by Chris Becker

Here comes the Santa rally with all markets outside China putting on gains in response to growing certainty surrounding the US tax cuts that should pass mid-week. Bitcoin continues to make new highs while “real” currencies like Aussie and Yen were essentially unchanged following the weekend gap.

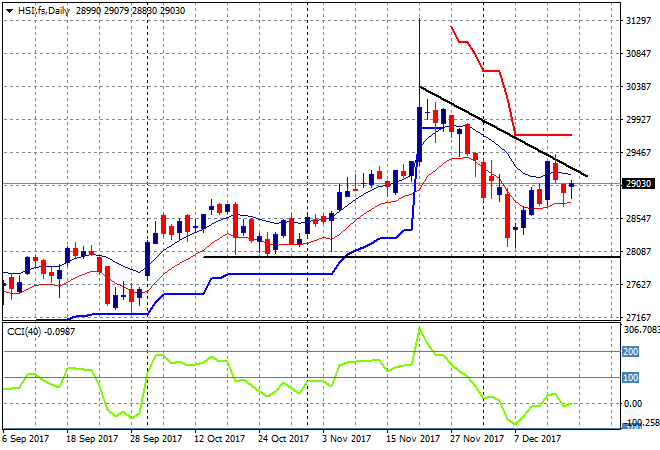

In mainland China the Shanghai Composite remains under pressure, falling 0.2% to be at 3259 points going into the close, still unable to get back above critical key support at 3300 from last week. The Hang Seng Index is doing much better, up 0.7% and taking back some of Friday’s losses, pipping just above 29000 points but still under the cloud of a downtrend since an epic breakout in mid-November:

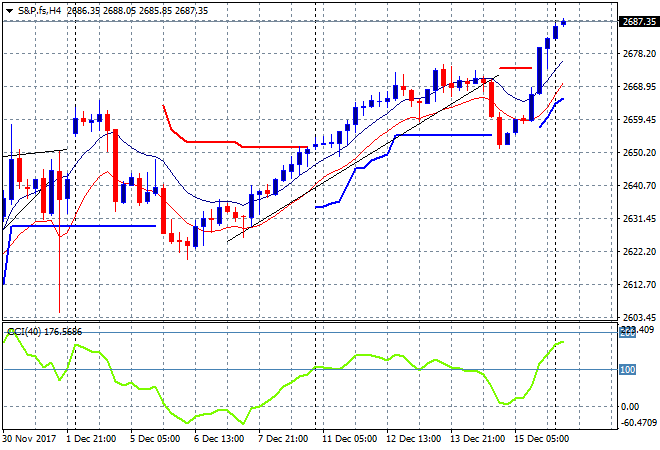

S&P futures are pushing higher after a very solid session on Friday night as Santa makes his way around the globe in the form of tax cuts for the rich:

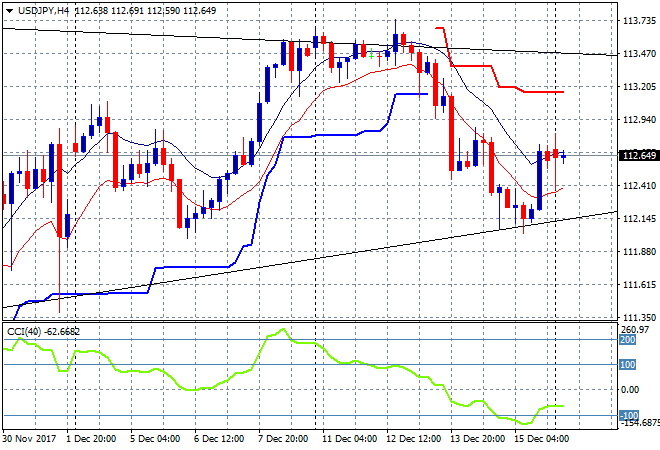

Japanese stocks have come back strongly with the Nikkei 225 surging 1.5% following the Friday night move higher in the positively correlated USDJPY pair, but still failed to close above overhead resistance at 23000 points. The USDJPY pair was relatively stable on the unnecessary Monday morning gap, unable to make any headway following that Friday night spike. If the daily/weekly pattern is to be trusted, we should see a USD rally here that takes the pair back up to the higher range above the 113 handle:

Santa loves Aussie stocks with the ASX200 pushing above 6000 points closing up 0.7% to 6038 points. This was all led by the banks, as the XXJ financial sector lept the same amount, as the Bennelong by-election result takes some heat off the political quango surrounding the most protected business in the Australian economy.

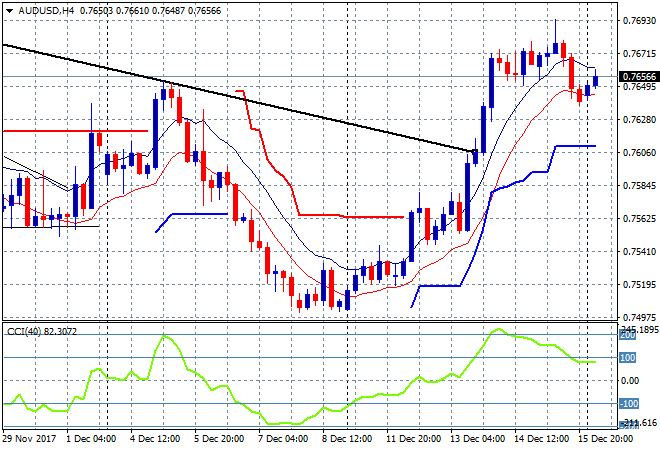

The Aussie dollar opened slightly higher on the gap after the small selloff on Friday night saw it hit below 76.50 against the USD. While momentum remains positive, the USD is coming back and is likely to go higher once the tax bill is passed, so we could see a retracement here back to the 76 handle:

The economic calendar starts the week slowly with some final EZ-wide CPI figures plus some Treasury auctions.