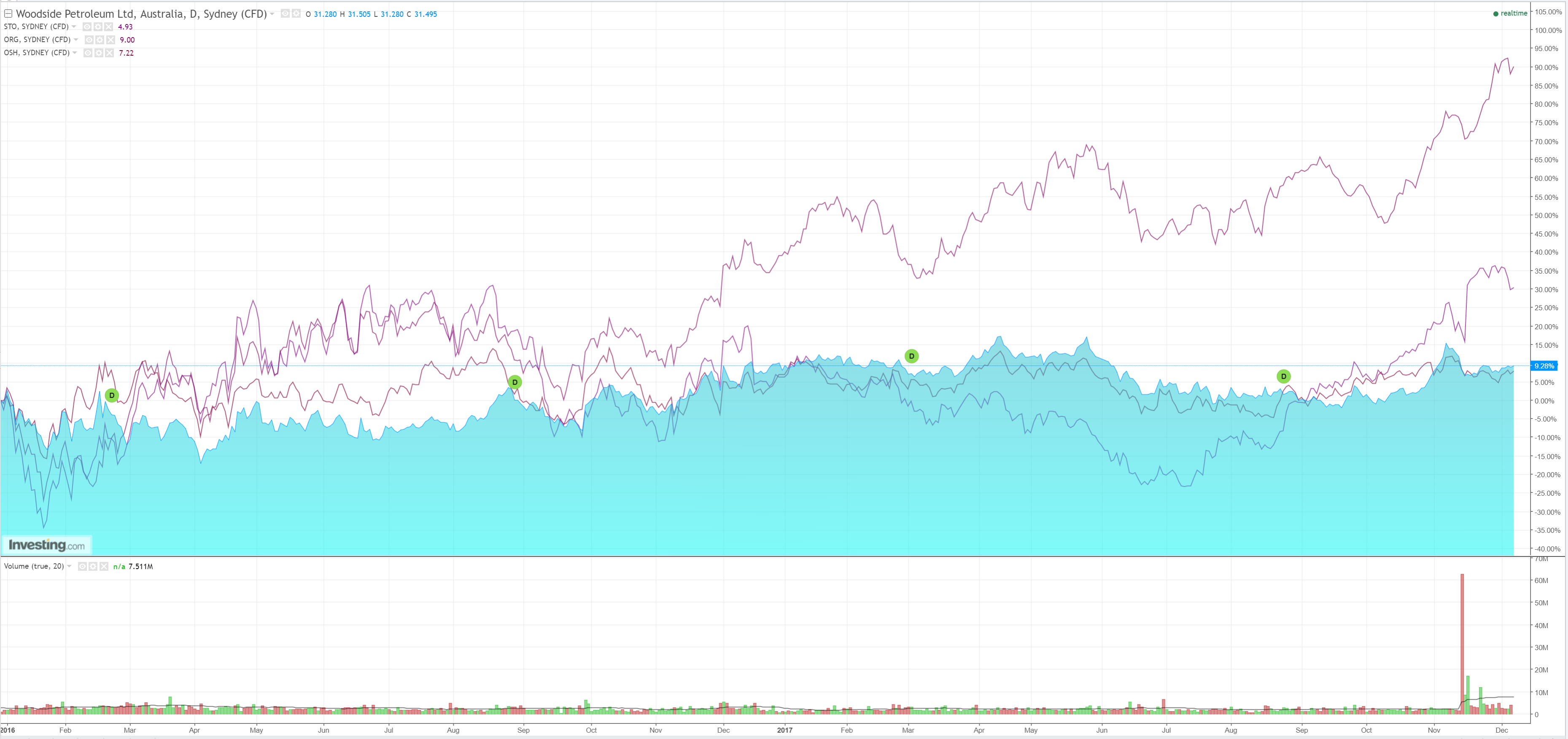

Pensioner killing is back in vogue:

