by Chris Becker

The usually volatile 2nd Thursday of the month here in Asia, with Aussie unemployment and the Chinese trifecta of releases shortly after got a bit more exciting today as the PBOC abruptly hiked short term interest rates. Following last nights Fed rate hike, this got markets a bit twitchy with minor setbacks across the region. The USD remained weak against the majors with the Aussie lifting appreciably on the unemployment “statistics” (fake news, Sad.)

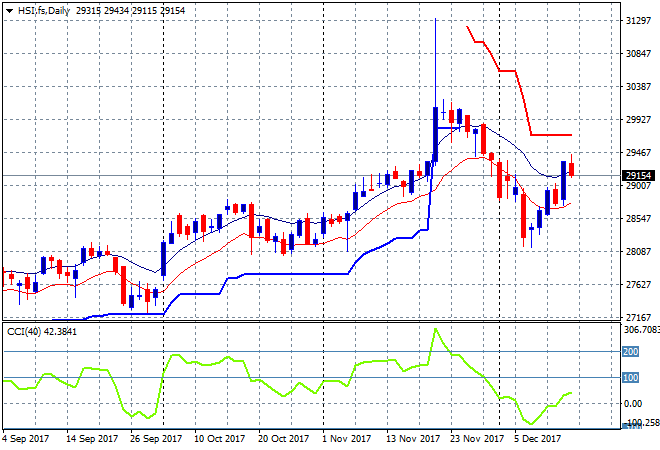

In mainland China the Shanghai Composite has fallen off after the lunch break following the PBOC move, down 0.4% to be at 3290 points, reversing most of yesterday’s gains. The Hang Seng Index is off a little less, down 0.2%, clinging above 29000 points, and obviously not confirming yesterday’s breakout:

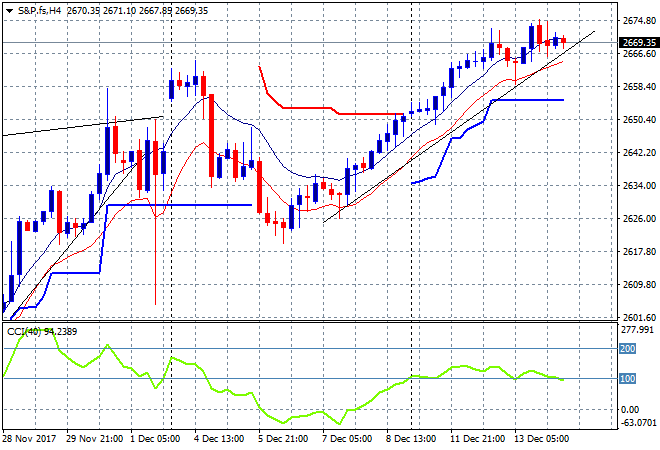

S&P futures are relatively stable here, with the trendline from last week’s low still intact:

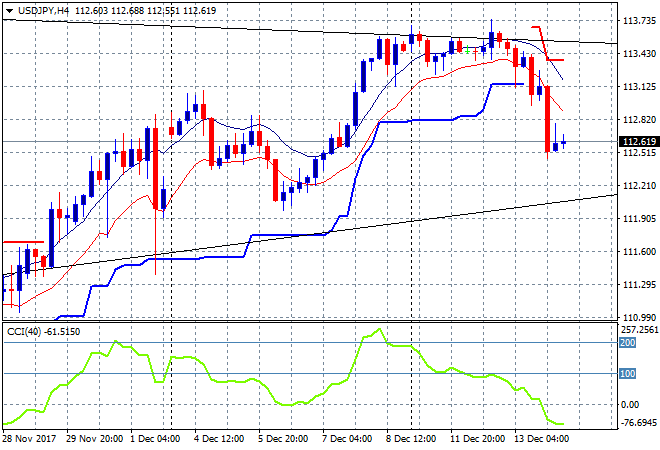

Japanese stocks sold off once again in response to a much stronger Yen overnight with the Nikkei 225 down 0.5% to close at 22671 points, continuing to reject overhead resistance at 23000 points. The USDJPY pair was relatively stable, unable to make new lows after last night’s breakodown below the 113 handle. The obvious short term target here is the lower bound of the weekly uptrend line (thin black line) at the 112 handle:

The ASX200 has for the third time in a row rallied at the open, but sold off during the day, unable to maintain its overnight momentum but still able to cling above 6000 points. The bourse closed down 0.1% to 6017 points, with no one sector dominating the action.

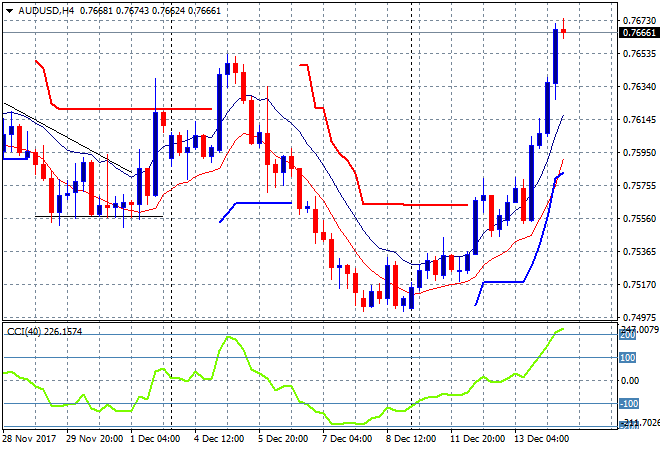

The Aussie dollar exploded higher on the unemployment print, exceeding last week’s gains and proving to once again be the popular currency to trade (especially when you get it wrong!) Again, momentum is way overdone here at below the 77 handle but price is starting to push the daily downtrend line and ATR resistance overhead:

The data calendar tonight rolls on with the monetary policy announcements, with the BOE and ECB meeting including the always price sensitive press conference thereafter. It doesn’t stop however, with advanced retail sales and initial jobless figures in the US.