by Chris Becker

A mixed day here in Asia as the Bank of Japan leaves its monetary settings and stimulus on the same path and stocks continue to already price in the Republican tax plan passed last night. Yields on longer term government bonds continue to climb higher while commodities are relatively stable as oil remains elevated.

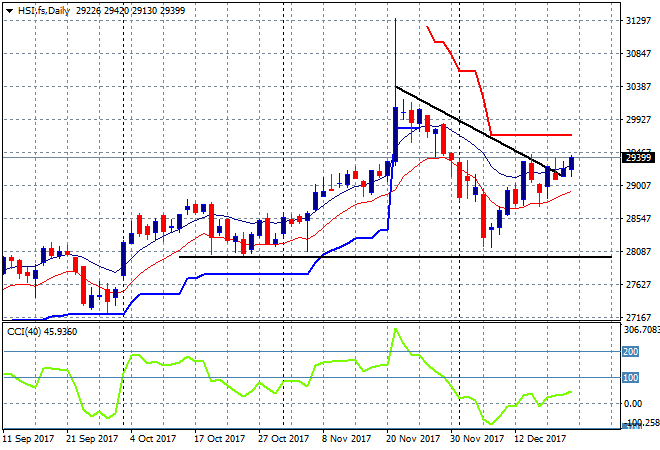

In mainland China the Shanghai Composite has bounced back after the long lunch break, currently up 0.6% to be back above the former critical key support at the 3300 point level. The Hang Seng Index has made a new daily high finally, up 0.4% to 29340 points and getting ready to break higher as momentum builds:

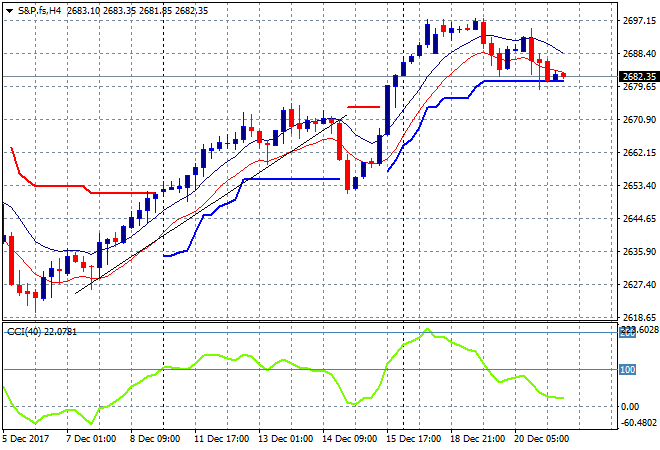

S&P futures are basically unchanged but the four hour chart shows a worrying lack of resolve at these absurd heights, so watch out for a potential retracement tonight:

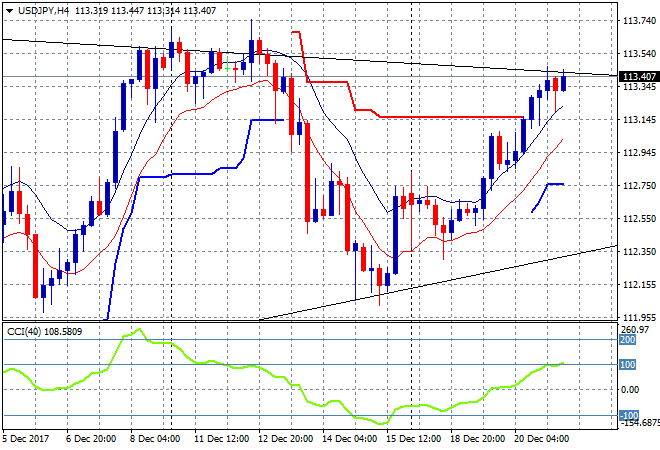

Japanese stocks were mixed on the BOJ result even as Yen continued to weaken against USD in the session. The Nikkei 225 was unchanged at 22891 points, still unable to close above overhead resistance at 23000 points. The USDJPY pair has almost met its previous weekly high although there is a slight slowdown here in intrasession momentum as it hits the 113.50 level. This corresponds to the weekly downtrend line and could prove too far to beat:

The ASX200 slumped at the open but was unable to recover, finishing down 0.2% to 6060 points in a fussy session. Energy and commodity stocks were the only real highlight, with the banks dragging down the rest of the bourse.

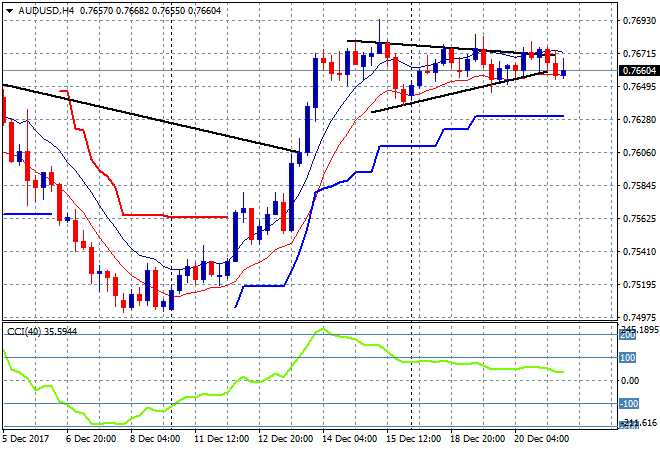

The Aussie dollar continues to remain elevated still hovering above the mid 76.60 level against the USD but there are some signs of weakness starting to appear at the four hourly and hourly charts. An inability to make a new daily high since the start of the week is weighing here, so I’m watching the 76.30 zone for a potential breakdown:

The economic calendar starts with some UK government financial reports that will be Pound Sterling sensitive, followed by Canadian CPI and then a big one with 3Q GDP and initial jobless claims from the US.