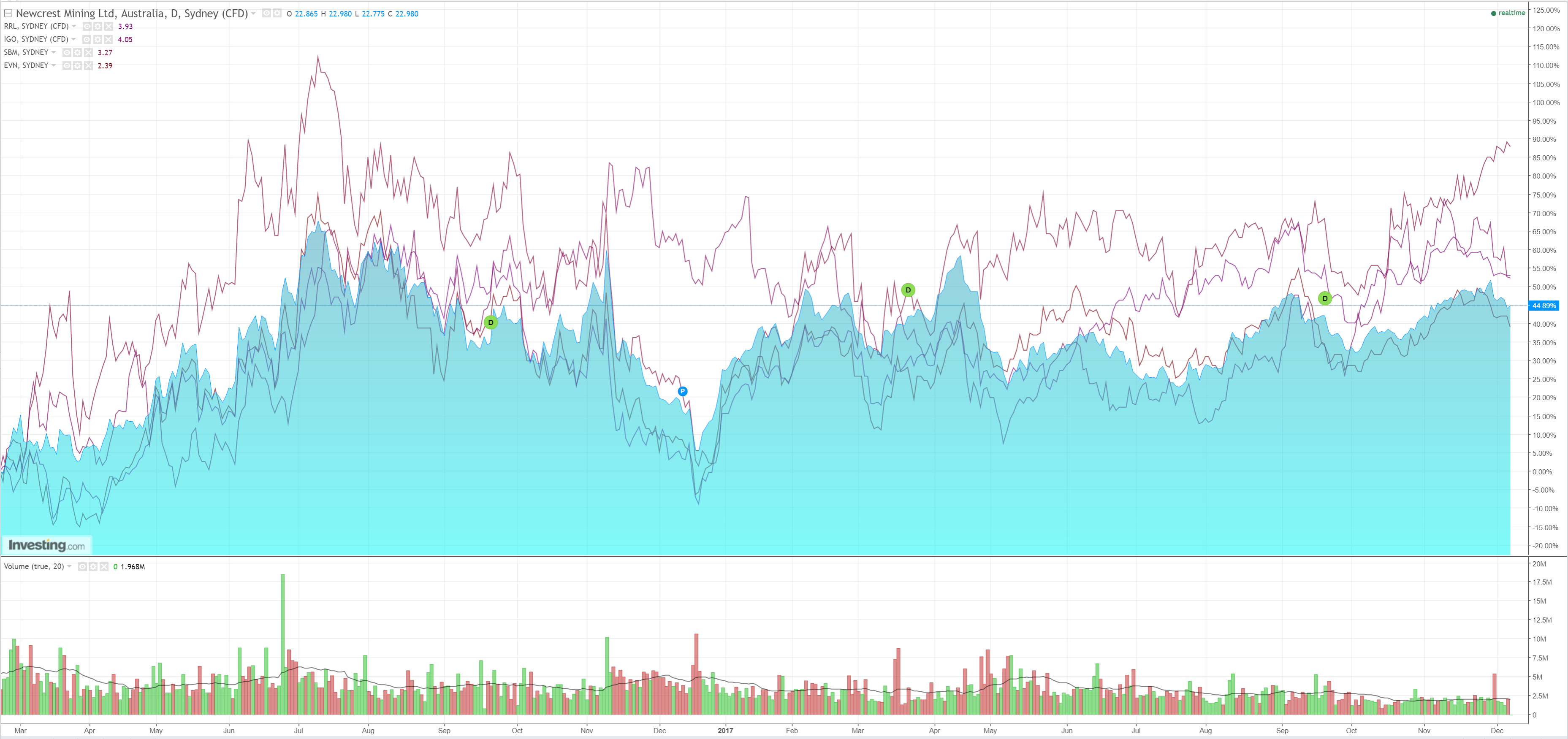

The Big Gold correction is gathering steam:

