by Chris Becker

A sea of red for Asian stocks today following the poor lead from Wall Street overnight as falling commodity prices on the back of a resurgent USD cascading into a mining stock selloff. 3Q Australian GDP data came in lower than expected which gave the local index a small reprieve as the Aussie dollar reversed sharply.

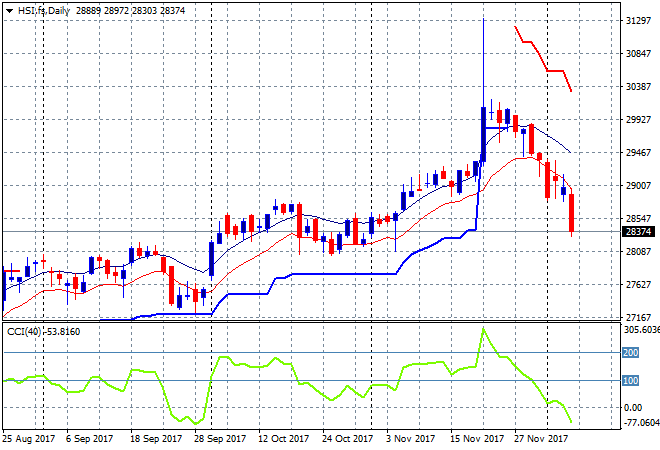

In mainland China the Shanghai Composite has fallen straight through key support at 3300 points, down nearly 1% to be at 3275 points. As I said yesterday if this level broke, the next support zone at the 3200 level beckons quite fast. The Hang Seng Index is doing even worse, down nearly 1.2% to 28481 points. My target at the 28500 point level has been reached already, with the next point at 28080 or so very close – but I think this is a little too fasT:

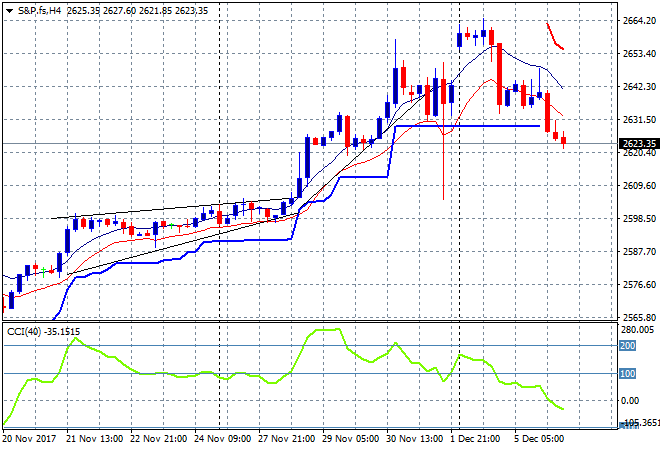

S&P futures are slipping as to be expected with the risk off mood, falling below the ATR trailing support level at 2630 which must remain firm here or this dip could widen:

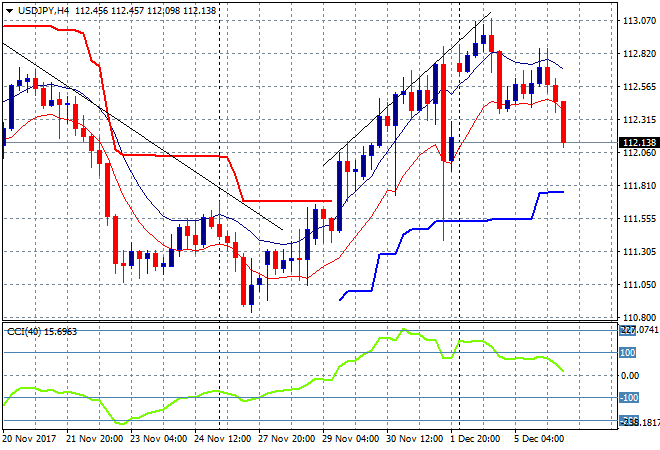

Japanese stocks were the worst in the region as Yen zoomed higher against USD. The Nikkei closed nearly 2% lower to 22195 points, confirming the bearish double top pattern I’ve been warning about on the daily chart. The USDJPY pair was looking firm here at the 112.50 mid zone but has sold off sharply in the last couple of hours. We could see a fall below the 112 handle and down to the prebreakout area at 111.50 or so:

The ASX200 gapped down again at the open on the poor lead from Wall Street but recovered somewhat on the soft GDP print, as lower interest rates continue to support the market. The afternoon session was more tepid and it sold off again, losing 0.5% to 5943 points. The main culprits here were miners, with the big-not-Australian BHP losing more than 2% with Rio Tinto off nearly 3%

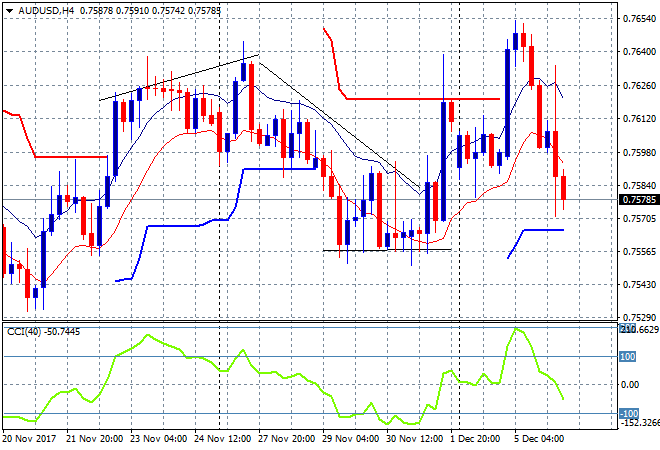

The false breakout last night on the RBA decision by the Australian dollar has been completely wiped out and then some by todays GDP print, reverting well below the 76 handle against the USD. This takes it on a trajectory to former support at the 75.60:

The data calendar includes the Canadian central bank meeting followed by a DOE crude oil inventory report.