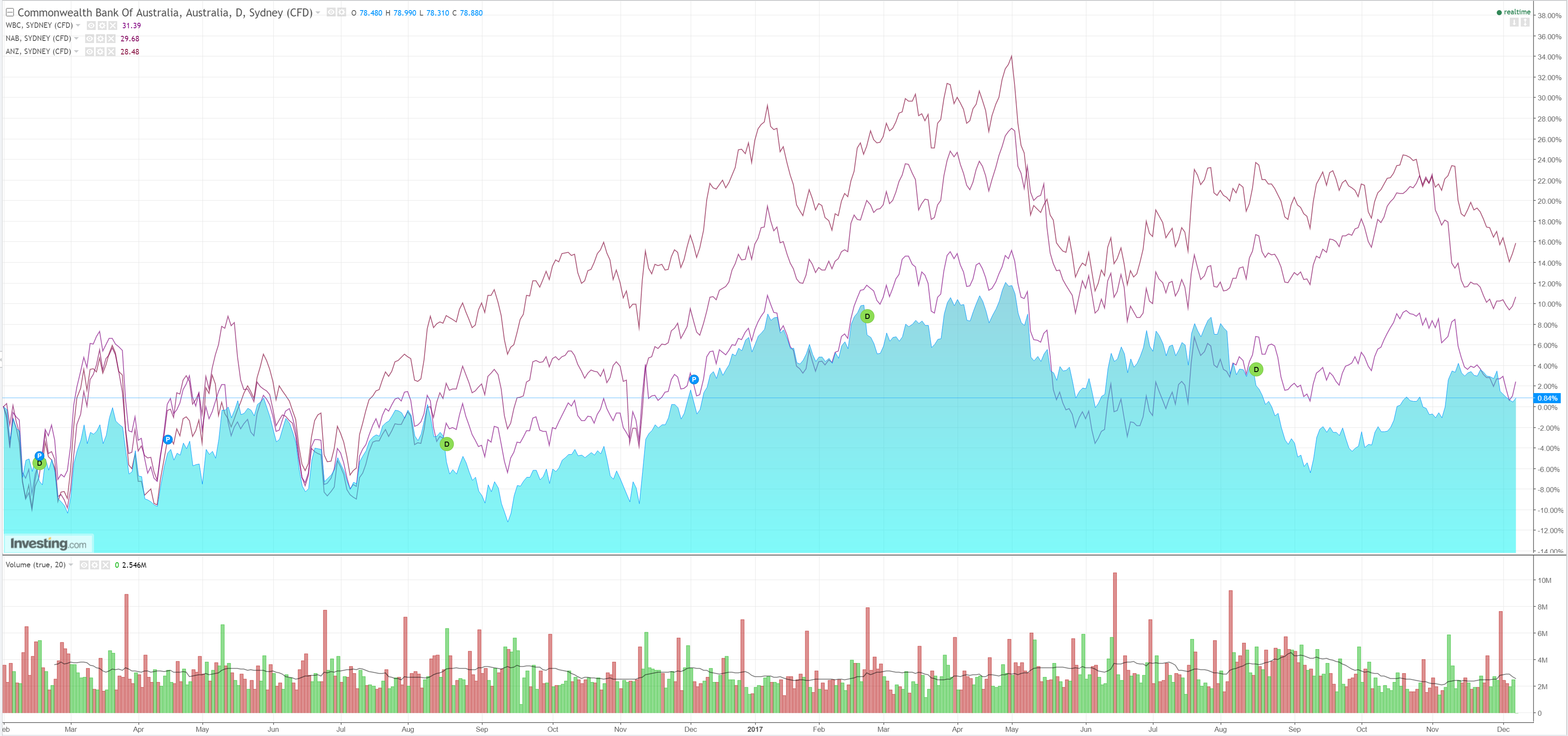

Big Sleazy is dead cat bouncing as yields fall:

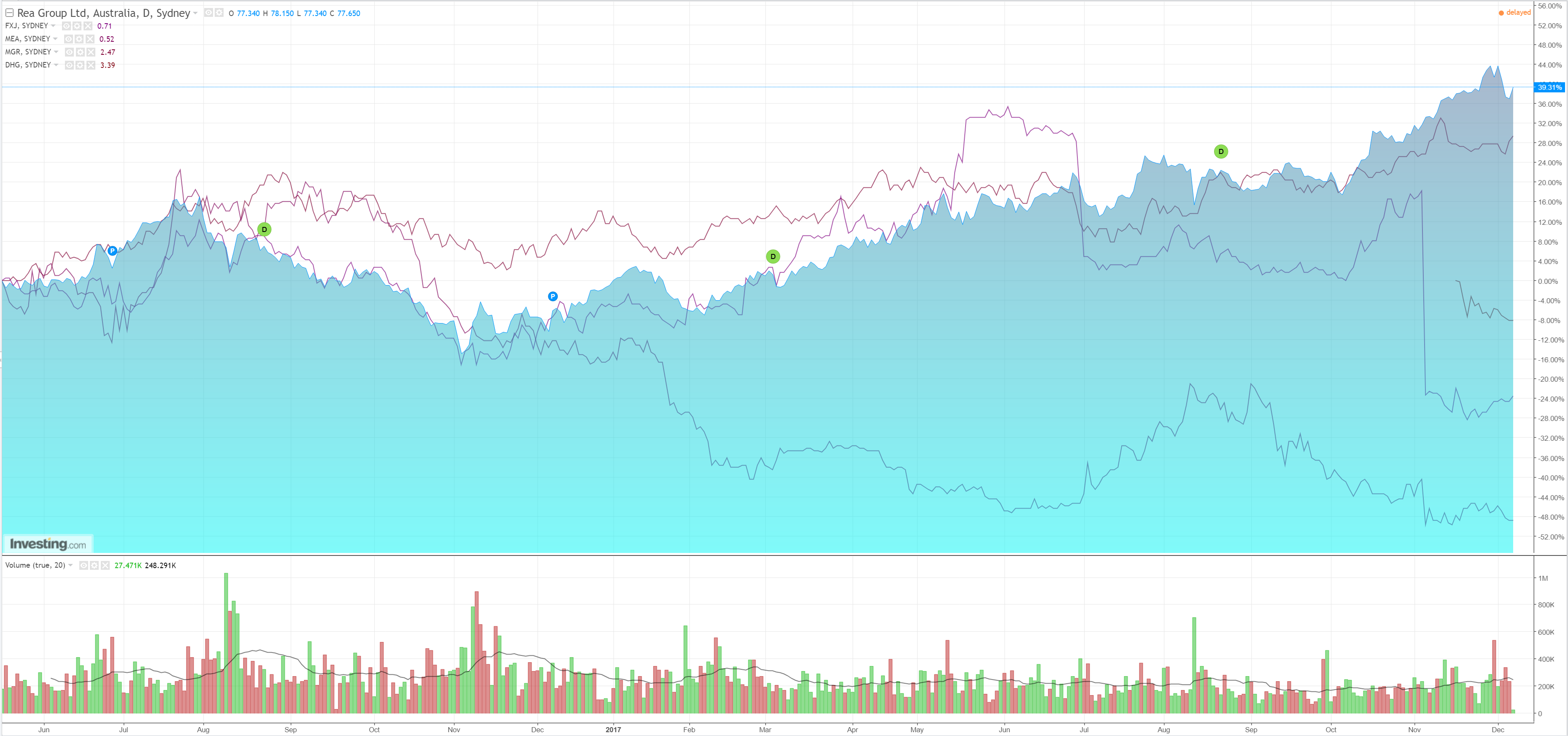

Big Maggot is also up. It’s now clear that REA is a NASDAQ proxy:

Morgan Stanley says next year is Groundhog Day for the bourse as it goes backwards:

We accept above trend multiples (now assuming 15x as base case value) to feature but push back on the concept that aggregate EPSg accelerates from current low 4%. This adds up to a target 5800…

Breached not Conquered – Not enough EPS to take market sustainably through 6000 in our view

Supported by below trend economic growth forecast

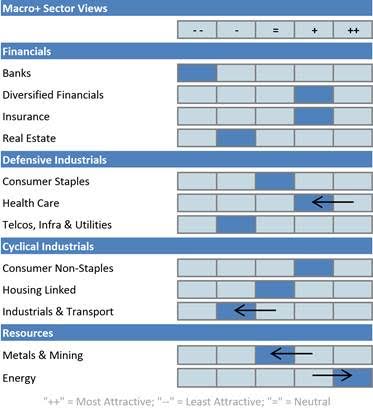

More importantly we identify 5 themes you need to take a view on:

AUD Direction – we see the AUD down directionally and want to be positioned in Global Growers as a Result.

Fiscal Policy – we might not get a Federal Election next year but it will feel like an election year. We want some Response stocks in the mix.

Consumer Crunch – Its Real and will continue to build over 1H18e in our view.

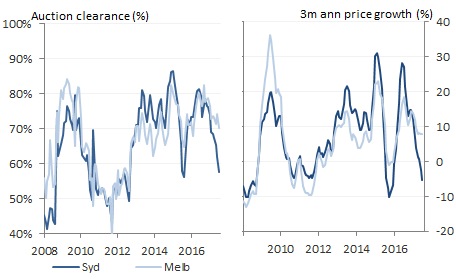

Housing – Its slowing – it feel like end 2015 but cant see the RBA cutting like last time to turn things around.

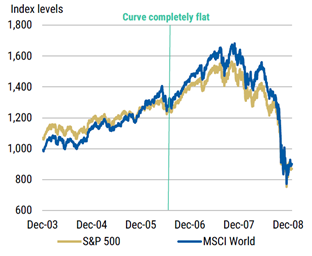

Shape of the Curve – we feel that our year end US10 target of 1.95% is something to wait for rather than position for. Risks ahead of that scenario are more about inflation upside surprise and we position for some of that.

Our key changes in Positioning:

I agree. Although resources have the iron ore tailwind for H1 it’s awful beyond that. If we get a cleared away RC by H2 then banks could fill the gap but that is just back-and-forth rotation without growth.

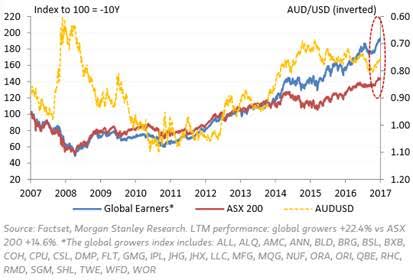

Much better options lie overseas. Especially so given the still high AUD is once again at the cliff’s edge:

———————————————————————–

David Llewellyn-Smith is chief strategist at the MB Fund which is currently long local bonds and international equities that offer superior growth and benefit from a falling AUD so he is definitely talking his book.

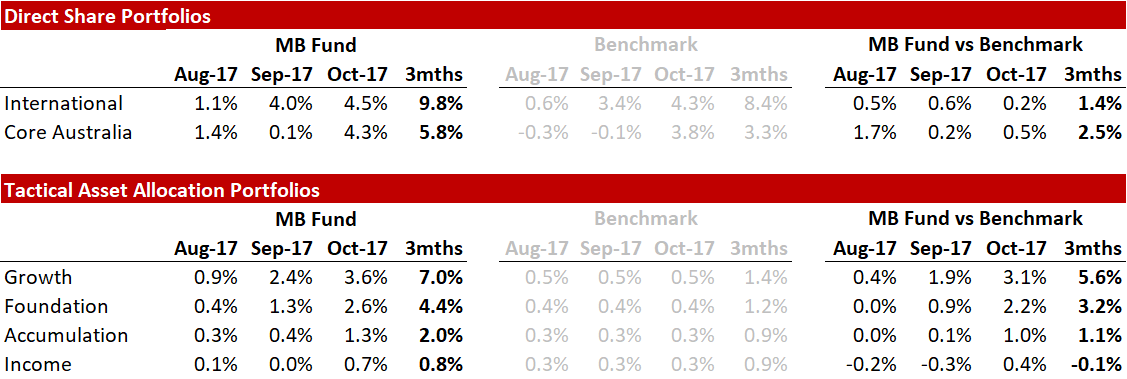

Here’s the recent fund performance:

Source: Linear, Factset

The returns above include fees and trading costs on a $500,000 portfolio. Note that individual client performance will vary based on the amount invested, ethical overlays and the date of purchase. The benchmark returns do not include fees. October monthly returns are currently at 4.9% for international and 4.2% for local shares.

If the themes in this post and the fund interest you then register below and we’ll be in touch:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. The MB Fund is a partnership with Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.